So, you’ve been in a car accident. After weeks at the body shop, your car finally looks brand new, but you have a sinking feeling you're not whole. You're right. The insurance company paid for repairs, but they haven't compensated you for the permanent hit to your car's resale value.

This drop in market price is called diminished value, and knowing how to calculate diminished value is your first step in recovering the money you're rightfully owed. The moment an accident shows up on a vehicle history report, your car is branded, and that stigma costs you real money. We're here to help you level the playing field.

What Is Diminished Value and Why It Matters

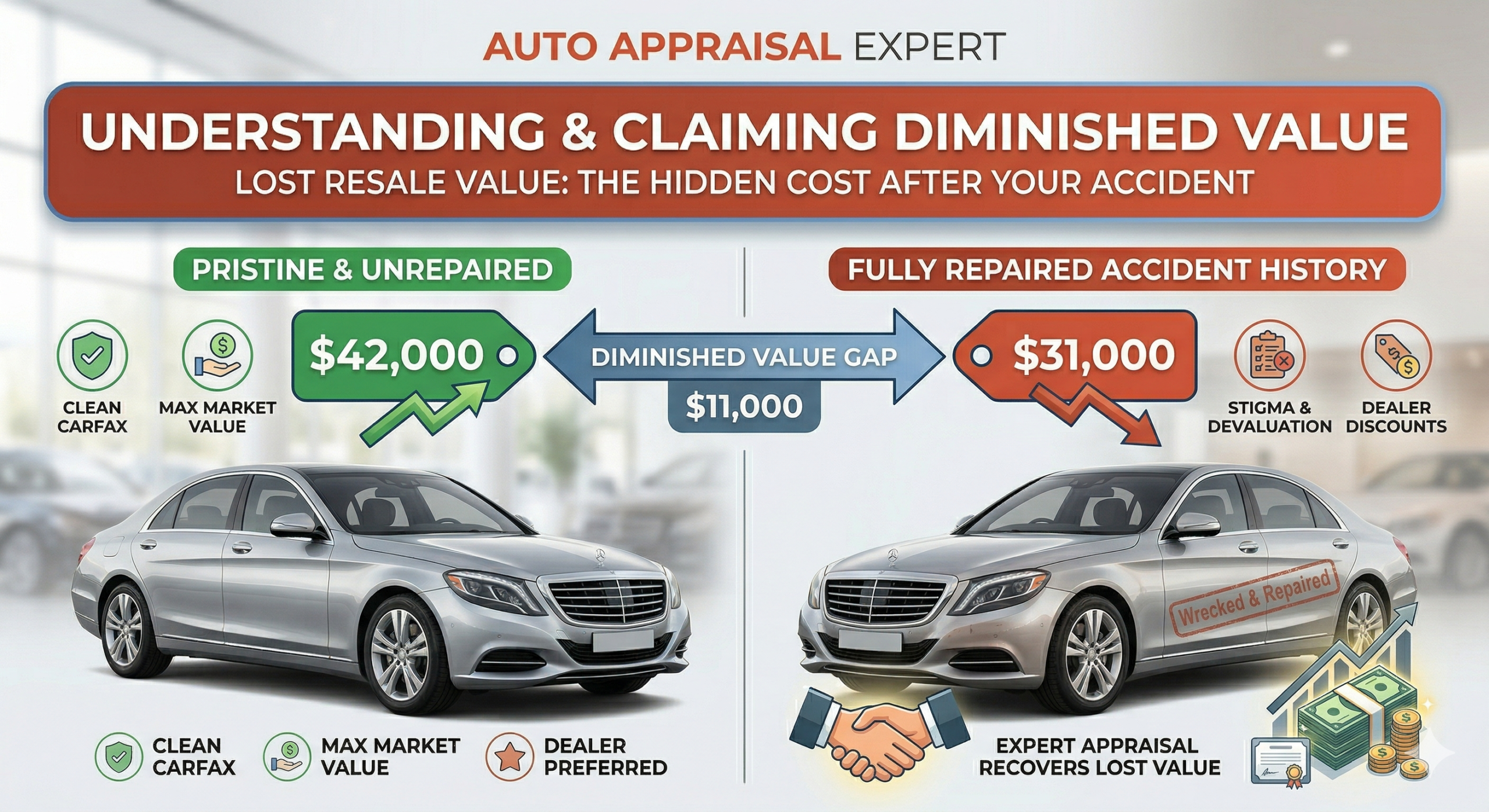

Put yourself in a buyer’s shoes. If you were looking at two identical cars, but one had a history of significant collision repair, you wouldn’t pay the same price. You'd demand a serious discount for the wrecked-and-repaired one. That discount is the diminished value.

Unfortunately, insurance adjusters are trained to minimize this loss. They often use internal, one-size-fits-all formulas and valuation software (like CCC ONE) designed to produce the lowest possible number. They're betting you don't know the rules of the game.

You don't have to play their game or accept a low-ball offer. Arming yourself with knowledge is the most powerful move you can make.

The Three Types of Diminished Value

"Diminished value" isn't a single vague concept. It breaks down into three distinct categories. Understanding which type applies to your car is key to building a solid claim with the insurance company.

Here's a quick rundown of the three main types:

| Type of Diminished Value | What It Means for You |

|---|---|

| Inherent Diminished Value | This is the most common type. It’s the automatic loss of value from having an accident history, even if the repairs are flawless. |

| Repair-Related Diminished Value | This is additional value loss from shoddy workmanship, like mismatched paint, poor panel gaps, or cheap aftermarket parts. |

| Immediate Diminished Value | This is the value difference right after the crash but before repairs. It’s rarely used in claims but is a valid legal concept. |

For most people filing a claim against the at-fault driver’s insurance, inherent diminished value is the core of the argument. It’s the undeniable stigma that has devalued your asset. This is often a battle between diminished value vs. total loss; if the repair costs approach the total loss threshold, the insurer may declare it a total loss instead.

Challenging the Insurer’s Math

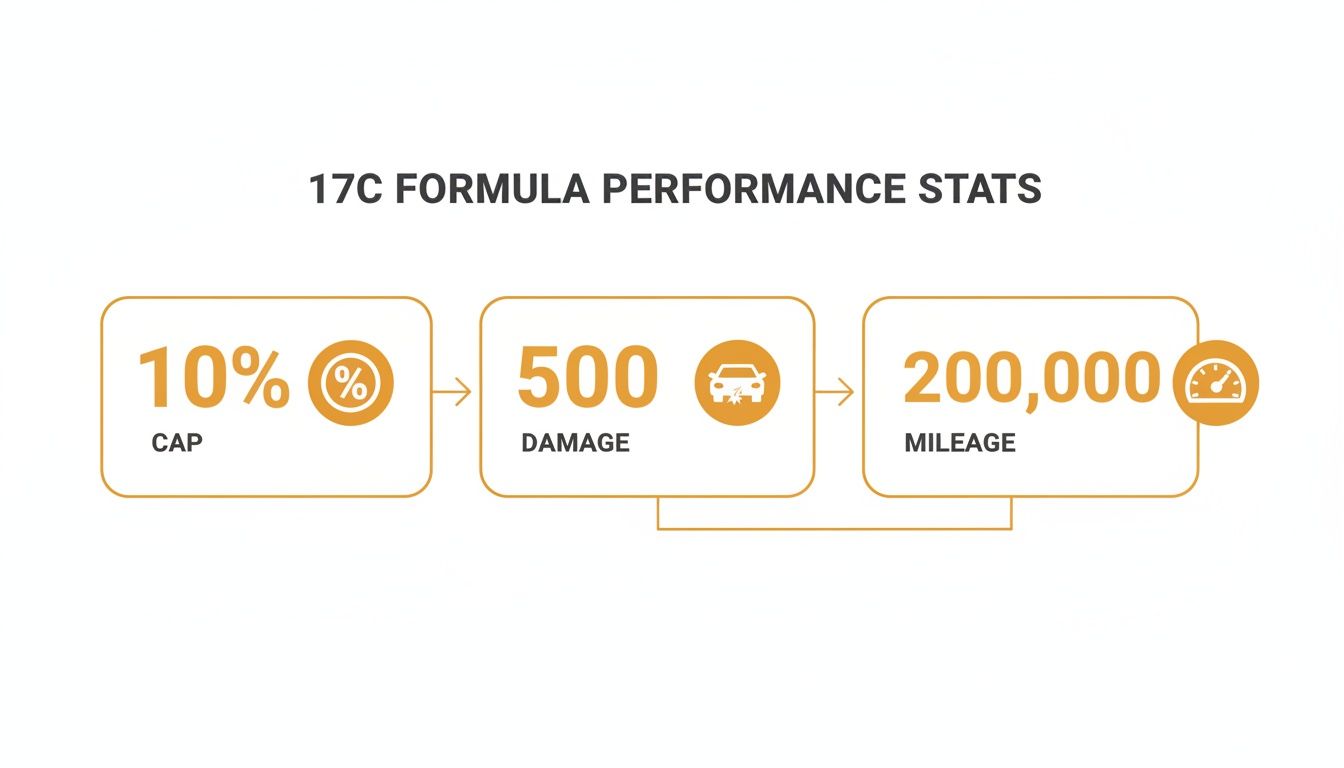

The insurance industry’s favorite trick for calculating diminished value is a formula known as 17c. It’s important to know that this is an internal tool, born from a single Georgia court case—it is not a law.

The 17c formula starts by capping the potential loss at just 10% of your car’s pre-accident value. Then, it applies arbitrary deductions for damage severity and mileage, whittling the final number down even further.

The 17c formula is a starting point for the insurance company, not the final word for you. It completely ignores real-world market factors like your vehicle’s desirability, regional demand, and the actual quality of the repairs performed.

The truly accurate way to determine the loss is through a market valuation report. A professional independent auto appraiser doesn’t use a magic formula; we compare your repaired vehicle to actual sales prices of identical cars on the open market—some with clean histories and some with accident records.

This evidence-based approach reveals the true financial impact of the accident stigma, with the potential to uncover anywhere from $1,000 to $5,000+ more than an insurer’s initial formula-based offer. To see how we build these USPAP-compliant reports, explore our comprehensive Diminished Value Service Page.

The Insurer’s Secret Weapon: How to Calculate Diminished Value Using the 17c Formula

When you ask an insurance company how to calculate diminished value, they’ll often pull out their favorite tool: the “17c Formula.” Understand this right away: this is the insurer’s internal shortcut, not an appraisal law or a reflection of the real world. It was designed for one purpose—to process claims quickly and cheaply.

This formula isn’t some ancient appraisal secret; it’s the direct result of a legal battle. The 17c Formula was born from the landmark 2001 Georgia Supreme Court case, Mabry v. State Farm. In that case, the court ruled that State Farm failed to properly pay policyholders for the loss in value after repairs. The settlement that followed outlined this specific calculation in paragraph 17, section C of the court documents—hence the name “17c.” You can find detailed breakdowns of this pivotal case.

Breaking Down the 17c Calculation

The 17c formula is a three-step process designed to systematically slash your claim’s value. Let’s walk through it with a vehicle that has a pre-accident Actual Cash Value (ACV) of $30,000. ACV is a simple term for what your car was worth on the open market the moment before the crash.

-

The 10% Cap: First, the insurer assumes the maximum loss is 10% of the vehicle’s pre-accident worth. For our $30,000 car, this immediately limits the potential claim to $3,000, no matter how bad the accident was.

-

The Damage Multiplier: Next, they apply a “damage multiplier” based on a subjective scale from 0.00 to 1.00. Severe structural damage might get a 1.00, while moderate panel damage could be 0.50. If our example car had moderate damage, the claim is instantly cut in half: $3,000 x 0.50 = $1,500.

-

The Mileage Penalty: Finally, the insurer applies a mileage deduction. If our car has 45,000 miles, the insurer might use a 0.60 multiplier, shrinking the claim again: $1,500 x 0.60 = $900.

And just like that, a significant accident on a $30,000 vehicle results in a meager $900 offer. This rigid, insurer-friendly math is exactly why you have to know how to fight it.

The Fundamental Flaw of the 17c Method

The biggest problem with the 17c formula is what it ignores: reality. It’s a sterile calculation that has zero connection to the real world where actual human beings buy and sell cars.

The 17c formula is a mathematical abstraction. It completely disregards market demand, vehicle desirability, brand stigma, and the quality of the repairs—all the factors a real buyer considers before making an offer.

A certified market valuation report from an independent auto appraiser is the definitive counterpunch to this flawed formula. Instead of using arbitrary multipliers, a professional appraisal uses real-world data from dealer-sold comparables and auction results to prove your vehicle’s true loss in value. This is the evidence you need to push the negotiation past their bogus formula.

Beyond 17c: A Real-World Guide to How to Calculate Diminished Value

If the 17c formula is the insurer’s shortcut, a proper market analysis is the professional’s roadmap to the truth. This is the gold-standard method certified appraisers use, and it’s designed to pinpoint your vehicle’s actual loss in market value.

Forget arbitrary caps and subjective multipliers. This approach is grounded in real-world data, not a flawed algorithm. It directly answers the question of how to calculate diminished value by looking at what real buyers are willing to pay for a car just like yours, but with an accident history.

Moving Beyond Formulas to Real-World Data

A true market analysis is elegantly simple. It works by comparing your repaired car to two specific groups of vehicles currently for sale:

- “Clean” Comparables: Identical models—same year, make, trim, and similar mileage—with no accident history. Their average selling price establishes your car’s true pre-accident value.

- “Branded” Comparables: Identical models that have a similar accident history reported. Their average selling price reveals the market penalty—the real-world diminished value.

The gap between what the “clean” cars sell for and what the “branded” ones sell for is your actual, quantifiable loss. It’s not a guess; it’s a direct reflection of consumer behavior.

The graphic below highlights the flawed inputs that the 17c formula uses, which a proper market analysis is specifically designed to overcome.

Unlike this formulaic approach, a real market valuation report accounts for the specific nuances that these simple, one-size-fits-all modifiers completely ignore.

A Tale of Two Valuations: A Ford F-150 in Texas

Let’s walk through a real-world scenario. Imagine you own a 2024 Ford F-150 in Texas that was worth $45,000 before being in a moderate collision. The at-fault driver’s insurer, armed with the 17c formula, offers you a check for $2,500.

Now, let’s see what a market analysis reveals:

- Pre-Accident Value: We find multiple clean-title 2024 F-150s with similar mileage selling for an average of $45,000 on Texas dealer lots. This confirms the baseline value.

- Post-Accident Value: Next, we identify similar F-150s with reported accident damage. They’re selling for an average of only $34,500.

- The True Loss: The difference is a staggering $10,500 ($45,000 – $34,500).

In this real-world example, the market analysis has the potential to uncover an additional $8,000 in diminished value that the insurer’s formula completely missed. This is the power of using real data.

This approach is powerful because it can be tailored to specific vehicle types and regions. Truck demand in Texas is sky-high, which influences pricing. Likewise, the stigma against a repaired luxury sedan is often far greater than 10%—a critical fact the 17c formula won’t account for. You can learn more about how accident history impacts resale value on KBB.com.

When an insurance company hands you a low offer based on their internal formula, they’re betting you won’t challenge it with superior evidence. A professional market valuation report, built on certified appraisal methodologies, is precisely the evidence you need to call their bluff and negotiate from a position of strength.

How Repair Quality Impacts Your Final Payout

When calculating diminished value, most people focus only on the accident itself. But there’s another layer of value loss that insurers conveniently ignore: repair-related diminished value. This is the extra drop in your car’s worth caused directly by shoddy, incomplete, or subpar repairs.

Even without an accident on the vehicle history report, a savvy buyer or a trade-in manager can spot poor workmanship from a mile away. These flaws amplify the market stigma, compounding your financial loss.

It’s one thing to have a car with a documented accident history; it’s another to have one that still wears the visible scars of a bad repair job.

Becoming Your Own First-Line Inspector

You don’t need to be a certified appraiser to spot the most common repair-related red flags. Before you accept your vehicle back from the body shop, become your own inspector. A careful walk-around can reveal major issues that an insurer’s simple formula would never account for.

Here’s what to look for:

- Mismatched Paint: Look at the repaired panels from different angles and in different lighting. Does the new paint perfectly match the factory finish in both color and texture?

- Uneven Panel Gaps: Crouch down and check the spaces between the doors, the hood, and the trunk. Are the gaps uniform, or are they wider in some places and narrower in others?

- Non-OEM Parts: Did the shop use Original Equipment Manufacturer (OEM) parts or cheaper aftermarket alternatives? The final repair order should specify this, but aftermarket parts can often be identified by a flimsy feel or poor fitment.

These flaws are more than cosmetic. They are glaring signals to any future buyer that the car was not properly restored, which is crucial when you need to calculate diminished value accurately.

How Subpar Repairs Compound Your Loss

Imagine a 2023 Honda Civic with a pre-accident value of $22,000. After a moderate collision, the at-fault driver’s insurer uses the 17c formula and offers you $880. You get the car back, but you notice the new bumper color is slightly off and a headlight doesn’t sit right.

Now, you try to sell it. Clean, comparable Civics are selling for $20,000, but because of the accident history and the visible repair flaws, the best offer you can get is $16,500.

Your true loss isn’t the $880 the insurer offered. It’s the $5,500 difference between its pre-accident value and what the market is now actually willing to pay for it—a loss caused by both the accident and the poor-quality repair.

This is repair-related diminished value in action. It’s a separate and additional loss that basic formulas completely fail to capture. Documenting this poor workmanship is critical evidence. You can read more about these findings on TheZebra.com.

A professional car appraisal for insurance claim purposes will meticulously document every one of these defects. An independent auto appraiser uses high-resolution photos, a detailed analysis of the repair order, and paint meter readings to build an undeniable case that the insurer’s initial offer was inadequate.

How to Build and Present Your Diminished Value Claim

Knowing what your car is worth after an accident is only half the battle. The real fight is getting the insurance company to actually pay it.

This is where you shift from calculating a number to building a case. A compelling claim isn’t about simply asking for more money; it’s about presenting a mountain of evidence that proves your financial loss, leaving the adjuster with no room to argue.

Think of yourself as the lawyer for your own car. You need to collect the right paperwork, write a powerful opening statement, and know which rules to play by.

Your Essential Documentation Checklist

Before you ever pick up the phone, the first step is always organization. An adjuster can easily brush off a verbal complaint, but they can’t ignore a folder packed with official documents.

Create a dedicated folder and start gathering these key items:

- The Police Report: This officially establishes fault, which is the foundation for any third-party claim.

- The Final Repair Invoice: This document is your proof of the accident’s severity, listing every part replaced and every hour of labor.

- Pre-Accident Maintenance Records: Showcasing that your vehicle was well-maintained proves it was in excellent condition before the crash, strengthening its pre-accident value.

- Photos and Videos: Get pictures of the initial damage before repairs and clear shots of any lingering flaws after the work is done.

The Cornerstone of Your Claim: The Professional Appraisal

Once your documents are organized, it’s time to get your most powerful weapon: a professional, USPAP-compliant appraisal report.

USPAP stands for the Uniform Standards of Professional Appraisal Practice. It’s the set of ethical and performance rules for the appraisal profession. Handing the insurer a USPAP-compliant report shows them you aren’t just guessing—you have a certified valuation from an expert.

This report is the definitive answer to how to calculate diminished value. It moves your claim from the realm of opinion into the world of hard facts. A certified market valuation report from an independent auto appraiser is the single most important investment you can make, with the potential to uncover $1,000 to $5,000+ in value that adjusters miss. If you’re wondering how to challenge the insurer’s lowball valuation, you might be interested in our guide on auditing your total loss report from CCC.

Drafting a Compelling Demand Letter

Your demand letter is your formal opening argument. It needs to be professional, concise, and completely backed by the evidence you’ve gathered.

Your letter should clearly and calmly state:

- Your identity and the associated claim number.

- The basic facts of the accident, confirming the other party’s fault.

- The specific amount of diminished value you are claiming, explicitly citing your appraisal report.

- A list of all enclosed documents (police report, repair bill, appraisal, etc.).

- A reasonable deadline for their response, like 15 business days.

Expert Tip: Use precise language. Don’t say, “My car is worth less now.” Instead, write, “As documented in the attached certified appraisal report, my vehicle has suffered an inherent diminished value of $X,XXX as a direct result of the collision.”

Invoking Your Secret Weapon: The Appraisal Clause

So, what happens if the insurance company ignores your demand or replies with another insulting lowball offer? This is when you deploy the most powerful tool hidden in your policy: the Appraisal Clause.

The Appraisal Clause is a provision that gives you the right to an independent resolution process when you disagree on your vehicle’s value. It forces the insurer to engage with your evidence on a level playing field. Learn more about how to leverage the Appraisal Clause on our Total Loss & Appraisal Clause Page.

Invoking this clause transforms you from a passive victim into an active participant. Subrogation, the process where your insurer goes after the at-fault party’s insurer, doesn’t always include diminished value, so taking direct action is often necessary.

FAQ: Answering Your Top Diminished Value Questions

Can I claim diminished value if the accident was my fault?

In almost all states, the answer is no. A diminished value claim is a third-party claim against the at-fault driver’s insurance company. Your own policy’s collision coverage is designed to cover repairs but typically excludes diminished value. The only major exception is Georgia, where insurers must cover it even on first-party claims.

How long do I have to file a diminished value claim?

Every state has a statute of limitations for property damage, which is a hard deadline for filing. These time limits can be as short as two years or as long as six from the date of the accident. The best time to file is right after repairs are done to prevent the insurer from blaming subsequent wear and tear for the value loss.

Is paying for an independent auto appraiser really worth it?

Absolutely. A professional appraisal isn’t a cost—it’s an investment that delivers a powerful return. Without a certified report, your claim is just your word against theirs. A USPAP-compliant market valuation report provides the hard evidence needed to negotiate, and it often uncovers $1,000 to $5,000+ in lost value that an insurer’s formula misses.

What if the insurance company just ignores my demand?

This is a classic tactic designed to wear you down. Your strongest response is to formally invoke the Appraisal Clause in your policy. This forces them into a binding dispute resolution process with independent appraisers. If they still act in bad faith, contact an attorney. For personalized help, you can always reach out to us for a free consultation.

Don’t leave money on the table. Get your free claim review or order a certified appraisal report today to take control of your insurance settlement.

About AutoAppraisalExpert

AutoAppraisalExpert is a premier provider of independent vehicle appraisal reports and insurance claim consulting. Our mission is to equip vehicle owners with the data-driven evidence required to recover the full financial value of their asset after an accident. Whether navigating a complex Diminished Value claim or disputing a low-ball Total Loss offer, we provide the certified documentation needed to negotiate with insurance companies from a position of strength.

With a national reach and deep industry expertise, we have helped thousands of policyholders identify errors in carrier valuation reports (like CCC) and invoke the Appraisal Clause to secure fair settlements. We pride ourselves on transparency, speed, and reports that stand up to the toughest insurer scrutiny.

Why Trust This Guide

This guide was written and verified by the AutoAppraisalExpert technical team. Our appraisers specialize in total loss disputes and diminished value forensics. We stay current on state insurance regulations, court-accepted valuation practices, and evolving market trends to ensure our readers—and our clients—always have the most accurate information available.

Ready to see what your car is really worth? Get your free estimate today.

Related Posts