Is the check from your insurance company lower than you expected after they totaled your car? You’re not alone. That first offer can feel like a final, non-negotiable number, leaving you stressed about how you’ll afford a replacement vehicle.

Take a breath. That initial offer is not the final word—it’s the opening bid in a total loss settlement negotiation. This guide is designed by certified appraisal experts to show you how to challenge a lowball offer with evidence, level the playing field, and recover the fair settlement you’re owed.

Why Your Insurer’s First Offer Is a Starting Point for a Total Loss Settlement Negotiation

Insurance companies are billion-dollar businesses, and they use automated software to protect their bottom line. These systems, like CCC ONE, are programmed to produce conservative initial offers, often resulting in valuations thousands of dollars below your vehicle’s true market value. This is the “algorithm” myth: their software is a starting point, not a final authority.

Our goal is to help you close this value gap. We’ll walk you through how to build an iron-clad case for your car’s real Actual Cash Value (ACV). ACV is an industry term that simply means what your vehicle was worth right before the accident.

By using your own policy’s Appraisal Clause and irrefutable market data, you have the potential to turn a lowball offer into a fair settlement.

The Three Pillars of a Strong Total Loss Settlement Negotiation

When you get that valuation report, your job is to scrutinize it for inaccuracies. You are looking for three main things:

- Flawed Valuation Tools: Insurer systems have known biases. We’ll show you how to challenge their data with a real market valuation report.

- Unrealistic Market Data: Are they using stale listings from hundreds of miles away? You need to counter with real-world, dealer-sold comparables from your local market.

- Unfair “Condition Adjustments”: Adjusters often apply arbitrary deductions for minor wear and tear. These adjustments are baseless if your car was well-maintained.

A professional appraisal often uncovers an extra $1,000 to $5,000+ in value that adjusters overlook. Our reports provide the evidence needed to negotiate effectively. For a deeper look at the first steps, learn more about what happens when insurance totals your car.

Auditing the Insurance Company’s Valuation Report

The insurance company’s valuation report is the official foundation of their settlement offer. Don’t just glance at the final number. This document is your roadmap to finding the money they left on the table.

Your job is to audit this document for the common errors and flawed assumptions that lead to lowball offers. The entire report boils down to one number: your vehicle’s Actual Cash Value (ACV). ACV isn’t what you paid for the car or some generic Blue Book® Value from KBB.com. It is the fair market price someone would have paid for your exact car, in its pre-accident condition, right before the loss.

Where the Errors Hide: Decoding the “Comps”

The core of the insurer’s valuation is a list of so-called “comparable” vehicles, or “comps.” These are recently sold cars the system claims are similar to yours. This is where most valuation games are played.

Expert Insight: Insurer software is built for volume, not accuracy. The algorithms often pull comps from cheaper, distant markets or fail to account for unique options, creating a “value gap” that can easily cost you thousands.

To dissect their comps, ask the right questions:

- Geographic Mismatch: Are the comps from your local market? A car sold 200 miles away does not reflect the cost to replace your car in your neighborhood.

- Trim and Package Confusion: Did they get the trim level right? Misidentifying your fully-loaded Limited model as a base trim is a massive and frequent error.

- Questionable Mileage Adjustments: Look at how they adjust for mileage. We often see automated adjustments are far less than what the real-world market dictates.

- Stale Sale Dates: How old are these sales? Comps from six months ago don’t reflect today’s more expensive market.

Challenging Unfair Adjustments and Missing Options

Once the software picks its comps, it applies “condition adjustments.” This is another area ripe for dispute. If you kept your car in excellent shape, you must fight subjective downgrades.

Finally, go line-by-line through the options and equipment list. Did they include your panoramic sunroof or premium audio system? Every feature has value, and anything they miss is money out of your pocket.

For a deep dive, our guide on how to audit your CCC total loss report is essential reading. By methodically auditing the report, you start building a fact-based case. That’s how you begin a real total loss settlement negotiation.

Building Your Case with Real Market Evidence

You’ve audited the insurer’s report and pinpointed its flaws. Now, it’s time to go on the offensive. A successful total loss settlement negotiation isn’t won with complaints; it’s won with superior, evidence-based data.

Your goal is to paint a crystal-clear picture of what it would cost to buy a true replacement for your car in your local market, right now.

Finding True Replacement Vehicles

The foundation of your counter-offer is finding better “comparable” vehicles. The gold standard here is dealer-sold comps, as they represent the real-world retail price you would have to pay.

Here’s where you should be hunting for your own comps:

- Local Dealer Websites: Search online inventories of dealerships in your area for vehicles that are a close match.

- Major Listing Sites: Use platforms like Autotrader, Cars.com, and CarGurus. Set the search radius to your immediate market (within 50 miles) to keep the data relevant.

- Auction Sites (Use with Caution): For unique vehicles, sites like Cars & Bids or Bring a Trailer can be a goldmine.

For every comparable you find, save a PDF of the full vehicle listing. A simple link is not enough. Make sure your saved document includes the VIN, mileage, options, and the asking price.

Assembling Your Vehicle’s “Value Package”

Finding better comps is half the battle. The other half is proving the specific, unique value of your car. Compile a “value package”—a folder of documents that tells the story of your car’s life and condition.

Your value package should have:

- Maintenance Records: Every oil change and service record proves your car was well-maintained.

- Receipts for Recent Upgrades: Did you just put on new tires for $800? This adds direct, provable value.

- The Original Window Sticker: This is undeniable proof of every single option and package.

- Pre-Accident Photos: Clear, recent photos are powerful visual evidence of its condition.

This package transforms your car from a VIN in their software into a tangible, high-value asset.

Diminished Value vs. Total Loss

It’s crucial to know the difference between diminished value vs. total loss. A total loss claim pays for the entire pre-accident value of your car. A diminished value claim, which we break down in our guide on how to calculate diminished value after an accident, is for cars that are repaired.

You cannot claim both for the same incident. If your car is declared a total loss, the settlement is supposed to make you whole by covering its full value, period.

The Ultimate Weapon: A Professional Independent Appraisal

Doing your own homework is a great start. But if you want to bring the insurance company’s lowballing to a dead stop, nothing beats a formal appraisal from a certified, independent professional. An adjuster can’t easily dismiss a USPAP-compliant report built on certified appraisal methodologies.

Unlocking Your Secret Weapon: The Appraisal Clause

Buried in your auto policy is a tool you probably never knew you had: the Appraisal Clause. This is your contractual right to bring in your own independent auto appraiser when you and the insurer are at a stalemate.

Invoking this clause is a massive power shift. It yanks the dispute out of the adjuster’s hands and forces it into a formal, structured resolution process.

Expert Takeaway: Think of the Appraisal Clause as your policy’s built-in “second opinion” button. Pressing it forces the insurance company to engage with your evidence on a professional-to-professional level.

A professional report from an expert appraiser has the potential to uncover $1,000 to $5,000 or more in extra settlement money. This is the result of making precise adjustments for condition, mileage, and local market demand—details that automated systems are programmed to ignore.

Why a Professional Report Packs Such a Punch

An adjuster has a much harder time arguing with a USPAP-compliant report. USPAP (Uniform Standards of Professional Appraisal Practice) is the set of federal-level ethical and performance standards for our profession. A USPAP-compliant report is the gold standard, ensuring the valuation is objective and will hold up under scrutiny.

The practice of lowballing is a documented business model. A 2022 investigation by the UK’s Financial Conduct Authority found insurers systemically offered sums below fair market value, only increasing them after a formal complaint. This confirms a global truth: insurers start low. Our reports counter these tactics with data-driven proof. You can dig into these industry findings in this insightful analysis.

A certified appraisal delivers:

- A Certified Valuation: A professional conclusion backed by established methodology.

- Defensible Adjustments: Line-item adjustments based on actual market data.

- Irrefutable Comparables: Comps that are actually comparable to your vehicle.

When you invest in a car appraisal for an insurance claim, you’re buying leverage, credibility, and the professional firepower to secure the full value your policy promised.

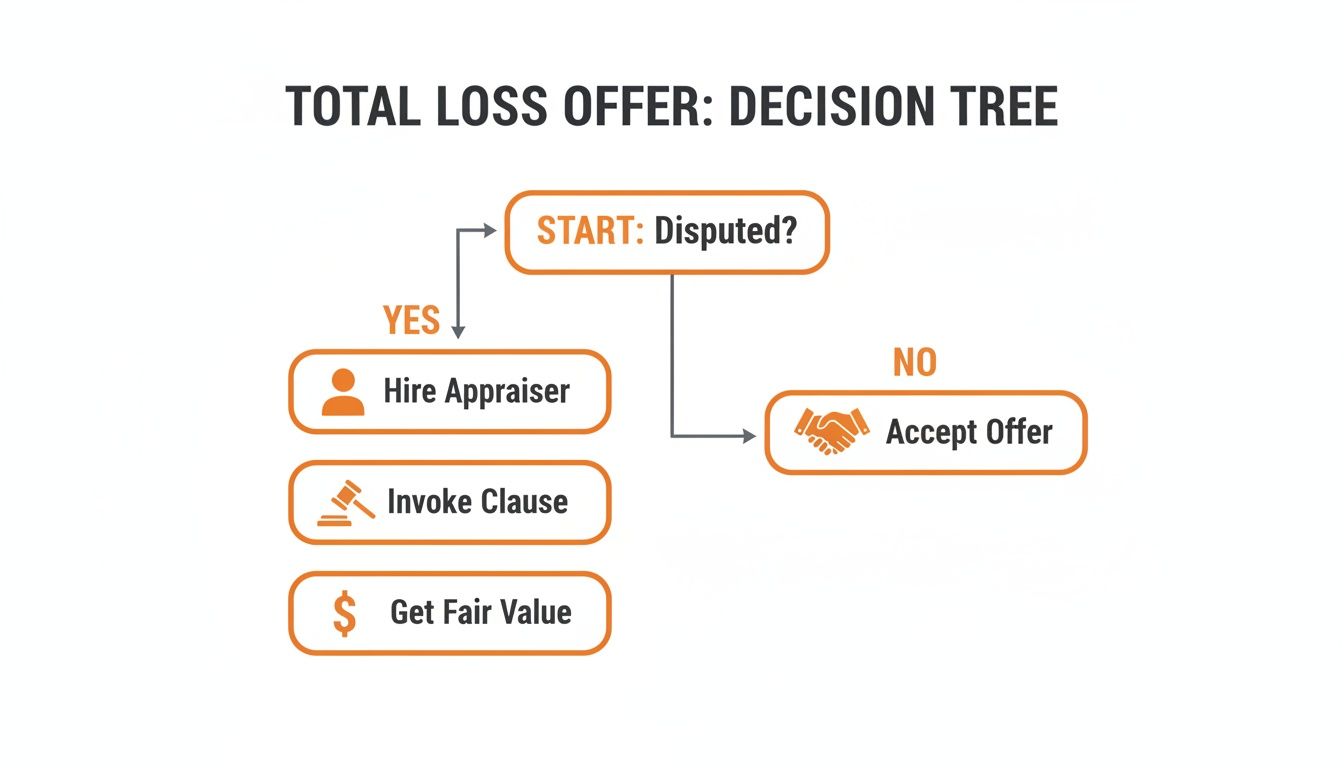

Executing Your Counteroffer Strategy

You’ve audited their lowball valuation, gathered market research, and have a certified independent appraisal. Now it’s time to present your business case. You are a proactive negotiator armed with undeniable facts.

The path forward is clear. This decision tree lays out your next move after receiving an unsatisfactory offer.

The moment you dispute the offer and bring in a professional, you put yourself on the path to recovering your vehicle’s true fair market value.

Making Your First Move: The Counteroffer

Your initial move should be a formal, written counteroffer sent via email. You want a documented paper trail. The tone should be firm, professional, and entirely driven by data.

Your email needs to accomplish three things:

- State Your Rejection and Demand: Clearly state you are rejecting their valuation and present your counteroffer—the value from your certified appraisal report.

- Attach the Proof: This is crucial. Attach your comparable vehicle listings, receipts, and most importantly, the complete, signed independent appraisal report from a trusted company like SnapClaim.

- Set a Timeline: Request a formal response within a reasonable timeframe, like 7-10 business days, to show you’re serious.

Use a direct and professional email subject line: “Counteroffer on Claim #[Your Claim Number] for [Your Name].” It sets a no-nonsense tone.

How to Handle Pushback

The adjuster will likely push back. A classic tactic is to dismiss your comps as “retail asking prices.” Your counter is your certified appraisal. A professional appraisal from a fair market value expert is built on industry-standard methodologies, not just online listings.

What if the adjuster stonewalls you? Politely request to speak with their direct supervisor. The frontline adjuster often has limited authority. Document every interaction.

If a manager gives you the same runaround, it’s time to use your trump card: The Appraisal Clause. Send a formal, written demand letter (certified mail is best) explicitly invoking this right. This action legally forces the dispute into a binding resolution process.

Getting Paid: The Final Steps

Once you agree on a number, the rest is paperwork. But read every line of the final settlement and release forms. Make sure the settlement amount is exactly what you agreed to.

Remember, the final check will be for the agreed-upon value minus your deductible. After you sign the release and transfer the title, the check is issued. The total loss settlement negotiation is officially over. You stood your ground and recovered the money you were rightfully owed.

How to Counter Common Insurer Negotiation Tactics

Insurance adjusters are trained professionals, and a total loss settlement negotiation is their home field. They have a playbook of tactics designed to make you accept less than you’re owed. Knowing their game is the first step to beating it.

The “Delay and Drag”

One of the most common tools is silence. They might go dark for days, hoping your frustration will lead you to accept any offer. This isn’t just poor customer service; it’s a strategy.

Your Counter-Move: You set the pace. After any phone call, send a polite follow-up email summarizing the conversation and outlining next steps. End with a clear action item: “Per our conversation, I expect your revised offer by Friday, October 28th.”

The “Incomparable Comparable”

The adjuster clings to their flawed “comparable” vehicles, even after you’ve handed them perfect, local examples. They’ll say, “Your comps are just asking prices,” or “Our system is state-approved.” This is a deflection.

Your Counter-Move: Don’t argue over their bad data. Pivot back to your strongest evidence: your certified independent auto appraiser‘s report.

Counter-Script: “I understand your report, but my claim’s value is based on the certified, USPAP-compliant market valuation report I provided. It was prepared by a licensed professional using court-accepted methods. Let’s focus on the evidence in that report.”

This reframes the negotiation. You are no longer debating their flawed software; you’re forcing them to contend with a professional, legally defensible valuation.

The “Phantom Damage” Claim

The adjuster insists your vehicle had significant “pre-existing damage” to justify heavy condition deductions. They’re gambling that you can’t prove them wrong.

Your Counter-Move: This is where your “value package” pays off. Present your complete maintenance history, receipts, and pre-accident photos. A certified appraisal from a firm like SnapClaim includes a detailed condition assessment that makes these baseless claims evaporate.

The Policy Misrepresentation

An adjuster might tell you that certain features aren’t covered or that you aren’t entitled to sales tax. They are banking on the fact you haven’t read your full insurance policy.

Your Counter-Move: Put the burden of proof back on them. Politely ask, “Can you show me where it says that in my policy? Please point me to the specific section.” More often than not, they can’t—because it doesn’t exist.

Total Loss Settlement Negotiation: Frequently Asked Questions

How long do I have to dispute a total loss?

Technically, you have until the statute of limitations runs out, which varies by state. However, momentum is critical. Act immediately. Do not cash the check from the insurer, as this can be seen as acceptance. Notify the adjuster in writing that you formally dispute their valuation.

What is the Appraisal Clause and how does it work?

The Appraisal Clause is your most powerful tool. It’s a provision in most auto policies for settling valuation disputes. If you and the insurer can’t agree on your vehicle’s Actual Cash Value (ACV), either party can invoke it.

Here’s how it works:

- You hire your own certified appraiser.

- The insurance company hires theirs.

- Those two appraisers agree on a neutral third-party expert, or “umpire.”

A binding decision is reached when any two of the three agree on a value. To start this process, send a formal written demand to your insurer invoking the clause.

Can I still negotiate if I owe money on my car?

Yes, and you absolutely must. The negotiation is about establishing your car’s fair market value; your loan is a separate issue. If your settlement is higher than your loan balance, you keep the difference. A thorough total loss settlement negotiation is crucial to shrink or eliminate any gap you might owe.

What is a total loss threshold and why should I care?

A total loss threshold is a legal benchmark, set by state law, that dictates when a vehicle must be declared a total loss. For example, a state with a 75% threshold means a car is totaled if repair costs exceed 75% of its pre-accident value. A lowball ACV completely skews this math, potentially forcing a total loss on a repairable vehicle, or vice-versa, based on an inaccurate valuation.

Don’t leave money on the table. Get your free claim review or order a certified appraisal report today to take control of your insurance settlement.

About AutoAppraisalExpert

AutoAppraisalExpert is a premier provider of independent vehicle appraisal reports and insurance claim consulting. Our mission is to equip vehicle owners with the data-driven evidence required to recover the full financial value of their asset after an accident. Whether navigating a complex Diminished Value claim or disputing a low-ball Total Loss offer, we provide the certified documentation needed to negotiate with insurance companies from a position of strength.

With a national reach and deep industry expertise, we have helped thousands of policyholders identify errors in carrier valuation reports (like CCC) and invoke the Appraisal Clause to secure fair settlements. We pride ourselves on transparency, speed, and reports that stand up to the toughest insurer scrutiny.

Why Trust This Guide

This guide was written and verified by the AutoAppraisalExpert technical team. Our appraisers specialize in total loss disputes and diminished value forensics. We stay current on state insurance regulations, court-accepted valuation practices, and evolving market trends to ensure our readers—and our clients—always have the most accurate information available.

Ready to see what your car is really worth? Get your free estimate today.