Is your insurance company calling your car a “total loss” and offering a check that feels insultingly low? You’re not alone. This decision isn’t guesswork; it hinges on a specific calculation dictated by state law, known as the total loss threshold by state. Understanding this rule is the first step in leveling the playing field and fighting for the money you’re rightfully owed.

The Two Rules That Govern a Total Loss

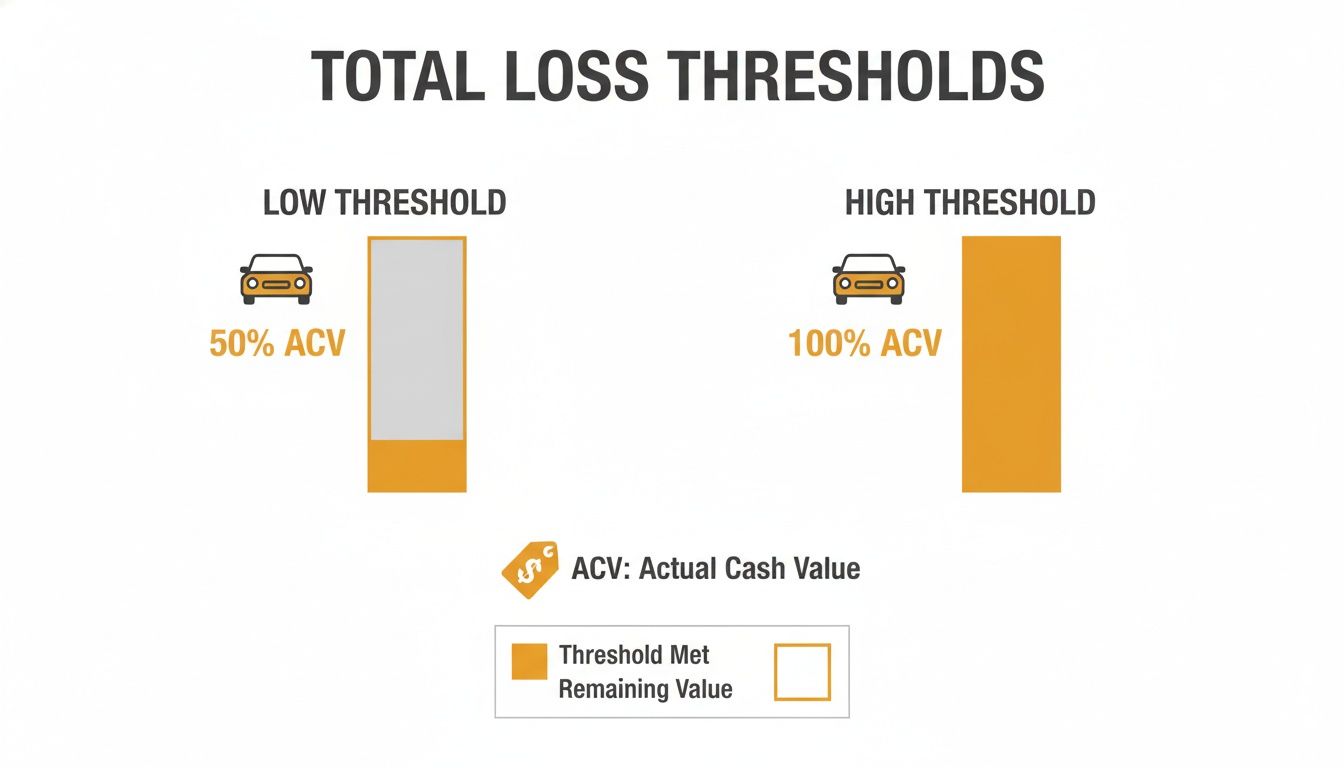

Every state has its own regulations, but they generally fall into one of two camps: a rigid Total Loss Threshold (TLT) or a more comprehensive Total Loss Formula (TLF).

A TLT is a straightforward percentage. If repair costs exceed, say, 75% of the car’s pre-accident value, it must be declared a total loss. The TLF, on the other hand, is an equation: Cost of Repairs + Salvage Value > Actual Cash Value. This formula gives the insurer more flexibility but can be complex for a stressed vehicle owner to decipher.

Why Actual Cash Value is the Real Battleground

No matter which rule your state uses, the entire calculation depends on one crucial figure: your vehicle’s Actual Cash Value (ACV). ACV is an industry term for the fair market value of your vehicle the moment before the accident happened.

This is where the fight usually begins. An insurance company’s low-ball ACV can wrongly force a repairable car into a total loss. Worse, it means you’re stuck with a check that’s thousands of dollars less than what it actually costs to replace your vehicle, a classic tactic we see from billion-dollar insurers.

This chart shows how much the threshold can vary, but it also highlights that an accurate ACV is the foundation of any fair settlement.

As you can see, a low threshold state and a high threshold state handle claims very differently, but both are powerless to give you a fair outcome if the starting value—the ACV—is wrong.

Total Loss Threshold By State Quick Reference (2026)

This table gives you a quick, scannable reference for the total loss threshold by state. Use it to find out if your state uses a percentage-based TLT or the more complex TLF. This is the first piece of information you need before you even think about talking to an adjuster.

| State | Total Loss Threshold (%) | Governing Rule (TLT vs. TLF) |

|---|---|---|

| Alabama | 75% | TLT |

| Alaska | TLF | TLF |

| Arizona | TLF | TLF |

| Arkansas | 70% | TLT |

| California | TLF | TLF |

| Colorado | 100% | TLT |

| Connecticut | TLF | TLF |

| Delaware | TLF | TLF |

| Florida | 80% | TLT |

| Georgia | TLF | TLF |

| Hawaii | TLF | TLF |

| Idaho | TLF | TLF |

| Illinois | TLF | TLF |

| Indiana | 70% | TLT |

| Iowa | 50% | TLT |

| Kansas | 75% | TLT |

| Kentucky | 75% | TLT |

| Louisiana | 75% | TLT |

| Maine | TLF | TLF |

| Maryland | 75% | TLT |

| Massachusetts | TLF | TLF |

| Michigan | 75% | TLT |

| Minnesota | 70% | TLT |

| Mississippi | 75% | TLT |

| Missouri | 80% | TLT |

| Montana | TLF | TLF |

| Nebraska | 75% | TLT |

| Nevada | 65% | TLT |

| New Hampshire | 75% | TLT |

| New Jersey | TLF | TLF |

| New Mexico | TLF | TLF |

| New York | 75% | TLT |

| North Carolina | 75% | TLT |

| North Dakota | 75% | TLT |

| Ohio | TLF | TLF |

| Oklahoma | 60% | TLT |

| Oregon | 80% | TLT |

| Pennsylvania | TLF | TLF |

| Rhode Island | TLF | TLF |

| South Carolina | 75% | TLT |

| South Dakota | 75% | TLT |

| Tennessee | 75% | TLT |

| Texas | 100% | TLT |

| Utah | TLF | TLF |

| Vermont | TLF | TLF |

| Virginia | 75% | TLT |

| Washington | TLF | TLF |

| West Virginia | 75% | TLT |

| Wisconsin | 70% | TLT |

| Wyoming | 75% | TLT |

This table is your starting point. To truly understand how insurers use these numbers and how you can fight back, check out our complete guide to handling a total loss claim.

How to Dispute a Total Loss Threshold By State

To fight for a fair settlement, you first have to understand the math the insurance company is using. Their decision to “total” your car isn’t arbitrary; it’s a cold calculation based on one of two methods allowed by your state: the Total Loss Threshold (TLT) or the Total Loss Formula (TLF).

Knowing which method your state uses—and how to challenge the numbers—is the key to getting what you’re truly owed.

The TLT is a straightforward percentage rule. If the estimated repair cost hits a specific percentage of your car’s pre-accident value, state law mandates it be declared a total loss.

Let’s look at a quick example of a Total Loss Threshold:

- Your Car’s Pre-Accident Value (ACV): $20,000

- Your State’s TLT: 75%

- The Threshold for Total Loss: $15,000 (75% of $20,000)

In this scenario, if the body shop’s repair estimate is $15,000 or higher, the insurance company has no choice but to total the vehicle.

The Total Loss Formula (TLF) Explained

The second method, the Total Loss Formula (TLF), is more nuanced and gives the insurer wiggle room. This formula lets them factor in what they can get for your wrecked car at a salvage auction.

Here’s the equation: (Cost of Repairs + Salvage Value) ≥ Actual Cash Value

Salvage Value is an industry term for the junk value of your car that the insurer pockets after selling the wreck. If the cost to fix your car plus its scrap value is more than its pre-accident worth, it’s smarter for them to just write you a check.

The Number That Matters Most: Actual Cash Value (ACV)

Both the TLT and TLF calculations pivot on one critical, and almost always disputed, number: the Actual Cash Value (ACV). This isn’t what you paid for the car or the dealer’s sticker price. It’s supposed to be the true market value of your vehicle one second before the impact.

The insurer’s first ACV offer is just that—an offer. It’s generated by valuation software like CCC ONE that is notorious for missing details that make your car valuable:

- Recent Upgrades: Did you just spend $1,500 on new tires or a premium sound system?

- Exceptional Condition: Was your vehicle garage-kept, smoke-free, and meticulously maintained?

- Local Market Demand: Is your specific truck or SUV a hot seller in your area, commanding a higher price?

Insurers are in the business of minimizing payouts. Their software is a starting point, not the final law. It is often built to find the lowest possible ACV, instantly shaving thousands off your car’s value. A lower ACV not only reduces your settlement but also makes it much easier to declare your car a total loss.

An independent market valuation report from a certified appraiser is the evidence you need to dismantle an insurer’s lowball offer. It’s your single most powerful tool for ensuring the total loss threshold by state is applied to a fair starting number. To dig deeper, check out our Total Loss & Appraisal Clause Page.

Why The 75 Percent Threshold Is A Common Standard

If you’ve ever looked at a list of total loss thresholds by state, you’ll see one number pop up again and again: 75%. This isn’t a random figure. It’s an intentional standard designed to create a financial buffer against unpleasant surprises.

The whole point is to protect both you and the insurer from a repair job that spirals out of control. Mechanics almost always find hidden damage once they start tearing a car down. The 75% rule creates a built-in 25% cushion to absorb those unexpected costs before the repair bill exceeds what the car is actually worth.

A Widespread And Established Practice

The 75% rule is the go-to standard for a reason: it gives adjusters and body shops a consistent, predictable framework. A quick look across the country shows just how dominant this figure is.

Roughly 20 states—including major ones like New York, Michigan, Maryland, and Virginia—have adopted this threshold. You can see a full comprehensive state-by-state breakdown to check the specific rules for your area.

How A Small ACV Dispute Changes Everything

On paper, the 75% rule seems fair. But its logic falls apart the second the insurance company lowballs your car’s Actual Cash Value (ACV). Because the threshold is a percentage, every dollar they shave off your car’s value makes it drastically easier to total it out. This is why getting an independent car appraisal for your insurance claim is a smart investment.

Let’s walk through a real-world example:

- Correct ACV: $12,000

- 75% Threshold: $9,000

- Repair Estimate: $8,500

In this scenario, your car is repaired. The costs are high, but since they’re under the $9,000 threshold, you get your vehicle back.

But watch what happens when the insurer’s software undervalues your car:

- Insurer’s Lowball ACV: $11,000

- 75% Threshold: $8,250

- Repair Estimate: $8,500

Just like that, a $1,000 drop in value turns your repairable car into a mandatory total loss. A certified, USPAP-compliant market valuation report provides the evidence needed to correct the insurer’s numbers. Before you accept any settlement, get a free consultation to see if their math adds up.

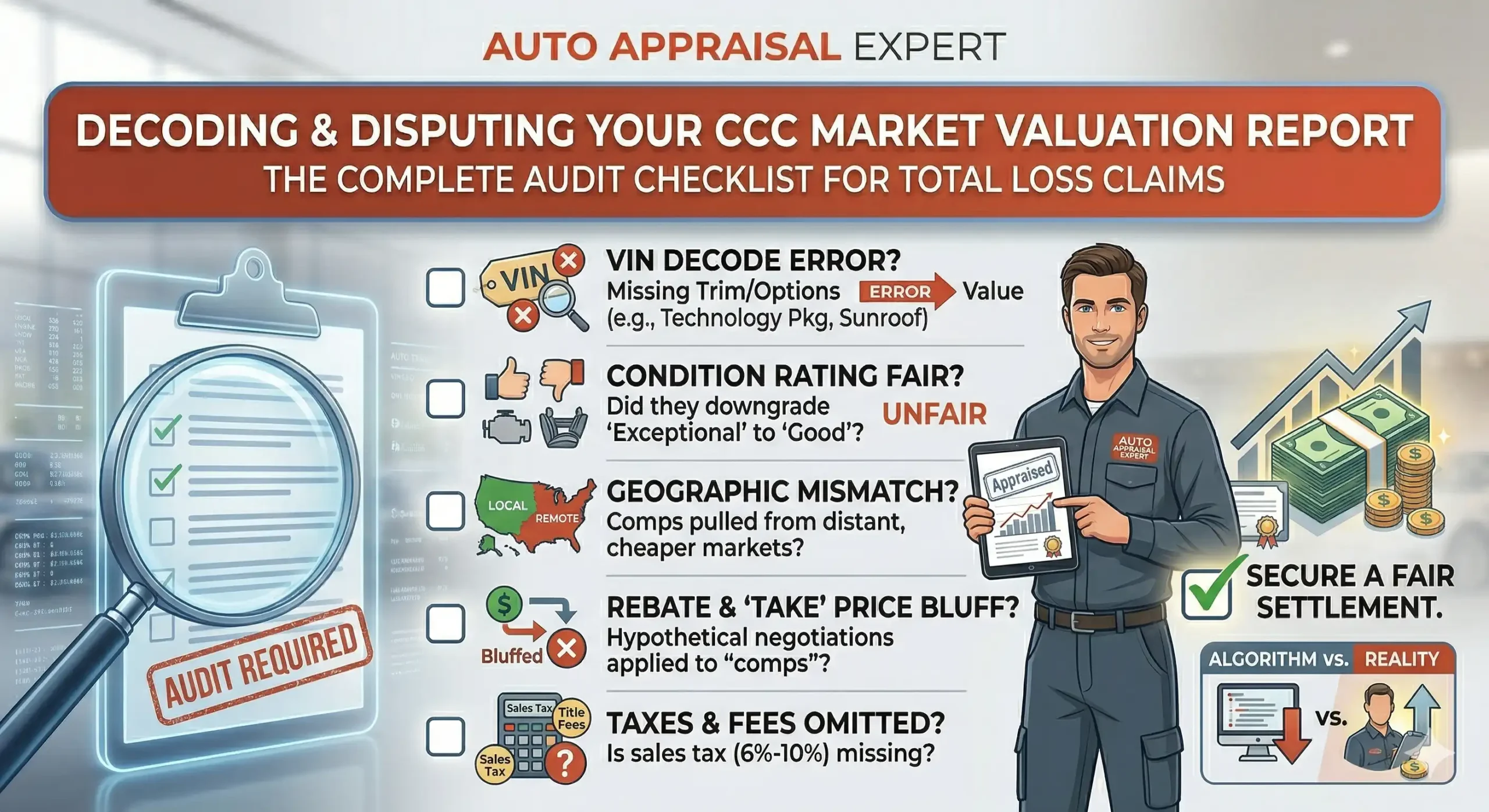

How To Dispute An Insurer’s Low Valuation Offer

Getting that total loss offer can be infuriating, especially when it feels insultingly low. The adjuster might present the settlement from software like CCC ONE as a final, non-negotiable figure. That’s a myth. The initial offer is their opening bid—and you have every right to challenge it.

You are in a much stronger position than they want you to believe. The process starts with one critical action: do not cash the settlement check. Cashing it can be legally seen as accepting their offer, slamming the door on any further negotiation.

Your Step-by-Step Action Plan

To effectively fight their valuation, you need to gather solid evidence, pinpoint their errors, and present a counter-offer built on hard facts.

- Request Their Full Valuation Report: Demand a complete copy of the report the insurer used to calculate your vehicle’s Actual Cash Value (ACV). Do not accept a one-page summary.

- Scrutinize the Report for Errors: Insurer-generated reports are often filled with errors that conveniently drive down your car’s value. Look for an incorrect trim level, wrong mileage, missing factory options, or unfair “condition adjustments.”

- Compile Your Own Evidence: Gather maintenance records, receipts for recent major work (like new tires), and the original window sticker. This paperwork proves you invested in the vehicle’s upkeep and contradicts claims of “average” condition.

The Ultimate Tool for a Fair Settlement

While your own research is vital, the single most powerful tool for winning a valuation dispute is a professional, independent appraisal.

An independent market valuation report is your proof. Our certified appraisers have found that insurers’ initial offers are often undervalued by $1,000 to $5,000 or more. This isn’t an accident; it’s a business model that relies on policyholders accepting the first offer.

To take control, you need a USPAP-compliant report from a certified independent auto appraiser. USPAP (Uniform Standards of Professional Appraisal Practice) is the quality-control standard recognized by courts and insurance carriers. A certified report is meticulously researched using real market data and dealer-sold comparables that stand up under scrutiny. This report becomes the bedrock of your counter-offer, giving you the leverage to formally reject their lowball number.

Invoking The Appraisal Clause In Your Policy

When you and your insurer are at a standstill over your vehicle’s value, it feels like a David-versus-Goliath battle. But buried in most auto policies is a powerful provision designed to level the playing field: the Appraisal Clause.

The Appraisal Clause is your contractual right to hire a certified professional to challenge the insurer’s valuation. It’s your policy’s built-in dispute resolution tool, and invoking it is the most effective way to fight a lowball total loss offer. It forces a fair, structured negotiation when a good-faith agreement isn’t happening.

How The Appraisal Clause Process Works

Once you formally invoke the clause in writing, a standardized process kicks off. The steps are designed to produce a final, binding outcome.

- You Hire Your Appraiser: You select and pay for a certified, independent auto appraiser to conduct an evidence-based valuation.

- The Insurer Hires Theirs: Your insurance company then chooses and pays for its own appraiser.

- The Two Appraisers Negotiate: The two experts compare reports, analyze market data, and attempt to reach an agreed-upon settlement.

- The Umpire Decides: If they can’t agree, they jointly select a neutral, third-party umpire who reviews both appraisals and makes the final, binding decision.

Invoking the Appraisal Clause takes the negotiation away from a claims adjuster and puts it into the hands of valuation experts. This simple action has the potential to increase your settlement by $1,000 to $5,000+.

Why A Certified Appraiser Is Non-Negotiable

This process is only as strong as your evidence. The insurer’s appraiser will use reports from systems like CCC ONE engineered to find the lowest possible value. To counter that, you can’t just show up with printouts from KBB.com.

Your entire case must be built on a USPAP-compliant market valuation report. This isn’t just an opinion—it’s a legally robust document prepared by a certified appraiser using real-world market data and dealer-sold comparables. By invoking the clause with a certified appraisal in hand, you completely change the power dynamic.

Whether your dispute involves a diminished value vs. total loss scenario or a direct challenge to the ACV, this is your path to a fair settlement. To see how we build an airtight case for our clients, check out our Total Loss & Appraisal Clause Page.

Understanding Diminished Value Vs Total Loss

What happens if your car isn’t declared a total loss, but you know its value has plummeted because of the accident? This highlights a critical distinction: the difference between a total loss and diminished value.

A total loss is a clear-cut decision dictated by your state’s total loss threshold. It means repair costs are too high compared to your car’s pre-accident value. The insurer pays you the Actual Cash Value (ACV) and takes ownership of the wrecked vehicle.

When Your Repaired Car Is Worth Less

Diminished Value comes into play after your car has been repaired. It’s the measurable, permanent drop in your vehicle’s resale value caused by its new accident history. Even with flawless repairs, a vehicle with a damage record is simply worth less than an identical one with a clean history.

Think of it this way: you’re shopping for a used car and find two identical models. The seller discloses that one was in a major collision but has been professionally repaired. Which one would you pay more for? That price gap is its diminished value.

Are You Owed for This Loss?

If another driver was at fault, you are almost certainly entitled to file a separate diminished value claim. This claim compensates you for the loss in market value that the at-fault party caused. Even if your claim doesn’t meet the total loss threshold by state, you could still be owed thousands of dollars—money that insurers will not voluntarily offer. Our Diminished Value Service Page can help you get back the money you’re rightfully owed.

FAQ: Your Total Loss Questions Answered

How do insurers calculate Actual Cash Value?

Insurance companies use third-party software like CCC ONE, which scours local dealer listings for “comparable” vehicles. The final number they present is the Actual Cash Value (ACV)—your car’s supposed pre-accident market worth. These automated systems often apply aggressive “condition adjustments” and miss high-value options, which is why an independent car appraisal for your insurance claim is crucial to establish the true market value.

Can I keep my car if it’s declared a total loss?

Yes, in most states, you have the option to “retain salvage.” The insurance company will pay you the ACV minus the vehicle’s salvage value—the cash they would have gotten at a scrap auction. Be warned: you’ll be issued a “salvage title” and must complete all state-mandated repairs and inspections before the vehicle is legally drivable, which can be a difficult process. For more on federal guidelines, you can check with the National Highway Traffic Safety Administration (NHTSA).

How long do I have to dispute a total loss offer?

You need to act fast, as timelines vary. The most important first step is to not cash the settlement check, as this is often considered acceptance of their offer. You should immediately notify the adjuster in writing that you are disputing the valuation and intend to get an independent appraisal. It’s best to start this process within a week or two of receiving their initial low offer.

Does the total loss threshold apply if the other driver was at fault?

Absolutely. The total loss threshold by state is the law and applies to every claim processed in that state, regardless of who caused the accident. The only real difference is which insurance company is paying. Your right to dispute their lowball valuation and hire an independent auto appraiser remains exactly the same.

Don’t leave money on the table. Get your free claim review or order a certified appraisal report today to take control of your insurance settlement.

About AutoAppraisalExpert

AutoAppraisalExpert is a premier provider of independent vehicle appraisal reports and insurance claim consulting. Our mission is to equip vehicle owners with the data-driven evidence required to recover the full financial value of their asset after an accident. Whether navigating a complex Diminished Value claim or disputing a low-ball Total Loss offer, we provide the certified documentation needed to negotiate with insurance companies from a position of strength.

With a national reach and deep industry expertise, we have helped thousands of policyholders identify errors in carrier valuation reports (like CCC) and invoke the Appraisal Clause to secure fair settlements. We pride ourselves on transparency, speed, and reports that stand up to the toughest insurer scrutiny.

Why Trust This Guide

This guide was written and verified by the AutoAppraisalExpert technical team. Our appraisers specialize in total loss disputes and diminished value forensics. We stay current on state insurance regulations, court-accepted valuation practices, and evolving market trends to ensure our readers—and our clients—always have the most accurate information available.

Ready to see what your car is really worth? Get your free consultation today.