Is your insurance company’s settlement offer feeling suspiciously low? You’re not alone. The thought of spending money on an auto appraisal can seem counterintuitive when you’re already facing a financial loss. But a professional appraisal isn’t a cost—it’s a strategic investment, and often the only tool that gives you the evidence needed to negotiate for the thousands of dollars the insurer is trying to keep. The auto appraisal cost is your key to leveling the playing field.

Your Guide to Appraisal Costs and Value

Let’s be clear: when an insurer hands you a market valuation report, their goal is to protect their bottom line, not to be fair to you. That report is generated by software and adjusters working for them, and it almost always undervalues your vehicle compared to real-world, local market data. The number they give you is a starting point for their negotiation, not the final word on what your car is worth.

This is precisely where hiring an independent auto appraiser flips the script. The question quickly changes from “What does an auto appraisal cost?” to “How much money am I leaving on the table without one?” A professional appraisal provides the evidence needed to negotiate from a position of strength.

How a Small Fee Can Unlock a Bigger Payout

The auto appraisal cost is a fixed, upfront fee that is small when you compare it to the potential gains. Our reports often provide the evidence needed to help clients negotiate an additional $1,000 to $5,000, and sometimes much more. It’s the hard evidence you need to fight back in two main scenarios:

- Diminished Value: Your car was repaired after an accident, but it’s now worth less simply because it has a wreck on its record.

- Total Loss: The insurance company declared your car a total loss, and their payout offer isn’t enough to buy a comparable replacement.

What surprises most people is how affordable a professional appraisal is. For example, specialized classic car appraisals can run between $300 and $500. For everyday insurance claims, the auto appraisal cost is often in that same range or even lower, representing a tiny fraction of the money at stake. You can get more details on appraisals for unique cars from experts like Waimak Valuations.

Leveling the Playing Field Against Insurers

An independent appraisal isn’t just about a bigger check; it’s about gaining leverage. Insurance companies are massive corporations with teams trained to minimize payouts. Your appraisal is the professional-grade, USPAP-compliant evidence that forces them to listen.

To help you see the value clearly, here’s a quick breakdown of typical costs versus the potential returns.

Typical Auto Appraisal Cost vs. Potential Settlement Increase

| Appraisal Type | Typical Cost Range | Average Potential Settlement Increase |

|---|---|---|

| Diminished Value | $300 – $550 | $1,000 – $5,000+ |

| Total Loss | $350 – $600 | $1,500 – $7,500+ |

As you can see, a modest investment in a professional report has the potential to yield a significant return. By investing in a USPAP-compliant appraisal—meaning it adheres to certified appraisal methodologies—you are arming yourself with a data-driven document that stands up to insurer scrutiny.

Our fee structure is completely transparent, and you can see a full breakdown by reviewing our pricing. Think of it as the key that unlocks the true value of your claim and gives you the power to fight for the settlement you rightfully deserve.

What Factors Influence the Auto Appraisal Cost?

When you get a quote for a professional car appraisal, you’re not just paying for a number. You’re investing in a meticulously researched, evidence-based report designed to stand up to an insurance company’s army of adjusters. The cost reflects the time, expertise, and deep-dive research needed to build an ironclad case for your car appraisal for insurance claim.

The Type of Appraisal You Need

The single biggest factor is the kind of claim you’re fighting. A diminished value appraisal and a total loss appraisal are two completely different services, requiring different evidence and methodologies.

- Diminished Value Appraisals: This is about proving your car lost resale value because of its accident history. The appraiser digs into market data and scrutinizes repair quality to calculate that “stigma” loss. You can learn more at SnapClaim’s Diminished Value resource.

- Total Loss Appraisals: Here, the goal is to prove your car’s Actual Cash Value (ACV)—a term for what it was worth the second before the crash. The appraiser audits the insurer’s lowball offer and builds a powerful counter-valuation using real, local, dealer-sold comparable vehicles.

The Complexity and Uniqueness of Your Vehicle

A run-of-the-mill sedan is easier to value than a rare or heavily modified vehicle. The more unique your car, the more time and expertise it takes to pin down its true market value.

Complexity drivers include:

- Specialty Vehicles: Trucks with aftermarket lift kits, classic cars, imported models, or limited-edition sports cars all require extra research.

- High-End Luxury or Exotic Cars: Valuing these machines requires an expert who understands niche market trends.

- Extent of Damage: For diminished value vs. total loss considerations, severe structural damage requires a much more intensive analysis to document the loss in value correctly.

The Depth of the Report and Supporting Evidence

You’re not buying an opinion; you’re buying proof. A report that can make an adjuster sweat must be loaded with documentation. A quick online estimate from a site like KBB.com, while useful for a ballpark idea, is not the evidence an insurer is forced to acknowledge.

A professional appraisal report is a USPAP-compliant document. This means it follows the Uniform Standards of Professional Appraisal Practice, the industry’s gold standard for ethics and performance. It turns your claim from an opinion into a tool that insurers have to take seriously. The cost reflects the real-world legwork an independent auto appraiser does—work that automated systems can’t.

This includes contacting dealership sales managers to verify the actual selling prices of comparable cars, not just the list price. It means analyzing your car’s specific condition and writing a clear narrative that explains exactly why the insurer’s offer is wrong. This is the level of detail that gives your claim leverage and builds the foundation for a settlement based on true fair market value.

Diminished Value vs. Total Loss Appraisals

While several factors influence the final auto appraisal cost, the biggest driver is the reason you need one. After an accident, you’re usually fighting one of two major battles against an insurance company: a Diminished Value claim or a Total Loss dispute. Understanding which battle you’re in is the first step, because each one requires a unique report and expert strategy.

Proving Inherent Diminished Value

A Diminished Value (DV) claim is about recovering the resale value your car lost just because it now has an accident history. Even with flawless repairs, that vehicle is permanently “stigmatized.” An independent appraiser proves this loss by:

- Quantifying the Stigma: We dig into real-world market data, showing exactly how much less comparable vehicles with accident histories are selling for.

- Analyzing Repair Severity: Frame damage causes a much steeper drop in value than a simple bumper replacement.

- Applying Proven Methodologies: In some cases, insurers try to use a flawed calculation like the 17c Formula—a simplified, often inaccurate method to estimate diminished value. A true appraisal goes much deeper to reflect genuine market conditions.

A DV appraisal can provide the hard evidence needed to show that your expertly repaired $30,000 SUV has lost $4,500 in real-world market value—a loss the insurer would otherwise ignore.

Disputing a Low Total Loss Offer

A Total Loss happens when an insurer decides the cost to fix your car is more than it was worth right before the crash. This is often determined by a state’s total loss threshold—a set percentage of the car’s value. Instead of paying for repairs, the insurer cuts you a check for its Actual Cash Value (ACV), and this is where the fight begins.

That ACV offer is almost always generated by software like CCC ONE, which has a reputation for producing low valuations to save the insurance company money. An expert total loss appraisal acts as a direct audit of their offer. It’s a data-driven counter-offer built on real, local market evidence—not a cost-saving algorithm.

A professional appraiser fights back by:

- Auditing Their Report: We tear down the insurer’s CCC ONE report, hunting for errors like using out-of-state “comparable” vehicles or missing valuable factory options.

- Finding Real-World Comps: We build our counter-valuation using actual vehicles for sale at dealerships in your local market.

- Certifying a Higher Value: Our USPAP-compliant report explains exactly why your vehicle is worth more than their software claims.

Let’s say an insurer offers you $18,000 for your totaled sedan. A professional appraisal can provide the proof to show its true ACV is closer to $22,000, giving you the leverage you need.

Why the Insurer’s Valuation Is Just an Algorithm

When you get that market valuation report from the insurance company, it looks official and final. But you must understand what it really is: the insurer’s opening offer in a negotiation, created by software like CCC ONE to protect their bottom line, not yours. This is the “Algorithm Myth”—the idea that their software is a flawless, impartial judge of value.

The truth? These programs are built to close claims as cheaply as possible. They often use flawed data that fails to capture your car’s true Actual Cash Value (ACV)—an industry term for what your vehicle was worth the moment before the accident.

Spotting the Cracks in Their Automated Report

A certified independent auto appraiser knows exactly where to find the mistakes in these reports. The most common flaws are:

- Bad Comps: Using vehicles from other states or old sales that don’t reflect your local market today.

- Unfair Condition Hits: Applying steep, arbitrary deductions for minor “wear and tear.”

- Missing Features: Overlooking valuable factory options and trim packages you paid for.

As repair costs rise, insurers are quicker to declare a car a total loss, making independent valuations more critical than ever. You can read more about how market trends are impacting appraisals.

Your Secret Weapon: The Appraisal Clause

So, how do you fight back? You use the rules they wrote themselves. Buried in the fine print of almost every auto policy is a powerful tool called the Appraisal Clause.

The Appraisal Clause is your contractual right to dispute the insurance company’s valuation. It allows you to hire your own certified appraiser to present an independent valuation, forcing the insurer to negotiate based on facts.

Invoking this clause changes the game. It yanks power away from the adjuster’s software and puts it back into the hands of human experts who use real-world evidence.

How an Expert Closes the Value Gap

The auto appraisal cost is a tiny investment for this massive shift in leverage. A certified appraiser uses the gold standard: real-time, dealer-sold comparable vehicles.

- We identify recently sold vehicles that are a true match for yours.

- We contact dealership managers to confirm the actual transaction prices.

- We build a USPAP-compliant report that documents this evidence.

This evidence-based approach is what closes the “value gap” and frequently provides the evidence needed to negotiate for an extra $1,000 to $5,000+. It forces the insurance company to abandon its algorithm and deal with the factual, fair market value of your vehicle. While public data from a source like the NHTSA.gov provides a good foundation, it’s just the start.

Calculating Your Potential Return on Investment

It’s natural to hesitate before spending more money. But looking at the auto appraisal cost isn’t about spending—it’s about recovering. The right question isn’t “Can I afford an appraisal?” It’s “Can I afford to let the insurance company keep thousands of dollars that rightfully belong to me?” Thinking about the return on investment (ROI) makes the decision purely strategic.

A Simple Checklist for Your Decision

You should strongly consider an appraisal if:

- The Insurer’s Offer Feels Wrong: If you can’t find a truly comparable replacement vehicle for the amount they’re offering, their number is probably wrong.

- Your Vehicle Was Newer or in Excellent Condition: Insurer software is notoriously bad at valuing low-mileage or meticulously maintained vehicles.

- Your Vehicle Had Significant Damage: For a diminished value claim, any repair involving the frame, structure, or airbags creates a massive stigma that insurers rarely acknowledge without proof.

- You’re Dealing with a Difficult Adjuster: If the adjuster is just repeating “the system says…”, a formal, USPAP-compliant report forces them to engage with real-world evidence.

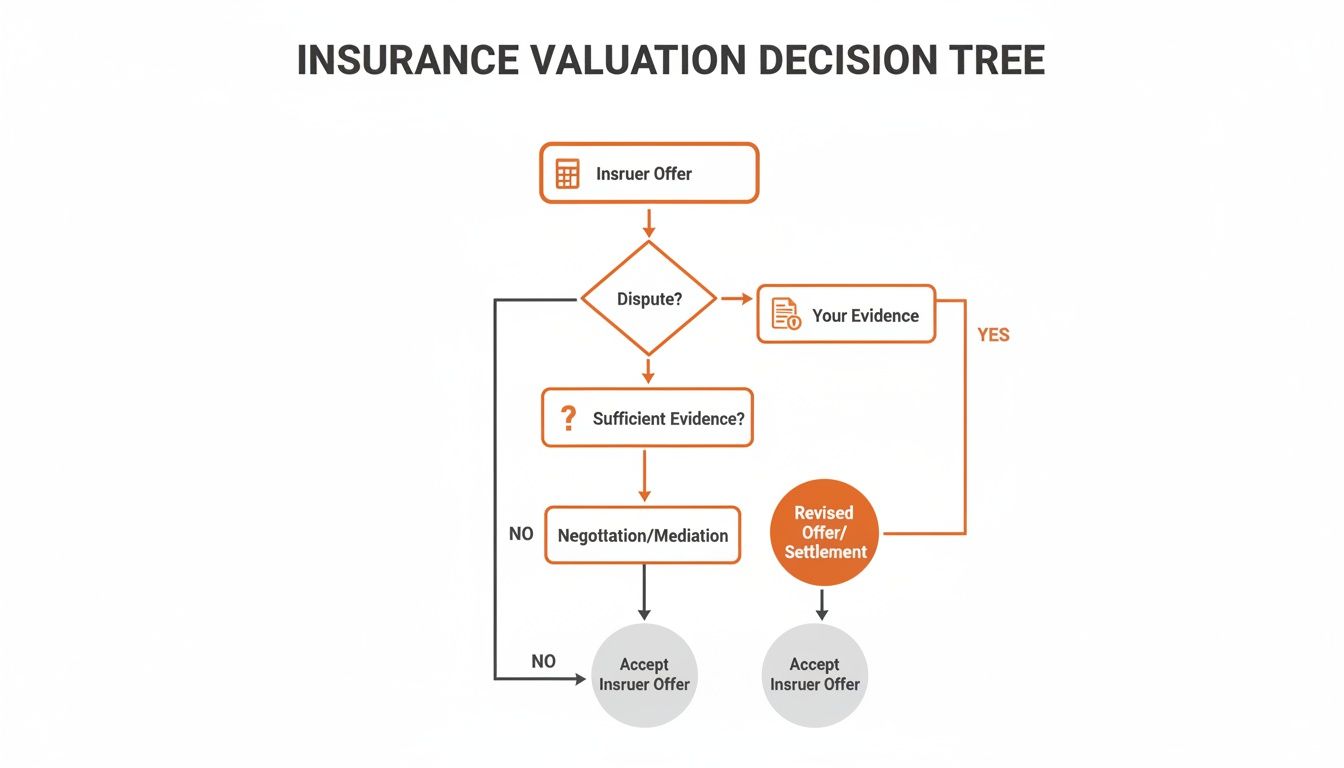

This flowchart maps out the thought process. Notice how everything hinges on your decision to challenge the first offer with credible evidence of your own.

The path to a fair settlement starts the moment you decide their first offer isn’t the final word.

Seeing the ROI in Action: A Case Study

Let’s put this into real-world numbers. Take Sarah, who owned a three-year-old SUV that was totaled. Her insurance company’s CCC report offered $24,000. She knew that felt low; she couldn’t find a similar vehicle for less than $28,000.

She invested $395 in a certified total loss appraisal from an independent auto appraiser. Our appraiser found the flaws—they used out-of-state “comps” and missed her premium options package. The final certified value was $28,500. Armed with our report, Sarah invoked the Appraisal Clause. The insurance company agreed to the higher valuation.

Sarah’s net gain was $4,105 ($28,500 settlement – $24,000 initial offer – $395 appraisal cost). Her investment had the potential to pay for itself more than 10 times over.

While we can never guarantee a specific outcome, our reports consistently provide the evidence needed to negotiate for $1,000 to $5,000+ in value that adjusters hope you won’t notice, making the auto appraisal cost a powerful investment.

How to Use Your Appraisal Report to Win Your Claim

Armed with a professional appraisal, you’re no longer just disagreeing with the insurance company—you’re challenging them with hard facts. This report isn’t just paper; it’s leverage. You are presenting a formal, evidence-backed valuation that the insurance company is obligated to consider.

Submitting Your Report to the Adjuster

Your first move is simple: email a full copy of the appraisal report directly to the adjuster. Keep the email polite but firm. State that you are formally disputing their valuation and presenting your independent appraisal as evidence of the vehicle’s true Actual Cash Value (ACV)—the industry lingo for what your vehicle was worth right before the accident.

This single action changes the dynamic. The adjuster can no longer just point to a number on their screen. They now have a USPAP-compliant report in their hands, a document built on certified, professional methodologies that they must address.

Invoking the Appraisal Clause

What if the adjuster ignores your report? It’s time to play your trump card: the Appraisal Clause. This is a provision in almost every auto insurance policy giving you the right to settle a value dispute with independent experts.

Invoking the Appraisal Clause is a formal process that forces a structured negotiation. It’s the ultimate tool for leveling the playing field against a billion-dollar insurer.

You trigger this by sending a formal, written letter to the insurance company. This escalates the dispute beyond the individual adjuster, compelling the carrier to engage with the facts in your report. You can learn more about what happens when insurance totals your car and how to respond effectively. This process shifts the power back to you.

Frequently Asked Questions About Auto Appraisal Cost

After an accident, you’re stressed and you have questions. We get it. We’ve built our business on providing the answers that help you get paid fairly.

How long do I have to dispute a low total loss offer?

Most states have a statute of limitations for property damage claims, often two to four years, but you should never wait. The best time to challenge a low offer is immediately. Acting fast preserves evidence and shows the insurance company you are serious about a fair settlement.

Is the auto appraisal cost worth it for a small difference?

If an insurer’s offer is $1,500 below fair market value, spending a few hundred dollars on a certified report is a smart financial move. Our reports often provide the evidence needed to negotiate for $1,000 to $5,000+ in additional value, meaning the appraisal has the potential to pay for itself many times over.

Can I get an appraisal after I cash the insurance check?

You can, but it makes your life harder. Cashing their check often implies you’ve accepted their offer as “payment in full.” While some states let you cash a check “under protest,” your strongest negotiating position is before any money changes hands. Get your independent appraisal first.

What makes a professional appraisal different from KBB?

Sites like Kelley Blue Book give you a ballpark estimate—they are not evidence. An independent appraisal is a USPAP-compliant legal document, built by a certified expert using real, local, dealer-sold cars to prove your vehicle’s true Actual Cash Value (ACV). This documented proof is what forces an adjuster’s hand.

Don’t leave money on the table. Get your free claim review or order a certified appraisal report today to take control of your insurance settlement.

About AutoAppraisalExpert

AutoAppraisalExpert is a premier provider of independent vehicle appraisal reports and insurance claim consulting. Our mission is to equip vehicle owners with the data-driven evidence required to recover the full financial value of their asset after an accident. Whether navigating a complex Diminished Value claim or disputing a low-ball Total Loss offer, we provide the certified documentation needed to negotiate with insurance companies from a position of strength.

With a national reach and deep industry expertise, we have helped thousands of policyholders identify errors in carrier valuation reports (like CCC) and invoke the Appraisal Clause to secure fair settlements. We pride ourselves on transparency, speed, and reports that stand up to the toughest insurer scrutiny.

Why Trust This Guide

This guide was written and verified by the AutoAppraisalExpert technical team. Our appraisers specialize in total loss disputes and diminished value forensics. We stay current on state insurance regulations, court-accepted valuation practices, and evolving market trends to ensure our readers—and our clients—always have the most accurate information available.

Ready to see what your car is really worth? Get your free estimate today.