Meta Title: Classic Car Worth Estimate Guide. Dispute Low Offers

Meta Description: Need a classic car worth estimate? Learn how to dispute low insurance offers and build a stronger valuation case today.

Your insurer says your classic is worth less than expected, and the number looks like it came from the same process used for an ordinary used car. That’s the moment many owners realize the valuation fight isn’t about sentiment. It’s about evidence.

A proper classic car worth estimate has to account for things standard insurance tools often miss, especially in a total loss dispute or when establishing pre-loss value for a repaired vehicle. If you’re dealing with Actual Cash Value, that means the carrier’s opinion of market value at the time of loss. In practice, the fight is usually over what “market” they chose and what evidence they ignored.

Why a Standard Value Report Fails Your Classic Car

The biggest mistake in a classic car claim is treating the insurer’s software output like a final answer. It isn’t. It’s a starting point.

That matters because the U.S. collector car market holds an estimated $1 trillion in total insurable value across about 43 million vehicles, representing roughly 16% of the nation’s 275 million registered vehicles, according to American Collectors Insurance’s market overview. In a market that large, a weak valuation method doesn’t create a small error. It can create a major gap between the carrier’s number and the vehicle’s real-world value.

The algorithm myth

Insurers often rely on valuation systems that work reasonably well for late-model, high-volume vehicles. Those systems struggle when the car’s value depends on scarcity, originality, restoration quality, or documented history.

A standard report tends to flatten the details that make classics valuable. It may identify the right year and model, yet miss the specific trim, engine, provenance, restoration standard, or period-correct components that separate one example from another.

Practical rule: If the report reads like your classic could be swapped with any other car of the same year and nameplate, it probably isn’t capturing actual collector value.

That’s why owners get blindsided. The insurer calls it market value. The owner sees a number built from broad assumptions.

What standard reports usually miss

For a classic, value is rarely just “year, make, model, mileage.” A defensible valuation usually turns on details like these:

- Originality matters: Matching numbers, factory paint, original sheet metal, and authentic trim can move value materially.

- Condition must be graded: “Good for its age” is not an appraisal standard.

- Documentation counts: Service records, ownership history, judging sheets, awards, and restoration invoices can support value.

- Rarity changes the analysis: Limited production or unusual factory configurations narrow the pool of true comparables.

- Storage and preservation matter: Indoor climate-controlled preservation tells a different story than long-term outdoor storage.

Why ACV fights get tilted toward the carrier

Actual Cash Value, or ACV, is usually the valuation basis in a total loss claim unless the policy says otherwise. The phrase sounds neutral. The application often isn’t.

Carriers may present ACV as if it were a precise number pulled from objective software. For classics, ACV is better understood as an argument about fair market value supported by evidence. The party with better evidence usually has the stronger position.

That’s why a car appraisal for insurance claim workup has to go beyond the insurer’s printout. If the report ignores provenance, uses thin comparables, or treats your car like a commodity unit, it doesn’t deserve blind acceptance.

The real trade-off

Fast reports are cheap for insurers to generate. Accurate reports take more work.

That’s the core trade-off in these claims. Standardized systems give the carrier speed and consistency. They do not always give the owner a fair classic car worth estimate.

If the vehicle is near a total loss threshold, that valuation gap gets even more important. A low pre-loss value can affect the entire claim posture. The same is true when owners are trying to understand diminished value vs. total loss. One dispute asks what the car was worth before the event. The other asks how much value remains lost after repair. Both start with market evidence, not blind faith in software.

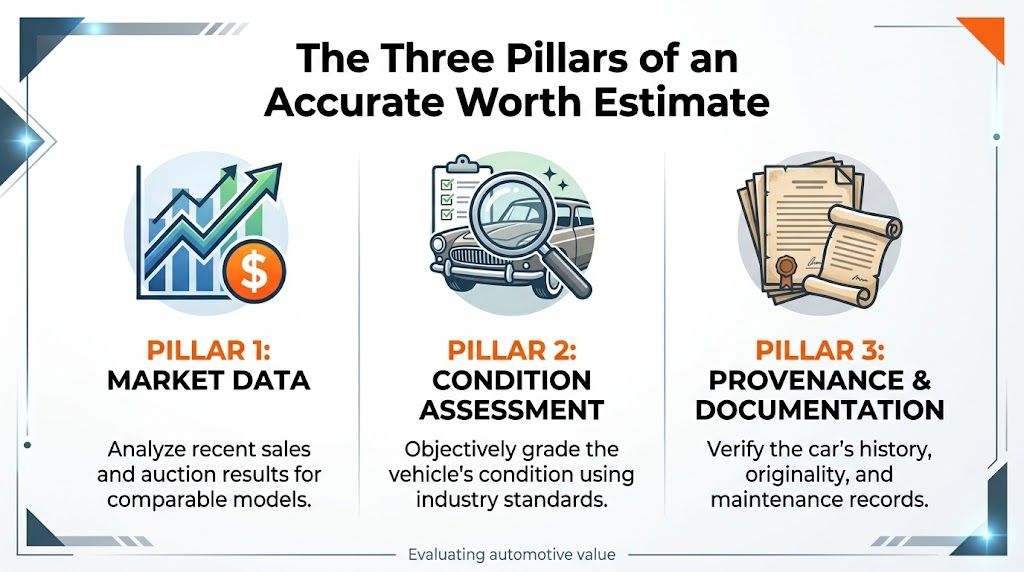

The Three Pillars of an Accurate Worth Estimate

An owner gets a total loss offer on a documented, numbers-matching car and sees it valued like a decent driver with no history. That usually means the insurer relied on a standard report built for ordinary vehicles, not a collector-market analysis.

A defensible classic car worth estimate rests on three inputs working together: market data, condition assessment, and provenance with documentation. Leave one thin, and the carrier has room to discount the file.

Market data from guides, comps, and auctions

Start with specialized collector sources, not generic insurance software. CCC ONE and similar systems can process late-model commuter cars efficiently, but they often miss the factors that separate one classic from another in the actual market.

Useful starting points include Hagerty Valuation Tools, NADA Guides, and CLASSIC.com. As noted earlier, American Collectors describes a sound process as matching the exact year, make, model, trim, engine, body style, and other specification details before weighing comparables. That is the right approach because a close spec match matters more in classics than in modern daily drivers.

Use market evidence in this order:

- Sold comparables first: Closed sales carry more weight than seller hopes.

- Recent transactions next: Older sales can help, but they need adjustment for market timing.

- Tight specification matching: Body style, drivetrain, factory equipment, and meaningful modifications all affect value.

Weak reports usually fail in familiar ways:

- They stretch the comp set: A coupe, convertible, tribute car, and original example do not belong in one pile.

- They rely on asking prices: Listings show intent, not where money changed hands.

- They depend on one database: No single guide captures private sales, dealer transactions, auction sentiment, and model-specific premiums at the same time.

SnapClaim’s fair market value guide gives a useful claims-focused explanation of how to frame market evidence so it reads like valuation support rather than a stack of screenshots.

Condition sets your position within the range

Market data gives you the range. Condition decides where the car belongs inside it.

That point gets missed constantly in insurance disputes. Two cars can share the same model year and major specs, yet one deserves the top end because it has correct finishes, sorted mechanicals, strong panel fit, and documented upkeep. The other may sit in the lower half because of paint age, corrosion, incorrect trim, or tired interior materials.

An adjuster does not need to agree with your opinion. The adjuster needs to confront your evidence. Clear photos, restoration invoices, maintenance records, and specific observations carry more weight than labels like “excellent” or “show quality.”

Sold comparables establish the bracket. Condition evidence justifies the placement.

Provenance and documentation create the premium

Classic cars break standard valuation systems. The market does not price a collector car as a generic transportation unit. Buyers pay for originality, history, documented restoration work, rare factory equipment, known ownership, and confidence that the car is what it claims to be.

That premium can be substantial in the right car. A numbers-matching drivetrain, original color combination, protect-o-plate, build sheet, ownership chain, marque expert correspondence, restoration photography, and period awards can all matter. Generic insurance tools often treat those details as invisible or irrelevant.

That is exactly why provenance belongs in the estimate, not in a side note after the insurer has already anchored the claim too low.

Here is how the three pillars function in practice:

| Pillar | Best use | Common mistake |

|---|---|---|

| Market data | Establishes the realistic value range from actual collector-market activity | Using broad or poorly matched comps |

| Condition assessment | Supports where the car falls within that range | Describing the car with vague praise instead of observable facts |

| Provenance and documentation | Supports premiums tied to originality, rarity, and known history | Assuming the insurer will identify and credit those factors without being shown |

Auction results need interpretation

Auction sales can help, especially for cars with active public trading histories. They still need context.

A headline result may reflect exceptional presentation, a well-known collection, ideal venue timing, fresh restoration work, or bidder competition that does not repeat in a private-party sale. On the other side, a rushed or poorly cataloged auction car can sell below what a patient buyer would pay in a cleaner setting.

Use auction data when the match is close and the catalog description supports the comparison. Treat it carefully when the sale is famous but the car is materially different from yours.

A strong market valuation report combines all three pillars into one argument. That is how you counter a standard insurer report that treats a documented classic like just another old car.

Grading Your Classic’s Condition Like an Appraiser

Condition drives value more than most owners want to admit. It also drives disputes, because many people describe cars generously.

Classic car valuations can involve scoring across 20 aspects to place a vehicle into one of six condition categories, according to HH Classic’s explanation of valuation methodology. That same source notes how strongly desirability and condition interact, using the example that the 1957 Chevrolet Bel Air often averages twice the worth of 1955/1956 models.

The six categories in plain English

Most owners don’t need concours judging language. They need a usable framework.

Category 1

Near-show condition. The car presents at a very high level, with excellent fit, finish, and detailing. Flaws are hard to find without close inspection.Category 2

Excellent driver or high-level restoration. It isn’t perfect, but it’s immediately impressive. Minor wear may exist, though nothing should distract from the car’s overall presentation.Category 3

Good, honest, and presentable. Many insured classics are found in this condition. The car is drivable and attractive, but closer inspection reveals age, use, or older work.Category 4

Driver-quality with visible needs. It may still be roadworthy, but cosmetic or mechanical shortcomings are obvious.Category 5

Restorable vehicle with substantial issues. It may run, or may not, but the car needs serious attention.Category 6

Parts-car territory. Value is tied more to salvageable components, identity, or restoration potential than present condition.

What separates a strong driver from an average one

A lot of disputes come down to the line between a solid Category 2 and a decent Category 3. Owners often call both “excellent.” Buyers don’t.

Look at the car the way a cautious buyer would:

- Body and paint: Check panel fit, waviness, rust evidence, bubbling, overspray, and color match.

- Chrome and trim: Pitting, dullness, missing pieces, and reproduction substitutions all matter.

- Interior: Seat wear, cracked dash pads, tired carpets, headliner condition, and switchgear authenticity tell a story quickly.

- Engine bay and undercarriage: Clean isn’t the same as correct. A fresh spray-over can hide more than it proves.

- Mechanical feel: Cold start behavior, idle quality, steering play, brake feel, and drivetrain noises affect grade.

A classic doesn’t get extra credit because it’s old. It gets the grade its current condition supports.

How to document condition so it holds up

If you’re preparing a car appraisal for insurance claim, document the car like someone else will need to defend it later.

Use a consistent photo set:

- Front, rear, both sides, and all corners

- Interior wide shots and close-ups

- Engine bay

- Trunk

- Undercarriage if available

- VIN, trim tags, odometer, and important stampings

- Every flaw you can identify

Then add written notes. Not sales language. Observations.

A useful condition note sounds like this: paint presents well from ten feet, but closer inspection shows light checking on the hood, minor chrome pitting, and age-related wear on the driver seat bolster. That’s far more credible than “beautiful classic in great shape.”

Where owners get into trouble

Some things weaken the report immediately:

| Weak approach | Better approach |

|---|---|

| “Excellent condition” | “Strong driver-grade car with older restoration and minor cosmetic aging” |

| Selective photos | Full photo set including flaws |

| Mileage as a magic value boost | Mileage considered with documentation and overall condition |

| “Garage kept” as proof | Maintenance records and objective inspection notes |

If your condition grade is inflated, every other value adjustment starts to wobble. A realistic grade may feel conservative, but it gives your classic car worth estimate credibility.

Uncovering Hidden Value in Provenance and Originality

Many classic car claims are won or lost at this stage. Two cars can look similar in photos and still trade in very different territory because one has proof behind it.

Buyers pay for confidence. Originality and provenance are how confidence gets documented.

The paperwork insurers often overlook

A standard value report rarely digs through binders, folders, and old envelopes. You should.

The most useful documents often include:

- Ownership records: Title history, prior registrations, and documented chain of custody

- Service records: Maintenance invoices, restoration receipts, and specialist shop paperwork

- Original literature: Window sticker, build sheet, manuals, warranty booklet, and dealer paperwork

- Event history: Judging sheets, awards, marque club documentation, and show records

- Restoration evidence: Before-and-after photos, parts sourcing, and notes showing what was replaced and what was preserved

Originality versus usability

Owners need to be honest about market segment. A numbers-matching, factory-correct car and a well-built restomod appeal to different buyers.

Originality usually helps when the market values factory correctness. Modifications may help drivability, but they don’t automatically help collector value. In some niches, they can narrow the buyer pool.

That doesn’t mean every non-original classic is discounted the same way. It means the report should answer a simple question: who is the likely buyer for this exact car?

A documented, largely original car tells the buyer what it is. An undocumented car asks the buyer to guess.

Rarity needs proof, not folklore

Owners often use “rare” too loosely. Low production, uncommon factory combinations, unusual body styles, and documented options can matter. Local scarcity or personal belief doesn’t prove rarity.

If rarity is part of your position, support it with factory documentation, recognized registries, marque sources, or sales history showing that comparable examples don’t appear often.

A practical file to build

If you’re preparing for a claim, sale, or market valuation report, assemble one clean package with:

- a chronology of ownership and restoration,

- scans of major invoices,

- copies of factory or period documents,

- photos of stampings, tags, and identifying details,

- and a short written summary explaining why the car is more than an average example.

That file doesn’t just help with a total loss dispute. It can also matter when establishing pre-accident value for a repaired-vehicle claim involving diminished value vs. total loss analysis.

Assembling Your Market Valuation Report for the Insurer

A classic car claim often turns on presentation as much as evidence. Owners may have strong comps, restoration invoices, and factory documents, then lose ground because the file reaches the adjuster as screenshots, loose PDFs, and angry notes. Generic systems such as CCC ONE already flatten unusual cars into average cars. A disorganized submission makes that problem worse.

The report needs to read like a valuation case file. The goal is simple. Show why this specific car sits outside the assumptions built into standard insurance tools, and support every adjustment with evidence the carrier can review line by line.

What a usable report should include

A good market valuation report usually includes these parts:

Vehicle identification

Year, make, model, series, body style, VIN, engine, transmission, factory colors, options, and any known matching-numbers details.Claim context

Date of loss, claim number, the carrier’s stated value, and whether the dispute concerns a total loss figure or pre-loss market value in another claim posture.Condition analysis

A supported condition grade with photos, inspection notes, and brief comments about paint, body, interior, chrome, glass, undercarriage, and mechanical presentation.Comparable market evidence

Recent sold examples, dealer sales when they are relevant, auction results when they are comparable, and notes explaining why each vehicle belongs in the set.Provenance and originality support

Copies of records, ownership history, restoration file excerpts, factory documentation, and photos of stampings, tags, or features that separate this car from a generic example.Reconciliation and final opinion

A short, disciplined explanation of how the evidence supports the final value range and your concluded classic car worth estimate.

Order matters. An adjuster should be able to move from identification, to condition, to comps, to conclusion without guessing how you got there.

What works in front of an adjuster

Plain language works better than outrage. The adjuster does not need a speech. The adjuster needs a reason to reject weak comps and accept better ones.

Use statements like:

- the insurer comp is not comparable because it is a different body style, engine, or series;

- the report omits documented originality, provenance, or rare factory equipment;

- the selected vehicles do not reflect equivalent condition, restoration quality, or preservation.

Avoid statements like:

- “you people are robbing me”;

- “everyone knows these cars are worth more”;

- “I saw one online for way above this.”

For owners who want a baseline on report format and valuation purpose, this overview of what a car appraisal is gives a useful starting point.

Why a structured report carries more weight

A serious report does more than attach comps. It explains why those comps fit the car and why the insurer’s examples do not. That distinction matters in the classic market, where a one-year-only configuration, documented ownership history, or high-originality car can trade in a different tier from a superficially similar driver.

Insurers often rely on systems built for ordinary late-model claims. Those systems help with volume. They do not do a good job pricing unusual collector cars with scarce production, meaningful provenance, or restoration quality that only shows up once you review the file carefully. Your report should correct that record in a form the carrier can answer, challenge, or accept.

A weak package invites a canned response. A tight package creates negotiating power.

A simple report standard

Use this check before sending the file to the carrier:

| Question | If yes | If no |

|---|---|---|

| Are the comparables true matches? | Keep them | Replace them |

| Is condition documented with photos and notes? | Use the grade confidently | Reinspect the car |

| Are originality and records attached? | Reference them in the analysis | Add an appendix |

| Does the conclusion explain the number? | Submit it | Rewrite the final section |

This kind of file helps in a total loss dispute, but it also helps when the fight is over pre-loss value on a repaired collector car. Either way, the report gives the insurer something concrete to answer instead of something easy to brush aside.

Using the Appraisal Clause and Hiring a Professional

Sometimes the insurer reviews your materials and still refuses to move enough. That’s when policy language starts to matter more than argument.

The Appraisal Clause is a policy provision that gives each side the right to appoint an appraiser to resolve a value dispute. It’s not the same as suing the carrier. It’s a contractual process for deciding value.

When the DIY route stops being efficient

A do-it-yourself valuation can work when the car is straightforward, the insurer is responsive, and the evidence gap is small.

It’s time to bring in an independent auto appraiser when:

- the insurer relies heavily on a generic software report,

- your car has meaningful provenance or originality issues the report ignores,

- the comparables are weak,

- or the valuation dispute is large enough that the quality of the evidence will decide the outcome.

A professional report can also help separate diminished value vs. total loss issues, especially when the carrier keeps shifting the discussion between them.

Why professional analysis matters more in today’s market

Static guides can lag when the market moves quickly or certain subsegments change faster than the broader hobby. The Classic Valuer’s discussion of modern valuation trends notes 20-35% value fluctuations in the last year in AI-driven data sets and reports that EV conversions can reduce values by 15-40% in purist segments. For claims work, the practical takeaway is simple. A static printout may miss what active buyers are doing.

That’s why experienced appraisers reconcile guides, sold comps, inspection findings, and segment-specific buyer behavior instead of treating one tool as gospel.

The more unusual the car, the less you should trust a one-click valuation.

Cost versus leverage

Owners sometimes hesitate to hire help because they’re already frustrated by the claim. That hesitation is understandable, but the decision should be framed like any other evidence question. Will stronger proof materially improve your negotiating position?

The author brief for this piece references that a professional appraisal often uncovers meaningful additional value. That may happen, but no ethical appraiser should promise a result. What a solid report does provide is a supported number, a credible methodology, and an advantage that vague owner opinion can’t match.

If you’re weighing whether outside help makes sense, this overview of auto appraisal cost considerations can help frame the decision. For market reference data commonly used by professionals, J.D. Power’s NADA Guides remain one of the recognized starting points.

A good appraisal is not a guarantee. It’s evidence. In claim work, evidence is what moves files.

Frequently Asked Questions About Classic Car Valuation

Can I use asking prices to support my classic car worth estimate

You can include asking prices as secondary context, but they shouldn’t carry the report. Sellers can ask whatever they want. Closed sales, especially recent and well-matched ones, are usually stronger evidence.

If you do use listings, explain why each one is relevant and note any visible differences in condition, originality, or equipment.

What if my insurer’s report uses the right model but the wrong kind of comps

Challenge the report directly and specifically. Point out body style differences, drivetrain differences, restoration level, condition grade issues, and missing documentation.

A proper market valuation report matters. The dispute is rarely won by saying the insurer is wrong in general. It’s won by showing exactly where the valuation logic breaks down.

Does mileage matter on a classic car

Yes, but not in isolation. Mileage can influence value, yet a documented, well-maintained car often presents better than a lower-mileage car with poor storage, weak records, or deterioration.

For classics, mileage is part of the condition and credibility story. It isn’t the whole story.

When should I invoke the Appraisal Clause

Usually after you’ve given the insurer a fair chance to review your evidence and it’s clear the dispute is about value, not coverage. Read your policy carefully. The clause procedures matter.

If the carrier keeps repeating a generic valuation without addressing your actual evidence, that’s often a sign the dispute has moved beyond informal negotiation. For broader consumer questions, the Auto Appraisal Expert FAQ page is a practical resource.

If your insurer is using a generic report to price a specialized collector vehicle, don’t accept that as the last word. A documented classic car worth estimate built on real comps, condition grading, and provenance can give you the evidence needed to challenge a low offer. Don’t leave money on the table. Get your free claim review or order a certified appraisal report today to take control of your insurance settlement.

About AutoAppraisalExpert

AutoAppraisalExpert is a premier provider of independent vehicle appraisal reports and insurance claim consulting. Our mission is to equip vehicle owners with the data-driven evidence required to recover the full financial value of their asset after an accident. Whether navigating a complex Diminished Value claim or disputing a low-ball Total Loss offer, we provide the certified documentation needed to negotiate with insurance companies from a position of strength.

With a national reach and deep industry expertise, we have helped thousands of policyholders identify errors in carrier valuation reports (like CCC) and invoke the Appraisal Clause to secure fair settlements. We pride ourselves on transparency, speed, and reports that stand up to the toughest insurer scrutiny.

Why Trust This Guide

This guide was written and verified by the AutoAppraisalExpert technical team. Our appraisers specialize in total loss disputes and diminished value forensics. We stay current on state insurance regulations, court-accepted valuation practices, and evolving market trends to ensure our readers, and our clients, always have the most accurate information available.

Ready to see what your car is really worth? Get your free estimate today.