You’ve just picked up your car from the shop. The repairs are done, the new paint shines, and it looks like the accident never happened. You breathe a sigh of relief, thinking the at-fault insurance company has made you whole.

But have they? There’s a hidden financial loss that adjusters almost never mention: diminished value after an accident. Put simply, your car is now worth less, not because of how it looks, but because it has an accident on its permanent record. This drop in market value is a real loss, and a standard repair check doesn’t cover it.

Why Your Car Is Worth Less After an Accident

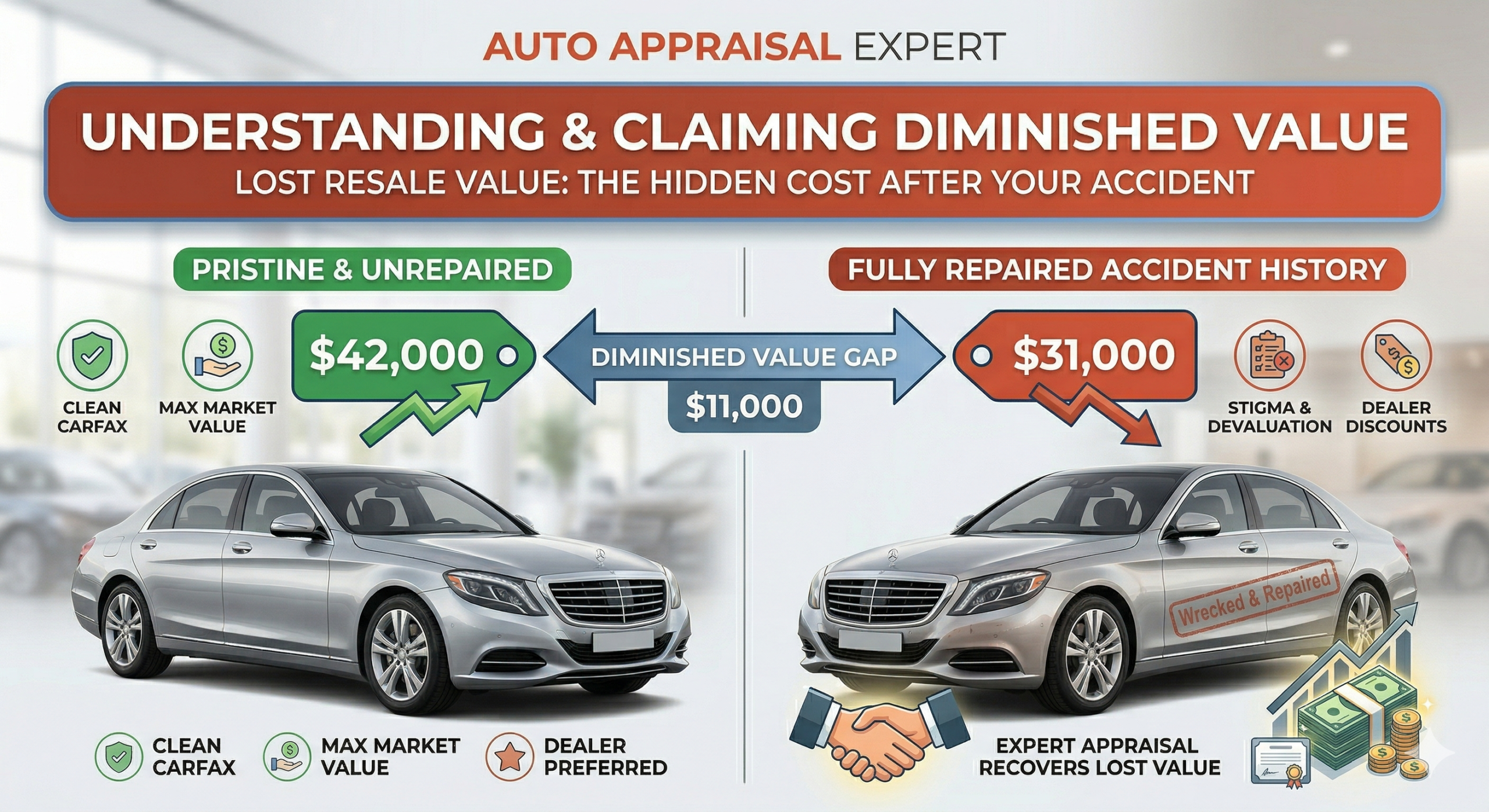

Even with flawless, high-quality repairs, a vehicle with an accident history is simply less desirable to any savvy buyer than an identical one with a clean CARFAX report. This instant loss of market appeal and resale price is what diminished value is all about. It’s a tangible financial hit you take the moment the collision is recorded, and you are entitled to be compensated for it.

Think about it from a buyer’s perspective. You’re looking at two identical used cars. Same year, same model, same mileage. One has a clean history. The other has a record of a significant collision repair. Which one are you choosing? If you even consider the repaired car, you’d demand a steep discount. That discount is its diminished value.

The Value Gap Insurers Don’t Want You to See

Most drivers believe that a check for repairs makes them financially whole again. That’s a mistake. The repair check only covers the physical damage; it does nothing to compensate for the permanent stigma now attached to your car’s vehicle history report. This creates a “value gap” that can easily cost you thousands of dollars when it’s time to sell or trade in your car.

A professional appraisal often uncovers $1,000 to $5,000+ in lost value that adjusters may overlook. It’s also vital to understand the difference between diminished value vs. total loss. A total loss means the insurer is writing your car off completely, while a diminished value claim is for a repaired vehicle that has lost market worth. You can learn more about what happens when your car is totaled here.

Your vehicle’s history is now part of its identity. A collision, even when expertly repaired, changes its story and, consequently, its market price. The at-fault driver’s insurance company is responsible for that part of the story, too.

The Three Faces of Diminished Value

To build a successful claim, it helps to understand the types of diminished value. Knowing the difference is your first step in building a rock-solid case against the insurer.

- Inherent Diminished Value: This is the most important type and the focus of most claims. It’s the automatic, unavoidable loss in value from the simple fact that the vehicle now has an accident in its history, even if repairs are perfect.

- Repair-Related Diminished Value: This loss is caused by shoddy repair work. Think mismatched paint, cheap aftermarket parts, or lingering mechanical problems. The proper remedy is to have the shop fix their work under warranty, not a DV claim.

- Immediate Diminished Value: This is the difference in value between the car’s pre-accident state and its immediate, post-accident damaged condition. This is rarely used for consumer claims.

For almost everyone pursuing a diminished value after an accident claim, inherent diminished value is the core of the fight. It’s the most predictable and provable type of loss. To see how this value is calculated using real-world market data, learn more from the experts at SnapClaim.

How Insurance Companies Undervalue Your Diminished Value After an Accident Claim

Insurance companies are masters of minimizing payouts, and they have a playbook designed to undervalue your diminished value after an accident claim. Their primary goal is to pay out as little as possible. They do this by relying on internal software and formulas that don’t reflect real-world market conditions.

One of their go-to moves is using the notorious “17c Formula,” which originated from a Georgia court case. This calculation is deliberately restrictive, built from the ground up to produce a low number. It’s an opening offer, not the final word.

The Myth of the “Algorithm”: CCC ONE and Rule 17c

Adjusters often present their valuation as an unchangeable fact generated by sophisticated software like CCC ONE. This program uses the 17c Formula, which starts by capping the maximum possible diminished value at just 10% of the vehicle’s pre-accident value. It then applies two arbitrary penalties:

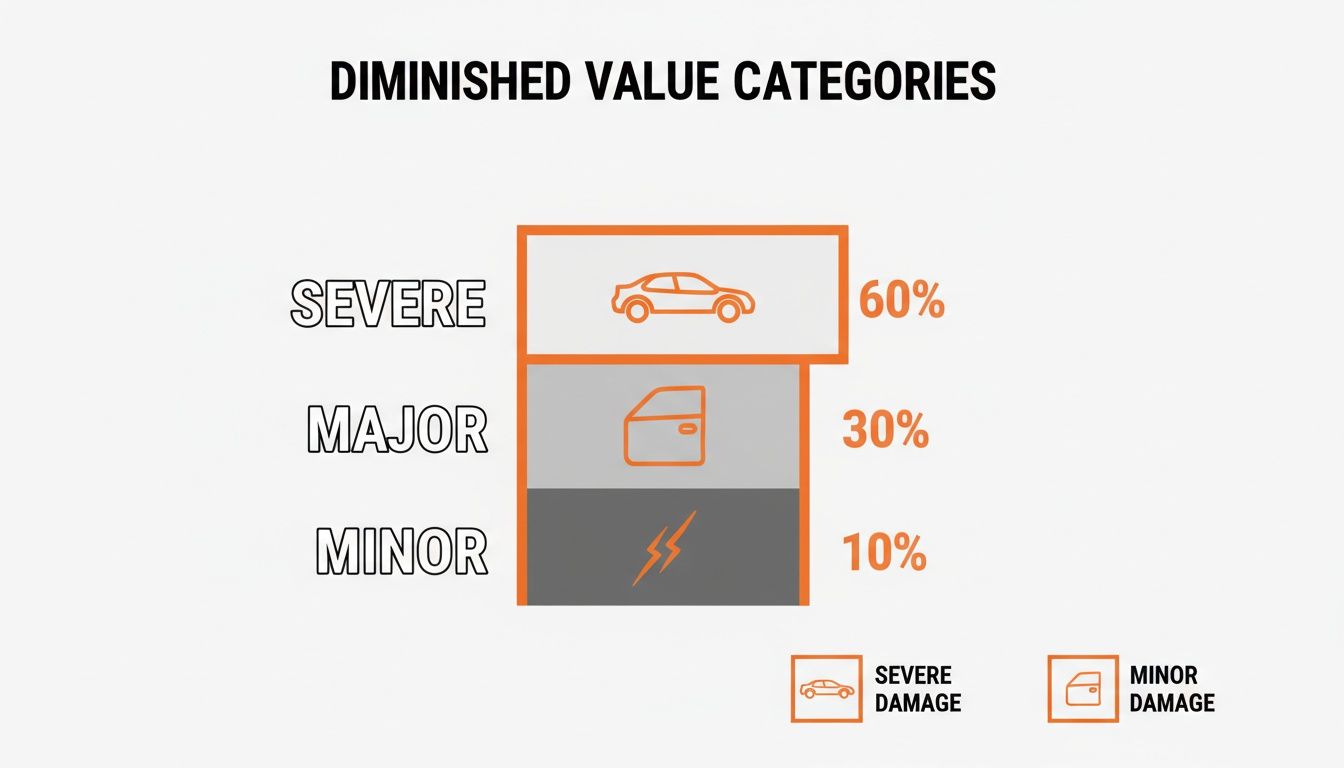

- A Damage Multiplier: This penalizes the claim based on vague categories like “minor” or “moderate.” The adjuster has total discretion, and they almost always lean toward a lower multiplier.

- A Mileage Multiplier: This reduces the value based on your car’s odometer reading, effectively punishing you for driving your car.

The result is a lowball offer presented as a final number. It’s critical to understand that this figure is just a starting point for negotiation—it is not a final authority on your car’s value.

The insurer’s calculation is an opening offer, not an objective truth. It’s based on a formula that serves their bottom line, not the reality of the automotive marketplace.

The infographic below illustrates the damage categories that directly impact these formula-based calculations, giving adjusters a way to justify their low numbers.

While this shows how adjusters classify damage, these labels are often used to justify lower payouts without considering how the market truly behaves.

Real Market Data vs. Insurer Math

The most effective way to counter these tactics is with irrefutable market evidence. A professional, independent auto appraiser provides your greatest asset. While an insurer hides behind internal formulas, a certified appraiser uses real-world data—the gold standard for proving your actual financial loss.

An appraisal report from AutoAppraisalExpert is built on evidence dealers and savvy car buyers use every day:

- Real-Time Market Data: We analyze what similar cars are actually selling for in your local area.

- Dealer-Sold Comparables: We find concrete examples of vehicles with and without accident histories to establish a clear price difference.

- Expert Analysis: Our certified appraisers provide a formal opinion of value that is USPAP-compliant. This means it follows the Uniform Standards of Professional Appraisal Practice, ensuring it stands up under insurer scrutiny.

This data proves a generic formula doesn’t cut it. A certified appraisal from a trusted resource like SnapClaim delivers the evidence you need to dismantle the insurer’s lowball offer. For a deeper look at how experts determine this, check out this guide to establishing fair market value after an accident.

Your Step-by-Step Guide to a Successful Claim

Filing for diminished value after an accident can feel daunting, but a clear strategy empowers you to take control. You are building a data-driven case so undeniable the insurance company can’t simply dismiss it.

With the right approach, you can shut down their lowball tactics and negotiate from a position of strength.

Step 1: Confirm Eligibility and Gather Evidence

First, ensure you have a valid claim. In most states, you can only file for diminished value against the at-fault driver’s insurance company (a third-party claim). If you were at fault, your own policy likely won’t cover this loss.

Once you’ve confirmed liability, gather this essential paperwork:

- The Police Report: Official proof of who was at fault.

- Repair Invoices: The final, itemized bill from the body shop.

- Photos and Videos: Collect all images of the damage and completed repairs.

Step 2: Get a Certified, USPAP-Compliant Appraisal

This is the most critical step. An online calculator or a dealer’s guess won’t survive an adjuster’s scrutiny. You need a USPAP-compliant diminished value appraisal from a certified professional.

A USPAP-compliant report is authoritative and extremely difficult for an insurer to discredit. This professional analysis frequently uncovers $1,000 to $5,000+ in lost value that the insurance company’s formulas ignore, showing a clear return on your investment.

An appraisal report is your proof. Without it, you are just asking for money. With it, you are proving a specific, quantifiable financial loss.

Step 3: Send a Formal Demand Letter

With your certified appraisal in hand, draft a formal demand letter to the at-fault party’s insurance adjuster. Keep it professional and firm.

Your demand letter must include:

- Your name, contact information, and claim number.

- A clear statement that you are making a claim for inherent diminished value.

- The exact dollar amount you are demanding, as determined by your appraisal.

- A full copy of your certified appraisal report and supporting documents.

This letter officially puts the insurer on notice and forces them to address your evidence-based claim. For more detailed guidance, see our article on how to calculate diminished value.

Step 4: Negotiate and Invoke the Appraisal Clause

The adjuster will likely respond with a low counteroffer. Stay firm. Point them back to the real market data and dealer-sold comparables cited in your report. This is a negotiation, and you now have the evidence to back up your position.

If they refuse to negotiate in good faith, it’s time to play your trump card: the Appraisal Clause. This is a provision in most auto insurance policies that gives you the right to an independent appraisal to settle a dispute. Invoking this clause can force a binding resolution. For a quick, free claim review, visit SnapClaim.

Why an Independent Appraisal Is Your Strongest Weapon

When you’re fighting for diminished value after an accident, you can’t just tell the adjuster their offer is “too low.” The single most powerful tool you have is a professional, independent appraisal report.

To win a negotiation against a trained adjuster, you must show up with the same level of authority and evidence they use themselves. A certified appraisal from an independent auto appraiser levels the playing field.

A USPAP-compliant report isn’t just an opinion; it’s a courtroom-ready document. It contains a meticulous vehicle inspection, pre- and post-accident market valuations, and a deep dive into comparable vehicles sold in your local area. This professional documentation forces the insurer to negotiate from a position of weakness.

The ROI Factor of a Certified Report

Some car owners hesitate to pay for an appraisal, but this is a mistake. View it as an investment. The small cost of a report has the potential to unlock a payout many times larger, often uncovering $1,000 to $5,000 or more in value that the insurer’s initial offer ignored. Our reports provide the evidence needed to negotiate for the full, fair amount you are rightfully owed.

What Makes an Appraisal Report So Powerful

A top-tier car appraisal for an insurance claim systematically dismantles the insurance company’s lowball arguments. It replaces their self-serving software with transparent, verifiable market reality.

A proper, USPAP-compliant report will always include:

- Detailed Vehicle Analysis: A thorough review of your vehicle’s specifics, including condition.

- Real-World Comparables: We pinpoint recently sold vehicles identical to yours, comparing examples with and without accident histories to establish a clear value gap.

- Expert Valuation Methodology: Our certified appraisers use industry-accepted techniques to determine the precise Actual Cash Value (ACV). ACV is the pre-accident market value of your vehicle.

- Local Market Focus: Valuations are tailored to your specific geographic area.

This comprehensive approach gives you the ammunition to force the adjuster off their lowball number. To learn more about proper valuation, check out the resources on the SnapClaim Fair Market Value page.

Your appraisal report is your evidence. Without it, you are simply asking for more money. With it, you are proving a specific, documented financial loss.

The insurance industry’s claims process can systematically underpay consumers. A vehicle with a $20,000 repair bill can easily have an additional $2,000 to $4,000 in unrecovered diminished value. This is why an independent valuation is essential protection. You can see the full scope of accident costs in this official NHTSA report.

Frequently Asked Questions About Diminished Value Claims

Here are answers to common questions about claiming your diminished value after an accident.

How long do I have to file a diminished value claim?

Every state has a deadline, known as the statute of limitations, for filing property damage claims, usually between two and five years from the accident date. However, you should file your claim as soon as repairs are finished to prevent the insurer from arguing that other factors caused the value loss. You can see specific rules for different areas, like these guidelines for diminished value claims in Colorado.

Can I claim diminished value if I was at fault?

In almost all cases, no. A diminished value claim is a third-party claim, meaning you file it against the at-fault driver’s insurance. Your own policy (a first-party claim) typically does not cover this loss. The primary exception is the state of Georgia, which you can read more about on the Progressive website.

Is diminished value different from a total loss?

Yes, they are completely separate. Diminished value is for cars that are repaired and pays for the drop in resale value. A total loss is for cars that are not repaired because the repair cost exceeds the total loss threshold. The insurer pays you the car’s pre-accident value and takes ownership of the vehicle. You can have one or the other, but not both.

Don’t leave money on the table. Get your free claim review or order a certified appraisal report today to take control of your insurance settlement.

About AutoAppraisalExpert

AutoAppraisalExpert is a premier provider of independent vehicle appraisal reports and insurance claim consulting. Our mission is to equip vehicle owners with the data-driven evidence required to recover the full financial value of their asset after an accident. Whether navigating a complex Diminished Value claim or disputing a low-ball Total Loss offer, we provide the certified documentation needed to negotiate with insurance companies from a position of strength.

With a national reach and deep industry expertise, we have helped thousands of policyholders identify errors in carrier valuation reports (like CCC) and invoke the Appraisal Clause to secure fair settlements. We pride ourselves on transparency, speed, and reports that stand up to the toughest insurer scrutiny.

Why Trust This Guide

This guide was written and verified by the AutoAppraisalExpert technical team. Our appraisers specialize in total loss disputes and diminished value forensics. We stay current on state insurance regulations, court-accepted valuation practices, and evolving market trends to ensure our readers—and our clients—always have the most accurate information available.

Ready to see what your car is really worth? Get your free estimate today.