Is your insurance company’s settlement check shockingly lower than you expected? You’re not alone. This isn’t just a miscalculation; it’s a common tactic used by insurers. Fortunately, you have a powerful contractual right to fight back: the insurance claim appraisal. This is your single best tool for disputing a low-ball total loss offer and securing the full value you’re legally owed.

Why Your Insurer’s First Offer Is Rarely Their Best (And How to Dispute It)

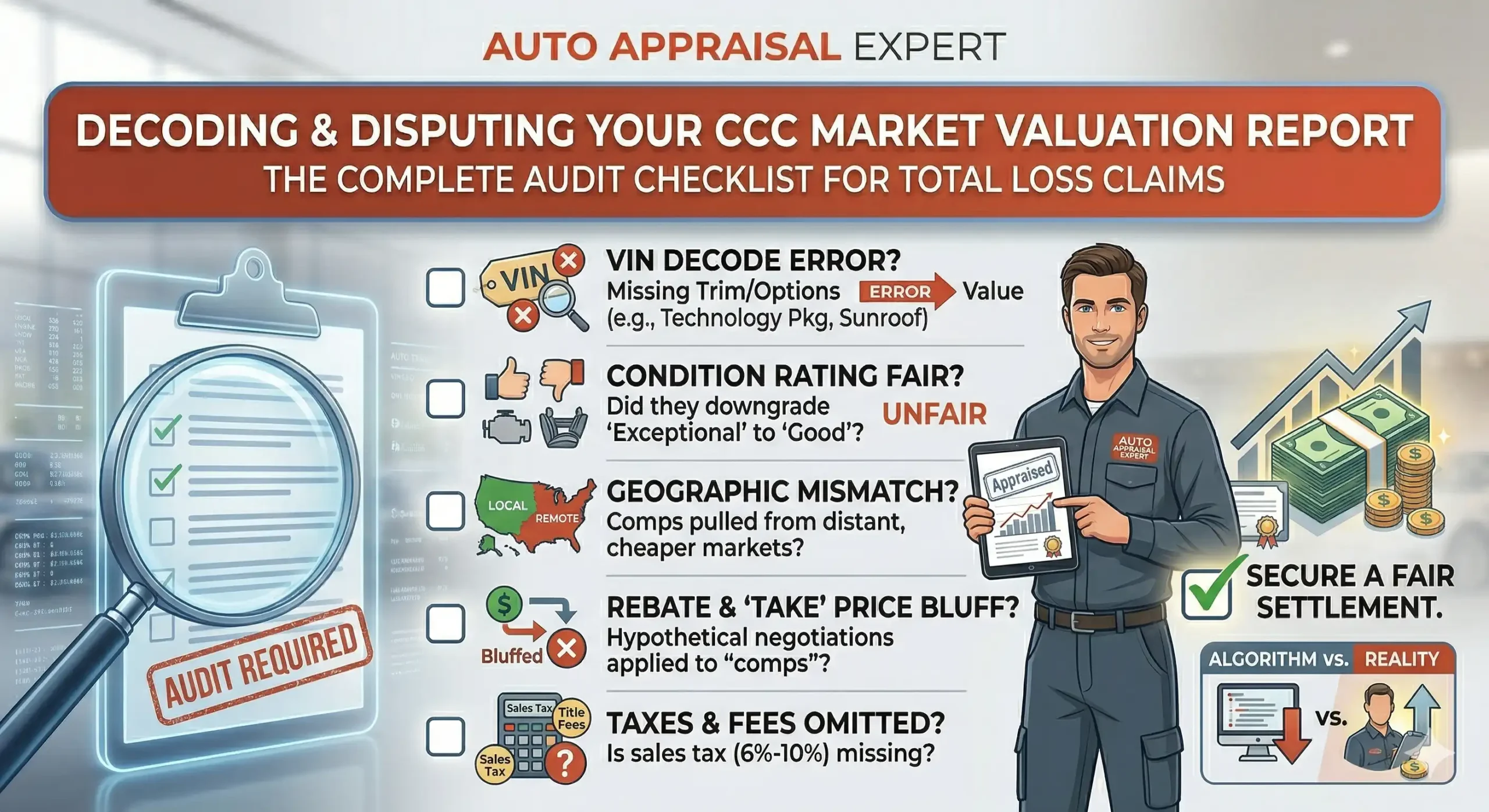

When an insurer declares your car a total loss, their first offer is not an act of fairness; it’s a number generated by software designed to protect their bottom line. Carriers almost universally use automated valuation tools like CCC ONE. While these systems provide a starting point, they are just an algorithm—and they are notorious for using questionable comparables, outdated data, and missing valuable options on your vehicle.

This flawed process creates a significant “value gap”—the difference between the insurer’s software-driven offer and your car’s true Actual Cash Value (ACV). The ACV is the price your vehicle would have sold for on the open market one minute before the collision. A professional appraisal often uncovers an additional $1,000 to $5,000+ in hidden value, providing the evidence needed to negotiate a higher settlement.

You Have the Right to an Independent Appraisal

Here’s the secret insurance companies hope you don’t discover: you are not stuck with their low offer. Buried in the fine print of most auto policies is a powerful provision called the Appraisal Clause. This is your contractual right to dispute the insurer’s valuation by hiring your own independent auto appraiser.

Invoking the Appraisal Clause is not starting an argument; it’s exercising a right you already paid for in your premiums. It levels the playing field, forcing the insurance company to negotiate based on real-world market facts, not just their internal software.

This clause allows you to present a fact-based, USPAP-compliant report built on verifiable, dealer-sold comparables—the gold standard for winning settlement disputes. It shifts the conversation from your opinion versus their algorithm to a debate over documented evidence. That’s how you gain the leverage needed to secure a fair market value for your vehicle.

Total Loss vs. Diminished Value: Which Insurance Claim Appraisal Do You Need?

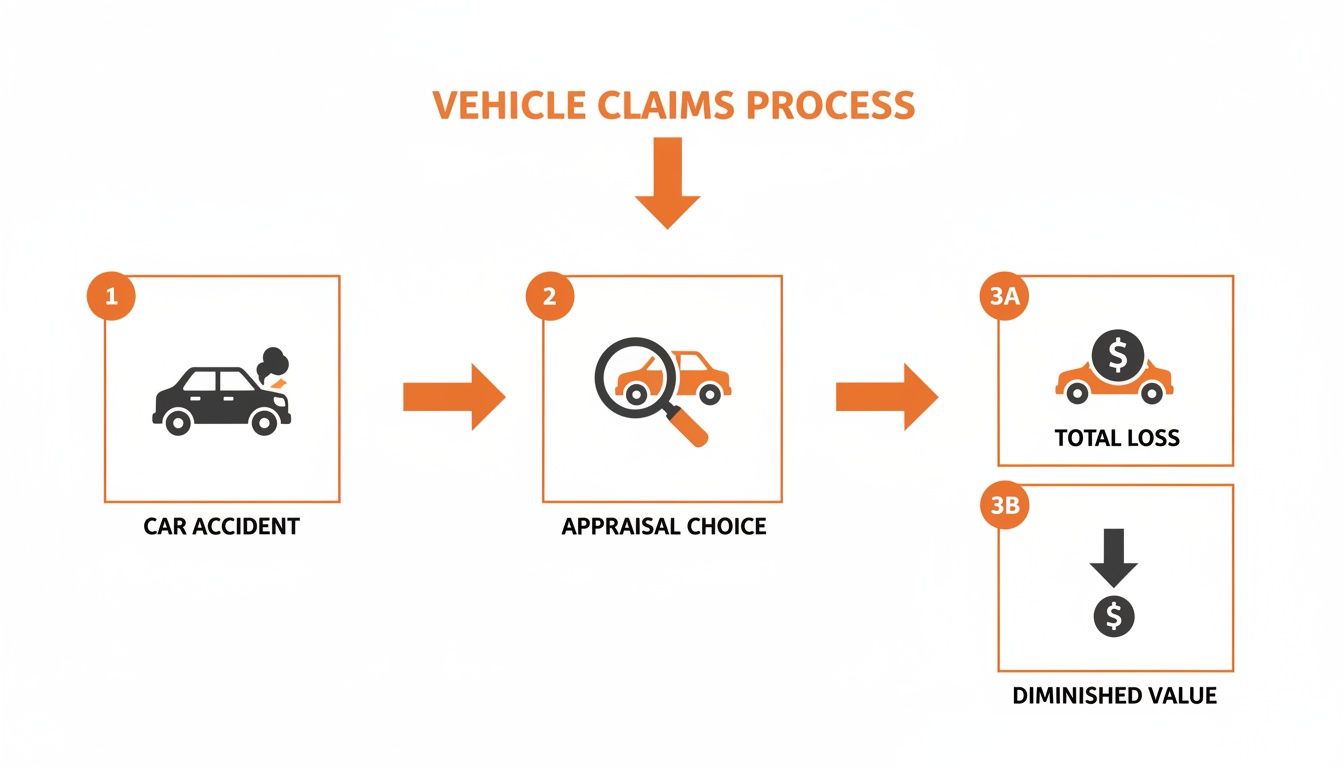

After an accident, your claim can go down two very different paths, depending on the severity of the damage. Understanding the difference between a total loss and diminished value is the first step to recovering the money you are owed. Each addresses a unique financial loss, and insurers handle them very differently.

Total Loss Appraisal: For Cars Beyond Repair

A vehicle is declared a total loss when the cost to repair it exceeds a certain percentage of its pre-accident value. This is known as the total loss threshold, a rule that varies by state. Once totaled, the insurer owes you the vehicle’s Actual Cash Value (ACV). This is where the dispute usually begins, as their initial offer is often based on flawed software reports.

An effective insurance claim appraisal counters this by providing a professional market valuation report. This USPAP-compliant document uses real, verifiable sales data for cars just like yours, creating a true, evidence-based ACV. This step alone has the potential to increase your settlement by thousands. If you’re in this situation, understanding what happens if insurance totals your car is essential.

Diminished Value Appraisal: For Repaired Cars

What if your car isn’t totaled? Even with flawless repairs, your vehicle is now permanently branded with an accident history on reports like CarFax, which sinks its resale value. This inherent loss of market worth is called diminished value.

Insurers rarely volunteer to pay for diminished value. They will cover the cost of repairs but often ignore the financial dent to your asset’s value. A diminished value appraisal is the specialized tool used to calculate this specific loss. It provides the hard evidence needed to demand full compensation from the at-fault party’s insurance for this hidden damage through a process called Subrogation, which is your insurer’s right to pursue the at-fault party’s insurance to recover money paid out.

Diminished Value vs. Total Loss: Key Differences

It can be confusing, so this table breaks down the core differences to help you identify your claim type.

| Factor | Total Loss Claim | Diminished Value Claim |

|---|---|---|

| Vehicle Status | The car is not repairable or repair costs exceed the state's total loss threshold. | The car IS repairable and has been (or will be) fixed. |

| What You're Claiming | The full pre-accident Actual Cash Value (ACV) of the entire vehicle. | The loss in market resale value caused by the accident history. |

| When It's Paid | Paid instead of repairs. The insurer typically takes ownership of the vehicle. | Paid in addition to repair costs. You keep the repaired vehicle. |

| Common Insurer Tactic | Using flawed software (like CCC ONE) to generate a low ACV offer. | Denying the claim exists or using a bogus "17c Formula" to offer a tiny payout. 17c is a generic, unscientific calculation insurers use to minimize diminished value payouts. |

| Your Goal | To recover the true market cost to replace your exact vehicle. | To be compensated for the financial stigma that hurts your car's resale value. |

Whether your car is a total loss or has been repaired, the insurer’s goal is to pay as little as possible. An independent appraisal is the key to forcing them to pay what’s fair.

How to Formally Invoke the Appraisal Clause

When the insurance company gives you a low-ball offer, it’s time to shift from defense to offense. Your policy’s Appraisal Clause is the most effective way to take control of the settlement process. You don’t need a lawyer to start; you just need to follow the correct procedure.

The 3 Steps to Force a Fair Valuation

- Send a Formal Written Dispute: Notify your adjuster in writing (email is fine, but certified mail is better) that you formally dispute their settlement offer and the valuation report it’s based on. Crucially, do not cash any checks they send for the vehicle, as this can be seen as accepting their offer.

- Explicitly Invoke the Clause: In the same communication, state: “I am invoking the appraisal clause of my policy.” This legal trigger obligates them to participate in the dispute resolution process outlined in your policy.

- Hire a Certified Independent Appraiser: This is your most important move. Select a qualified professional to conduct an insurance claim appraisal on your behalf. This expert will build the evidence-based case needed to fight for your vehicle’s true value.

Expert Insight: The credibility of your entire case rests on your appraiser’s report. Ensure it is USPAP-compliant. USPAP (Uniform Standards of Professional Appraisal Practice) is the federally recognized set of quality standards for professional appraisals, ensuring your report can withstand insurer scrutiny.

This professional-grade evidence is more critical than ever. As detailed in this analysis on insurance valuation trends, independent appraisers are essential for bridging the gap between outdated insurer data and current, real-world market prices.

What a Professional Car Appraisal for an Insurance Claim Includes

An insurer’s valuation from software like CCC ONE is a generic estimate—a low starting point for negotiation. A professional car appraisal for an insurance claim is a piece of defensible evidence built to prove your vehicle’s true worth. This is why a proper report from SnapClaim regularly helps clients negotiate for $1,000 to $5,000 or more in value that the adjuster’s software overlooked.

Core Components of a Certified Report

A USPAP-compliant report from a provider like SnapClaim leaves no room for doubt. It methodically proves your vehicle’s value using verifiable data. Here’s what’s inside:

- Detailed Vehicle Documentation: We document your vehicle’s specific condition, options, packages, maintenance history, and even recent upgrades.

- Precise Value Adjustments: The report applies specific dollar adjustments for factors like low mileage, excellent condition, or rare options that automated systems often miss.

- Hyper-Local Market Analysis: We find actual dealer-sold comparable vehicles from your local market—not just online listings—to establish a true baseline value reflecting what people are actually paying for cars like yours.

- Transparent Value Calculation: The report clearly shows the math, starting with real-world comps and applying documented adjustments to arrive at a final, defensible Fair Market Value.

This data-driven approach is the polar opposite of an insurer’s automated report. While consumer tools like KBB.com are a good starting point, a certified appraisal uses dealer sales data to prove value. You can see more on this process in our guide on how to calculate diminished value.

Why This Evidence Is So Powerful in 2026

Solid, third-party evidence has never been more critical. Claims processing is overwhelmed, with adjusters often managing 150-200 claims at once. Your case simply won’t get the individual attention it deserves.

A professional report cuts through the noise and forces the adjuster to justify their low offer against a mountain of credible evidence. According to recent industry trends on JDPower.com, a well-documented claim is key to a fair and timely settlement.

Navigating State-Specific Rules for Your Claim

Insurance is regulated at the state level, meaning the rulebook for your insurance claim appraisal changes depending on where you live. Knowing these local regulations gives you a powerful advantage.

One of the most important rules is your state’s total loss threshold. This law dictates when a car must be declared a total loss. In some states, it’s when repair costs hit 75% of the car’s pre-accident value; in others, the formula is different.

Timelines and Expectations

Hiring an independent auto appraiser is fast—you can often get a certified report within days. The real test of patience begins once you submit that appraisal to the insurer. They will need time to review it, and the negotiation process can take several weeks. The goal isn’t just to be fast; it’s to be right.

Key Takeaway: You must do your homework. Check with your state’s Department of Insurance for specific regulations. For a complete guide, see our breakdown of the total loss threshold by state.

FAQ: Your Insurance Claim Appraisal Questions Answered

When you’re fighting an insurance company, the process can feel confusing and overwhelming. Here are straightforward answers to common questions to help you move forward with confidence.

How long do I have to dispute a total loss offer?

Time is not on your side. Every state has a time limit, or statute of limitations, for property damage claims. Most importantly, never cash the settlement check. Cashing it can be legally interpreted as accepting their offer. Immediately notify the adjuster in writing that you are formally disputing their valuation.

How much does an independent auto appraiser cost?

A certified, USPAP-compliant appraisal report typically costs a few hundred dollars. Think of it as an investment. A professional market valuation report often provides the evidence needed to negotiate for $1,000 to $5,000+ more than the insurer’s initial offer. This can result in a significant return on your investment.

Can I use an appraisal for a third-party claim?

Yes. When another driver is at fault, you file a third-party claim against their insurance. You have the same right to be made whole, and their carrier must pay the fair market value for your damages. An independent appraisal is a powerful, unbiased tool in this scenario, like those offered by SnapClaim’s Diminished Value services, that the at-fault insurer cannot easily dismiss.

What if the insurance company rejects my appraisal?

An insurance company cannot simply “reject” a professional, USPAP-compliant appraisal report. Your auto policy’s Appraisal Clause outlines a formal process for settling valuation disputes. If your appraiser and the insurer’s appraiser cannot agree, a neutral “umpire” is brought in to make a final, binding decision. A professionally prepared report provides the undeniable evidence needed to win that negotiation.

Don’t leave money on the table. Get your free claim review or order a certified appraisal report today to take control of your insurance settlement.

About AutoAppraisalExpert

AutoAppraisalExpert is a premier provider of independent vehicle appraisal reports and insurance claim consulting. Our mission is to equip vehicle owners with the data-driven evidence required to recover the full financial value of their asset after an accident. Whether navigating a complex Diminished Value claim or disputing a low-ball Total Loss offer, we provide the certified documentation needed to negotiate with insurance companies from a position of strength.

With a national reach and deep industry expertise, we have helped thousands of policyholders identify errors in carrier valuation reports (like CCC) and invoke the Appraisal Clause to secure fair settlements. We pride ourselves on transparency, speed, and reports that stand up to the toughest insurer scrutiny.

Why Trust This Guide

This guide was written and verified by the AutoAppraisalExpert technical team. Our appraisers specialize in total loss disputes and diminished value forensics. We stay current on state insurance regulations, court-accepted valuation practices, and evolving market trends to ensure our readers—and our clients—always have the most accurate information available.

Ready to see what your car is really worth? Get your free estimate today.