Meta Title: Insurance Totals Your Car? Get a Fair Settlement Now

Meta Description: Wondering what happens if insurance totals your car? Learn how to dispute low offers and get a fair market value settlement with our expert guide.

Getting the call that your car is a "total loss" is a gut-punch, leaving you stressed and confused. So, what happens if insurance totals your car? In short, the insurance company has decided it's cheaper to pay you for your car's value than to repair it. This guide will walk you through the process and show you how to ensure you receive a fair settlement.

Once that decision is made, the insurer calculates your car’s pre-accident value, writes you a check for that amount, and typically takes possession of the damaged vehicle. The entire process hinges on one number: your car’s Actual Cash Value (ACV). ACV is the fair market price for your specific vehicle in your local area the moment before the crash. The insurer's first offer is just their opening bid—it is not the final word.

What Does "Totaled" Actually Mean?

When an adjuster declares your car a total loss, it’s a business decision. They have determined that the cost of repairs—plus what they could get for selling the wrecked car for parts (its salvage value)—is more than its Actual Cash Value (ACV). Think of ACV as the price your car would have sold for right before the accident.

Imagine your car was worth $10,000 pre-accident and needs $8,000 in repairs. The insurer will likely total it. Why? They can pay you the $10,000, sell the wreck to a salvage yard for $2,500, and come out ahead financially. Understanding their process is key to protecting your interests.

To level the playing field, you need to speak their language. Here are the key terms you’ll encounter.

Key Total Loss Terms Defined

| Term | Simple Definition |

|---|---|

| Actual Cash Value (ACV) | The fair market value of your vehicle right before the accident happened; this is the key number you will negotiate. |

| Total Loss Threshold | A percentage set by your state; if repair costs exceed this percentage of the car's ACV, it must be declared a total loss. |

| Salvage Value | The amount the insurance company can get by selling your damaged vehicle to a salvage or scrap yard. |

| Owner Retention | The option for you to "buy back" your totaled car from the insurer by having its salvage value deducted from your settlement. |

| Appraisal Clause | A right in your policy that allows you to hire your own independent appraiser if you disagree with the insurance company's valuation. |

Knowing these terms is the first step in protecting yourself during the claim. They are the building blocks of your settlement negotiation.

The Total Loss Formula and State Rules

Every state has its own set of rules for this process. The most important one is the total loss threshold, a specific percentage set by law. For instance, many states have a 75% threshold. This means if repair costs exceed 75% of your car’s ACV, it’s automatically a total loss.

Other states use a “Total Loss Formula” (TLF) instead of a simple percentage. A car is declared totaled if:

(Cost of Repair + Salvage Value) > Actual Cash Value

This formula is why a car that looks fixable is often declared a total loss—the insurer is just following a state-mandated financial equation. To ensure you’re being treated fairly, you need to understand your state’s specific total loss rules.

Your Settlement Offer Is Just a Starting Point

Here’s the most important thing to remember: the insurance company’s first settlement offer is just that—an offer. It is not set in stone, and you are not obligated to accept it.

Adjusters use valuation software, most commonly from a company called CCC Intelligent Solutions, to generate an ACV report. This report looks official, but it’s just their opening argument. These reports are notorious for errors, using incorrect “comparable” vehicles, and applying unfair condition adjustments that lower your car’s value.

Your insurance policy gives you the right to dispute their valuation. A professional, independent appraisal can often uncover an extra $1,000 to $5,000+ in value by using real-world, dealer-sold comparables and correcting the insurer’s mistakes. This evidence is what it takes to level the playing field against a billion-dollar insurance carrier.

Why You Must Dispute a Low Total Loss Offer

If your insurance company’s settlement offer feels low, you’re not imagining things. Modern cars are packed with expensive technology, and repair costs are soaring. This combination makes insurers quicker than ever to declare a vehicle a total loss to minimize their payout. Disputing a low total loss offer is no longer just an option; it’s a necessary step to protect your finances.

The reason is simple: cars have become incredibly expensive and complicated to fix. What used to be a simple fender-bender can now damage sensitive systems, leading to repair bills that were unthinkable a decade ago.

A single LED headlight assembly on a newer vehicle can cost over $3,000 to replace. Swapping a windshield isn’t just about glass anymore; the attached safety camera requires special recalibration that can add hundreds more to the bill. These costs stack up fast, making it much easier for a repair estimate to cross the total loss threshold.

The Math Behind More Total Losses

Insurers across the U.S. will usually declare a vehicle a total loss once repair costs hit 70-80% of its Actual Cash Value (ACV). And lately, that threshold is being crossed more often.

Data from the CCC Intelligent Solutions’ Q4 2025 Crash Course report confirms this trend. The share of claims flagged as total losses climbed from 22.1% to 22.8% in just one year, a significant and costly shift for vehicle owners.

This jump is fueled by a few key factors:

- An Aging Fleet: In 2025, over 72% of all total loss cars were 7 years or older. While an older car has a lower value, the cost to repair it doesn’t drop nearly as quickly.

- Skyrocketing Labor Rates: Skilled auto body technicians are in high demand, and their labor rates have shot up as a result.

- Parts Inflation and Supply Chain Issues: Lingering supply chain problems have made parts more expensive and harder to find, leading to longer repair times and higher overall costs.

When an insurer hands you a total loss offer, you aren’t just dealing with the fallout from an accident. You’re fighting a market where high-tech repairs make insurance companies quicker than ever to just write your car off.

Your Car’s Age and Technology Work Against You

Here’s the paradox of modern vehicles: the safety features designed to protect you make your car far more likely to be totaled. A bumper is no longer a simple piece of plastic and steel; it now houses parking sensors, blind-spot monitors, and radar for adaptive cruise control.

A seemingly minor impact can force the replacement of the entire bumper assembly, followed by complex and expensive recalibrations. For an older vehicle with a lower ACV, these high-tech repair costs quickly push it past the point of no return. The math is also heavily influenced by where you live, so you need to understand the specific total loss threshold by state.

How Insurance Companies Calculate Your Car’s Value

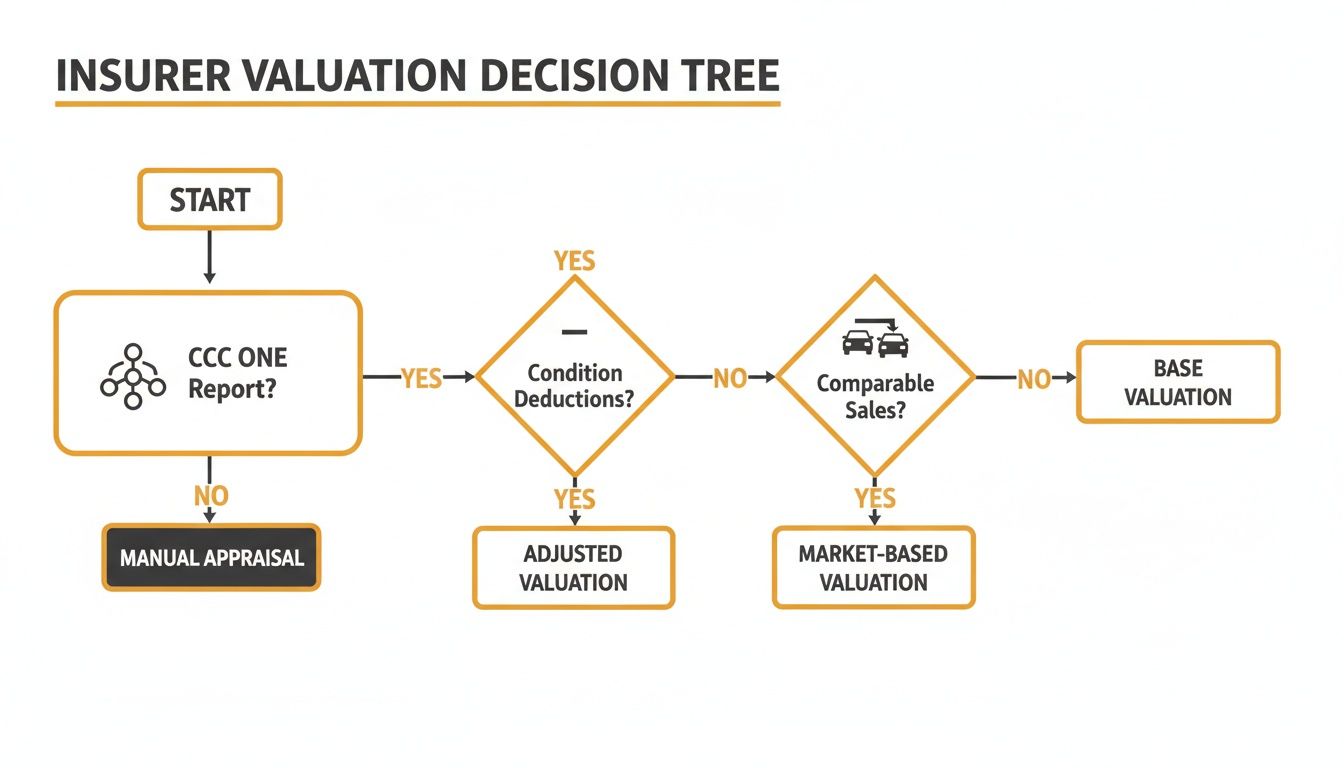

When an insurer declares your car a total loss, the claim boils down to one number: the Actual Cash Value (ACV). This is what your insurance company says your vehicle was worth the moment before the accident. But how do they arrive at that number?

Insurance companies rely heavily on third-party valuation software, and the industry king is CCC ONE Market Valuation Reports. Adjusters present these reports as definitive, computer-generated truths. In reality, they are tools that can be configured to produce a lower valuation, saving the insurance company money on your claim.

Understanding this process is the first step to protecting yourself. You aren’t arguing against a flawless computer; you’re pushing back against a flawed system that consistently overlooks the details that give your car its true value. You are also not comparing diminished value vs. total loss, as a total loss settlement should make you whole for the entire pre-accident value of the car.

The Problem with Their “Comparable” Vehicles

The heart of every CCC report is its list of “comparable” vehicles, or “comps.” These are supposedly similar cars recently sold or listed for sale in your local area, used to set a baseline for your vehicle’s value. This is where the biggest problems begin.

An insurer’s report is often filled with vehicles that are not truly comparable to yours. These “comps” might:

- Be a lower trim level: Comparing a base model to your fully-loaded Limited edition is a common tactic to get a lowball number.

- Have significant pre-existing damage: A car with a sketchy history is not a fair match for your well-kept vehicle.

- Come from a different market: A car sold 150 miles away doesn’t reflect the value in your higher-cost-of-living area.

- Be private party sales or dealer “project” cars: These are almost always priced lower than certified, retail-ready cars from reputable dealerships.

Their software can be set to seek out comps that systematically drag down the average value. It’s a common tactic to justify a low settlement offer right out of the gate.

The Shell Game of Condition and Mileage Adjustments

After picking comps, the valuation software applies adjustments for your car’s condition, mileage, and options. An adjuster might slap a “fair” or “poor” condition rating on your car for minor scratches, slashing hundreds or thousands from the value. They may also apply a large mileage deduction without considering your meticulous maintenance history.

The insurer’s report is not a final, legally binding assessment of value. It is their opening negotiation position. Your policy almost certainly contains an Appraisal Clause, giving you the right to hire your own independent auto appraiser to challenge their number with a data-driven market valuation report.

What happens if the insurance totals your car right after you invested in it? The initial CCC report will almost always ignore recent upgrades like new tires or a new battery. These are real costs that add to your car’s value, but the insurer’s software won’t see them unless you provide proof. This is why a certified appraisal from a company like AutoAppraisalExpert is so crucial. A professional report frequently uncovers $1,000 to $5,000+ in value that the insurer’s initial report “missed.” Learn more at SnapClaim.

Your Right to Dispute a Low Settlement Offer

Getting a lowball settlement offer for your totaled car is frustrating. It feels like the insurance company holds all the power, but a powerful tool is built right into your auto policy that most people don’t know exists: the Appraisal Clause.

Invoking this clause is not about picking a fight; it’s about exercising a contractual right. It gives you the legal authority to hire your own independent auto appraiser to determine what your vehicle was really worth. This is the single most effective way to level the playing field and dispute a low total loss offer.

The Power of the Appraisal Clause

Think of the Appraisal Clause as your policy’s built-in “second opinion” button. When you and your insurer can’t agree on the Actual Cash Value (ACV), this clause provides a clear, legal process to resolve the dispute. Subrogation, which is when your insurer recovers money from the at-fault party, happens separately and doesn’t affect your right to a fair ACV settlement from your own carrier.

Here’s how the appraisal process generally works:

- You hire your own appraiser. This is an expert who works exclusively for you, not the insurance company.

- The insurer hires their own appraiser. This is typically the same adjuster or another evaluator from their team.

- The two appraisers negotiate. Using evidence and market data, they try to agree on a fair value.

- An Umpire makes the final call. If the two appraisers can’t agree, they select a neutral third-party “umpire” who will review both reports and make a binding decision.

This process forces the discussion into the world of hard evidence. A certified, USPAP-compliant report provides the credible proof needed to make the insurer justify their lowball number—or abandon it altogether.

The key takeaway is that the insurer’s initial report is just their opening offer. It’s based on choices they made about comparable vehicles and condition deductions—choices you have every right to challenge.

Why an Independent Appraisal Is Crucial

Insurance companies are businesses squeezed by rising costs. Used vehicle values are at historic highs, with an average price over $25,000 according to sources like KBB.com, and parts inflation adds billions to annual claim costs. As a result, insurers are more motivated than ever to minimize payouts. It’s no surprise that a high percentage of claims are now declared total losses.

An independent appraisal cuts through the noise. It forces the conversation to be about one thing: what your specific car, with its unique history, condition, and options, was worth in your local market the day before the crash.

A professional market valuation report doesn’t use the insurer’s cherry-picked data; it builds a case from scratch using real-world evidence from your local area. This is the gold standard for winning a dispute over what happens if insurance totals your car, providing the concrete documentation needed to negotiate effectively and potentially increase your settlement by $1,000 to $5,000+.

Managing Payoffs, Loans, and Salvage Titles

Once you and the adjuster settle on a final number, the paperwork phase begins. This is where money moves and titles change hands. Understanding what happens next with your loan and the vehicle’s title is essential to wrapping up the claim without leaving money on the table.

First, let’s talk about the settlement check. If you have an outstanding auto loan, your lender is the legal lienholder, meaning they have a right to be paid first. The check for the agreed-upon Actual Cash Value (ACV) will go straight to your bank or finance company to pay off the remaining loan balance.

If the settlement is more than what you owe, your lender will take their share and send you a check for the difference. However, if you owe more on your loan than the car is worth—a situation known as being “underwater”—the ACV payment won’t be enough to close the loan. You are still legally on the hook for that remaining balance.

What Happens if You Still Owe Money?

This shortfall is precisely where Guaranteed Asset Protection (GAP) insurance becomes a financial lifesaver. GAP is an optional coverage designed to pay the difference between your car’s ACV and the amount you still owe on your loan.

If you have GAP coverage, it will step in to cover that deficiency, protecting you from making payments on a car you no longer own. If you don’t have it, you’ll need to work out a payment plan with your lender to pay that remaining balance out of pocket.

Keeping Your Totaled Car

What if you want to keep the car? You absolutely have the right to do this through a process called owner retention. In short, you “buy back” your wrecked car from the insurance company.

Here’s how it works:

- The insurer first determines the car’s salvage value. This is the price they could get for the wrecked vehicle from a salvage auction yard.

- They simply subtract this salvage value from your total loss settlement check.

- You receive the reduced payment and get to keep the car.

Be warned: once you retain the vehicle, its title is no longer “clean.” The state DMV will brand it as a “salvage title,” a permanent red flag to future buyers that it was once declared a total loss. To make it road-legal again, you must have it repaired and pass a rigorous state safety inspection to be issued a “rebuilt” title.

As organizations like the National Highway Traffic Safety Administration (NHTSA) often warn, rebuilt vehicles can have serious underlying safety issues. Getting a car with a branded title properly insured can also be a major headache.

Don’t Forget About Taxes and Fees

Finally, one of the most overlooked parts of a total loss settlement is the recovery of sales tax and registration fees. Many adjusters “forget” to include these, hoping you won’t ask.

In many states, the insurance company is required to include sales tax in your settlement to help you purchase a replacement vehicle. They may also owe you for the prorated portion of your unused vehicle registration fees. Always ask your adjuster to confirm that tax and fees are included in the final settlement offer.

How a Certified Appraisal Gives You the Upper Hand

When your insurance company hands you their valuation report, it feels final. It’s a dense document, often from software like CCC ONE, filled with numbers designed to overwhelm you into acceptance. But that report isn’t a final judgment; it’s their opening offer in a negotiation.

This is where you stop playing their game and start a new one—with a certified, independent appraisal. This isn’t just getting a “second opinion.” It’s arming yourself with an evidence-based weapon built to dismantle their lowball offer and prove your vehicle’s true, pre-accident fair market value.

The Expert’s Process vs. The Insurer’s Algorithm

An adjuster’s valuation is built for speed and savings. Their software can be configured to favor their bottom line. In stark contrast, a professional appraisal from an expert follows a meticulous process designed for one purpose: to find the truth.

We don’t rely on a flawed algorithm. We build a case for your vehicle’s value from the ground up, based on strict, universally accepted professional standards.

Our methodology is rooted in real-world market facts:

- Real-World Comps: We find recently sold vehicles from actual dealers in your local market. This reflects the real cost to replace your car—a far cry from the lowballed private-party ads insurers love to use.

- Valuing Every Detail: We meticulously document and assign value to every factor, from a high-end trim package and recent major service to its pristine condition.

- The Gold Standard of Appraisal: Our reports are compliant with the Uniform Standards of Professional Appraisal Practice (USPAP). USPAP is the gold standard for valuation, ensuring our findings are credible and can stand up to the toughest scrutiny.

This rigorous, hands-on approach produces a market valuation report that an adjuster simply cannot dismiss as “just an opinion.” It forces them to address the facts.

The Financial Impact of Fighting Back

Investing in a professional appraisal often yields a massive return. Our reports provide the evidence needed to negotiate, and it’s not uncommon for them to uncover $1,000 to $5,000 or more in value that the insurance company’s initial offer missed.

This isn’t magic; it’s the result of a thorough, unbiased investigation into your car’s real pre-accident worth. With rising repair costs, insurers are quicker than ever to total cars and slower to pay fair value. A certified appraisal provides the evidence needed to negotiate for the full settlement you are rightfully owed under your policy.

The moment you present a USPAP-compliant report, the dynamic shifts. The burden of proof is no longer on you to prove your car is worth more; it’s on the insurance company to justify why their number is so different from documented, real-world market evidence. This is the single most important step in taking control after learning what happens if insurance totals your car.

Frequently Asked Questions About Total Loss Claims

How long do I have to dispute a total loss offer?

There isn’t a single legal deadline, but time is critical. Notify the adjuster in writing that you intend to dispute their valuation as soon as you get their offer. Acting fast invokes your policy’s Appraisal Clause and prevents the insurer from closing your claim prematurely.

Can I keep my car if insurance totals it?

Yes, in most cases, you have the right to keep your car through owner retention. The insurer will get a salvage bid—what a scrap yard would pay for the wreck—and subtract that amount from your final settlement. However, the state will brand the vehicle’s title as a salvage title, which significantly hurts its future value and makes it difficult to insure.

What if my settlement is less than my loan?

If the settlement for your car’s Actual Cash Value (ACV) is less than what you owe, you are legally responsible for the remaining deficiency balance. This is what GAP (Guaranteed Asset Protection) insurance is designed to cover. If you don’t have GAP, you are stuck paying that balance out of pocket.

Do I have to accept the insurer’s “comparable” vehicles?

Absolutely not. You are not required to accept the “comps” their valuation report uses. In fact, disputing their list of comparable vehicles is one of the most effective ways to challenge a bad offer. A professional car appraisal for an insurance claim demolishes their argument by finding true, local, dealer-sold comparables that provide the evidence needed to prove your car’s real worth.

Don’t leave money on the table. Get your free claim review or order a certified appraisal report today to take control of your insurance settlement.

About AutoAppraisalExpert

AutoAppraisalExpert is a premier provider of independent vehicle appraisal reports and insurance claim consulting. Our mission is to equip vehicle owners with the data-driven evidence required to recover the full financial value of their asset after an accident. Whether navigating a complex Diminished Value claim or disputing a low-ball Total Loss offer, we provide the certified documentation needed to negotiate with insurance companies from a position of strength.

With a national reach and deep industry expertise, we have helped thousands of policyholders identify errors in carrier valuation reports (like CCC) and invoke the Appraisal Clause to secure fair settlements. We pride ourselves on transparency, speed, and reports that stand up to the toughest insurer scrutiny.

Why Trust This Guide

This guide was written and verified by the AutoAppraisalExpert technical team. Our appraisers specialize in total loss disputes and diminished value forensics. We stay current on state insurance regulations, court-accepted valuation practices, and evolving market trends to ensure our readers—and our clients—always have the most accurate information available.

Ready to see what your car is really worth? Get your free claim review today.