Getting the call from an insurance adjuster stating your vehicle is a total loss is often the start of a second accident—a financial one. While you are still dealing with the physical and emotional aftermath of a collision, you are suddenly forced to negotiate with a multi-billion dollar corporation over the value of your property.

At Auto Appraisal Expert, we specialize in helping vehicle owners navigate this complex process. The reality is that insurance companies use standardized software designed to minimize payouts. If you don’t know how to read their reports or how to invoke your rights, you could be leaving thousands of dollars on the table.

In this exhaustive guide, we will cover everything from the legal definition of a “totaled” car to the precise steps required to dispute a low settlement offer and win.

1. Understanding the “Total Loss” Definition

What exactly does it mean when a car is “totaled”? It isn’t always about the car being a mangled heap of metal. In fact, many vehicles that look perfectly driveable are declared total losses for economic reasons.

The Math Behind the Decision

Insurance companies typically use one of two methods to determine if a car is a total loss:

- The Total Loss Threshold: Many states (such as Florida or Texas) have statutory limits. If the cost of repairs plus the salvage value exceeds a certain percentage of the Actual Cash Value (ACV)—usually 70% to 80%—the car must be totaled by law.

- The Total Loss Formula (TLF): Some states use a formula:

Cost of Repair + Salvage Value > Actual Cash Value. If the math checks out, the car is deemed a loss.

Actual Cash Value (ACV) vs. Replacement Cost

This is the most common point of confusion. Unless you have a specific “New Car Replacement” rider, your insurance policy only covers the Actual Cash Value.

- ACV is defined as the fair market value of the vehicle immediately before the loss occurred.

- It accounts for depreciation, mileage, and pre-existing wear and tear.

- It is not what you owe on your loan (which is why Gap Insurance is important).

2. How the Insurance Company Calculates Your Offer

Insurers rarely use Kelley Blue Book (KBB) or Edmunds to value your car. Instead, they rely on specialized database software like CCC Intelligent Solutions, Mitchell, or Audatex.

The Problem with Valuation Software

These programs generate a Market Valuation Report. While they claim to be objective, they often “cherry-pick” data to lower the average. Common tactics include:

- Selecting “Low-Ball” Comparables: Using vehicles sold at auctions or through private sales that don’t reflect retail dealership prices.

- Geographic Skewing: Pulling “comparable” vehicles from 200 miles away where prices are lower than in your local market.

- Condition Adjustments: Deducting value for “average” wear and tear, claiming your car wasn’t in “dealer-ready” condition.

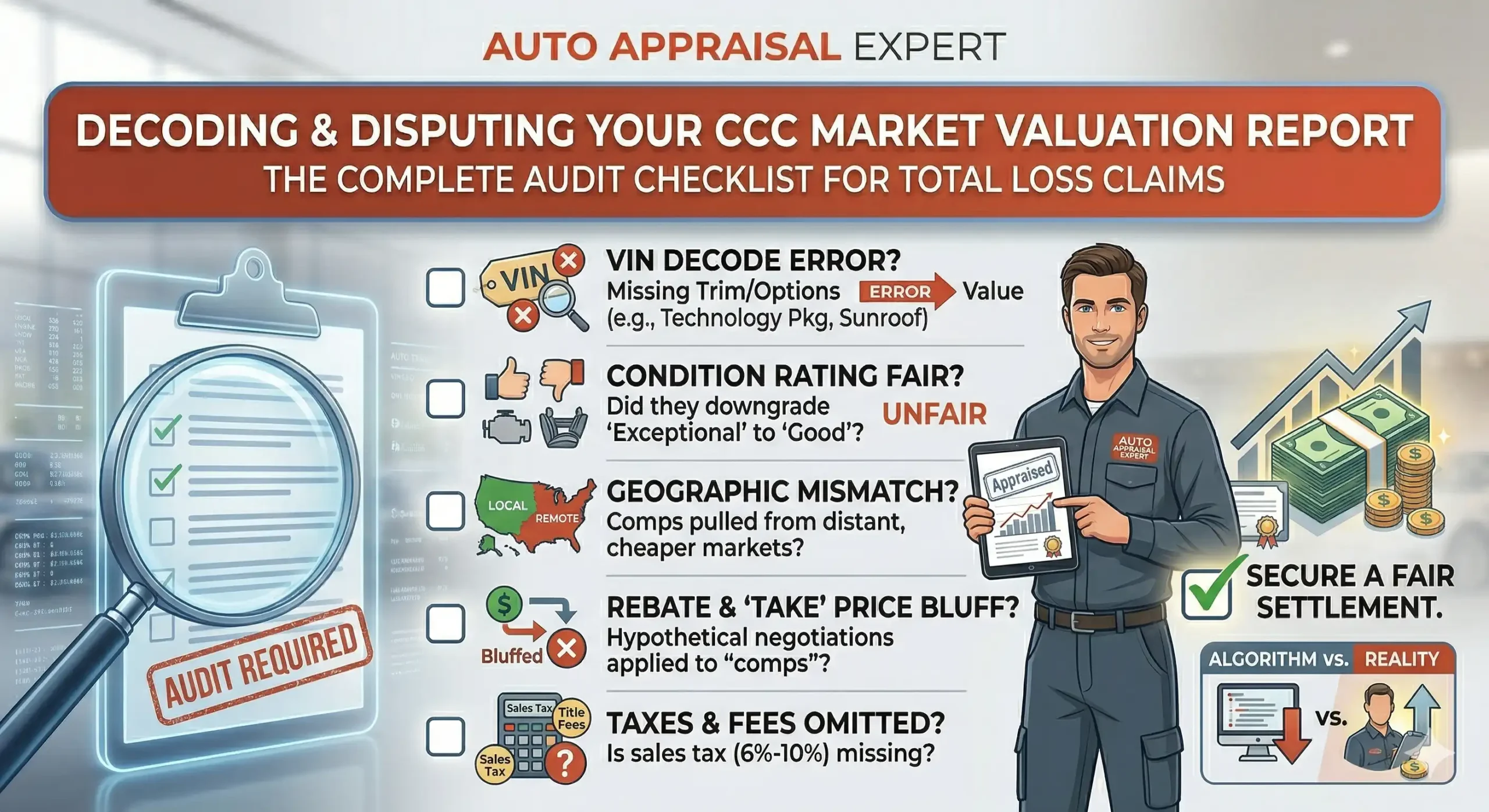

3. How to Review Your Total Loss Valuation Report

When the adjuster sends you a settlement offer, they will provide a PDF report (often 10–20 pages long). Do not just look at the final number. You must audit the report line-by-line.

Step A: Verify the “Decode”

The software “decodes” your VIN to determine your car’s features. Check for:

- Trim Level: Did they list your “Touring” edition as a base model?

- Packages: Are the sunroof, premium leather, and upgraded tech package listed?

- Mileage: Is the mileage accurate to the day of the crash? Even a few thousand miles can swing a value by $500–$1,000.

Step B: Audit the “Comparable Vehicles”

The report will list 3–5 vehicles “similar” to yours. Investigate them:

- Are they the same year? (A 2021 model is worth significantly more than a 2020).

- Do they have similar mileage?

- Are they currently for sale? Call the dealerships listed. Often, those cars were sold months ago or had “branded titles” (previous accidents) that the report failed to mention.

Step C: Analyze Condition Ratings

The adjuster rates various components (Paint, Interior, Tires, Engine) as “Fair,” “Good,” “Very Good,” or “Exceptional.” Adjusters almost always default to “Good” or “Private Party” condition. If you meticulously maintained your car, you should argue for “Exceptional” ratings.

4. Evidence You Need to Increase Your Settlement

If you believe the offer is too low, you cannot simply say, “I feel my car is worth more.” You need documented evidence.

1. Maintenance Receipts

Recent major maintenance adds value. If you put on new tires, replaced the timing belt, or installed a new transmission within the last 6–12 months, provide those receipts. While you won’t get a dollar-for-dollar return, it proves the vehicle was in superior mechanical condition.

2. Independent Market Research

Conduct your own search on Autotrader and Cars.com. Find at least three vehicles for sale within a 50-mile radius that match yours. If the average price of these cars is $25,000 and the insurance offered you $21,000, you have a clear case for a discrepancy.

3. Proof of Upgrades

Did you add a lift kit, a high-end audio system, or custom wheels? Standard valuations often ignore these. While some policies limit coverage for “aftermarket parts” to $500 or $1,000, you are still entitled to that value.

5. The “Appraisal Clause”: Your Legal Right to Dispute

If negotiations stall, most people think their only option is to hire a lawyer. This is a mistake. Most auto policies contain a specific provision called the Appraisal Clause.

How the Appraisal Clause Works

The Appraisal Clause is essentially a form of binding arbitration specifically for the value of the vehicle. Here is the process:

- Demand Appraisal: You formally notify the insurer in writing that you are invoking the Appraisal Clause.

- Hire Your Appraiser: You hire an independent expert, like Auto Appraisal Expert.

- Insurance Hires Their Appraiser: The insurance company selects their own independent appraiser (not the original adjuster).

- The Negotiation: The two appraisers review the data. If they agree on a value, that number is final.

- The Umpire: If the two appraisers cannot agree, they select a third-party “Umpire.” The Umpire reviews both arguments, and a decision joined by any two of the three parties becomes the binding settlement.

Why This Favors the Consumer

The Appraisal Clause moves the decision-making power away from the insurance company’s internal software and into the hands of real-world experts. In the vast majority of cases, the independent appraisal results in a significantly higher settlement than the initial offer.

6. Common Insurance “Low-Ball” Tactics to Watch For

Insurance companies are businesses focused on the bottom line. Watch out for these common psychological and technical tactics:

- The “Final Offer” Bluff: Adjusters will often say, “This is the maximum the system allows.” This is false. Systems have overrides, and the Appraisal Clause bypasses the system entirely.

- The Storage Threat: They may tell you they will stop paying for your rental car or storage fees if you don’t accept the offer within 72 hours. While they can limit rental days, they cannot force you to accept an unfair valuation under duress.

- Ignoring Local Market Trends: If you live in an area where 4WD trucks are in high demand (like Colorado or Montana), but the insurer uses national averages, they are under-valuing the local “market readiness” of your vehicle.

7. The Role of an Independent Appraiser

Why should you spend money to hire a professional? Can’t you just show the adjuster a few KBB screenshots?

Unfortunately, adjusters are trained to dismiss consumer-grade data. An Independent Certified Appraisal provides:

- USPAP Compliance: Our reports follow the Uniform Standards of Professional Appraisal Practice, making them legally robust.

- Market Analytics: We use actual “sold” data from dealer auctions and retail markets that the public cannot access.

- Expert Testimony: If your case ever went to court, a certified appraiser serves as an expert witness.

- Higher ROI: The increase in the settlement almost always dwarfs the cost of the appraisal fee.

8. Specific Considerations for Different Vehicle Types

Not all total losses are created equal. Depending on what you drive, the valuation process varies.

Luxury and Exotic Vehicles

Software like CCC is notoriously bad at valuing Maseratis, Porsches, or high-end Mercedes-Benz models. These cars rely heavily on specific options (like Carbon Fiber packages) that “standard” software often ignores.

Classic and Collector Cars

If you were driving a vintage Mustang or a classic Porsche when the accident occurred, a standard ACV policy is your enemy. These cars often require “Agreed Value” policies. If you have a standard policy, you must have an independent expert who understands the collector market to fight for the “diminished value” or total loss worth.

Electric Vehicles (EVs)

The EV market is volatile. Battery health and software versions (like Tesla’s Full Self-Driving) are massive value drivers that insurance companies frequently overlook in their reports.

9. Sales Tax, Title, and License Fees

One of the most overlooked aspects of a total loss settlement is the “Tax, Title, and License” (TT&L).

In many states, the insurance company is legally required to pay you enough to replace the vehicle. This means they must add the applicable state sales tax, registration fees, and title transfer fees on top of the vehicle’s market value.

- Example: If your car is worth $20,000 and your state sales tax is 8%, the insurer owes you an additional $1,600.

- Always check your settlement summary for a line item regarding taxes. If it isn’t there, they may be trying to shortchange you.

10. Summary Checklist: What to Do Right Now

If your car was just totaled, follow this checklist to ensure you aren’t taken advantage of:

- Do Not Sign: Do not sign the power of attorney or the settlement release until you are satisfied with the number.

- Request the Valuation Report: Ask for the full 10-20 page breakdown, not just the summary.

- Audit the VIN Decode: Ensure every option and the mileage are 100% accurate.

- Research Comps: Find three local listings that prove your car’s worth.

- Calculate Taxes: Ensure sales tax and registration are included.

- Call a Professional: If the gap between their offer and the real-world price is more than $1,000, contact Auto Appraisal Expert.

Why Choose Auto Appraisal Expert?

At Auto Appraisal Expert, we aren’t just enthusiasts; we are certified professionals with years of experience in the automotive and insurance industries. We know the language the adjusters speak, and we know how to dismantle their low-ball reports using cold, hard data.

We have helped thousands of clients across the country recover millions of dollars in undervalued total loss claims. Our mission is simple: to level the playing field between the individual car owner and the massive insurance corporation.

Get a Free Consultation

Is your insurance company offering you a settlement that feels “off”? Don’t guess—get the facts. We offer a preliminary review of your insurance valuation report to determine if an independent appraisal is right for you.

Click here to contact us or call us today to speak with an appraiser. Let us help you get back on the road with the settlement you actually deserve.