Is your insurance check lower than you expected after an accident? You’re not alone, and it’s a frustrating position to be in. You know your car was worth more, but proving it to a billion-dollar insurer can feel impossible. This is exactly where a professional car appraisal becomes your most powerful tool.

So, what is a car appraisal? It is a detailed, evidence-based valuation report prepared by a certified expert that establishes your vehicle’s true fair market value. Think of it not just as an opinion, but as the factual evidence you need to dispute an insurer’s lowball offer and negotiate a fair settlement.

Your First Line of Defense Against a Low Offer

When your car is declared a total loss, the insurance company calculates its Actual Cash Value (ACV). ACV is simply the amount they claim your car was worth moments before the crash. The problem is they often use valuation software like CCC ONE—a tool designed to serve their interests by minimizing payouts, not yours.

An independent auto appraiser dismisses their flawed algorithm. We conduct a thorough investigation into your specific vehicle and, most importantly, your local market. A professional car appraisal for insurance claim purposes is not a guess; it’s a financial assessment that analyzes real dealer-sold comparables and documents every feature to prove your car’s true worth.

Appraisal vs. Online Estimator: What’s the Difference?

It’s easy to confuse a real appraisal with a free online value estimator from a site like KBB, but they serve completely different purposes. One is a marketing tool, the other is a legal weapon for your insurance dispute.

| Feature | Professional Car Appraisal | Free Online Estimator (e.g., KBB) |

|---|---|---|

| Methodology | Detailed inspection, local market analysis, real-time dealer-sold comparable data. | Automated algorithm using national data averages and user-submitted info. |

| Authority | Legally binding in disputes, compliant with USPAP standards. | No legal standing. It is considered an opinion, not evidence. |

| Accuracy | Accounts for specific condition, high-value packages, maintenance, and local market demand. | Provides a general range, often missing specific trims and regional price variations. |

| Use Case | Insurance claim disputes (total loss & diminished value), legal proceedings, financing. | Getting a quick trade-in estimate or a general idea of your car's value. |

Ultimately, a professional market valuation report is built to be scrutinized by adjusters and courts. An online estimate is not.

When Do You Need a Professional Car Appraisal?

A certified appraisal is your best asset in two common post-accident scenarios. Figuring out which one applies to you is the first step toward getting the money you’re owed.

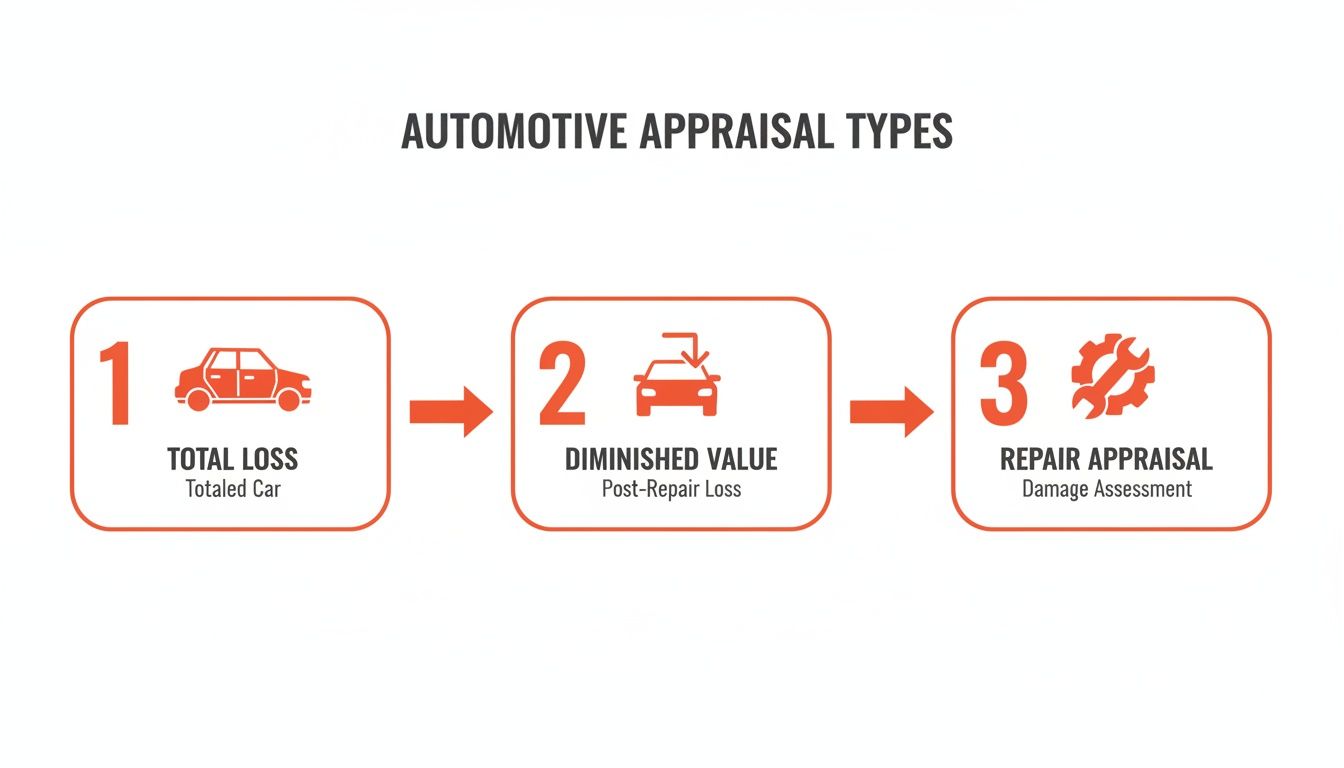

- Total Loss Disputes: The insurer declares your car a total loss, but their settlement offer is too low to buy a comparable replacement. A total loss appraisal provides the hard evidence you need to negotiate a much higher payout. For a deeper dive, read our guide on what happens if insurance totals your car.

- Diminished Value Claims: Your car was repaired, but its accident history now makes it worth less. This is diminished value vs. total loss. A DV appraisal quantifies that financial loss, empowering you to file a claim to recover it.

The Appraisal Clause: Almost every auto insurance policy has an “Appraisal Clause.” This is a contractual right that allows you to hire your own independent auto appraiser if you disagree with the insurer’s valuation. It levels the playing field and stops them from forcing an unfair offer on you.

A professional market valuation report is built to withstand an insurer’s toughest challenges because it’s prepared in compliance with the Uniform Standards of Professional Appraisal Practice (USPAP). This makes it a credible, legally sound document that stands up under insurer scrutiny. By using real-world, dealer-sold comparable vehicles, the report proves what a real buyer would have paid. It’s this evidence-based approach that provides the potential to increase your settlement by $1,000 to $5,000+.

The Two Main Types of Appraisals for Insurance Claims

When you’re fighting an insurance company, “car appraisal” isn’t a one-size-fits-all term. It’s your specific weapon for two very different financial battles. Understanding which type of appraisal you need is the first step to taking back control.

Let’s break down the two main situations where an independent auto appraiser becomes your most important ally: when your car is declared a total loss and when it’s repaired but has lost value (diminished value).

Total Loss Appraisals When Your Car Is Written Off

A Total Loss Appraisal is your counter-offer after the insurer declares your car a total loss and gives you a lowball settlement. Their entire goal is to close the claim for the lowest amount possible, which they justify with their Actual Cash Value (ACV) calculation. In short, ACV is just what they say your car was worth moments before the crash.

This number is almost always generated by software, like CCC, that is built to serve the insurance carrier—not you. The system often pulls inappropriate “comparable” vehicles, applies unfair condition penalties, or ignores valuable options. An independent total loss appraisal is designed to dismantle this flawed valuation with a report built on facts and real-world market data.

A certified appraiser builds a powerful case for your vehicle’s true value by:

- Scouring Your Local Market: We find real cars for sale at dealerships in your area, not from a national database.

- Documenting Pre-Accident Condition: We carefully account for your car’s actual condition, mileage, maintenance history, and every single factory option.

- Creating an Ironclad Report: You get a professional, evidence-based document that proves what a real person would have actually paid for your exact car.

This professional market valuation report gives you the leverage to demand a higher settlement—one that lets you buy a truly comparable replacement.

Diminished Value Appraisals for Repaired Vehicles

But what happens if your car is repaired, not totaled? Even with perfect bodywork, your car is now permanently branded with an accident history that kills its resale value. This is where a Diminished Value Appraisal comes into play.

Inherent Diminished Value is the automatic drop in market value a car suffers just because it’s been in a wreck. A car appraisal for insurance claim scenarios like this one calculates that exact financial loss. A professional appraiser determines the dollar-amount difference between your car’s market value before the accident and its value after the repairs are done.

This loss is real money, and in most states, you are legally entitled to be paid for it if the other driver was at fault. A diminished value appraisal from a provider like SnapClaim gives you the certified proof you need to file a formal claim and get that money back. The decision to total a car is based on the total loss threshold—the damage-to-value percentage where an insurer must declare it a loss. This threshold varies by state, which you can learn about in our guide on the total loss threshold by state.

How a Professional Car Appraisal Actually Works

So, how does a professional appraiser actually determine your vehicle’s true value? It’s not about clicking a button on some automated software. It’s an investigation built on hard evidence—the key to proving the insurance company’s initial offer is just a starting point for negotiation.

For an appraisal to hold any weight with an insurer, it absolutely must be compliant with the Uniform Standards of Professional Appraisal Practice (USPAP). This is a non-negotiable set of ethical and performance standards for appraisers, ensuring our conclusions are objective, well-supported, and built to withstand scrutiny.

The Foundation: Real-World Market Data

This is where a professional appraisal shines and separates itself from an insurer’s lowball report. We don’t use national averages or questionable auction data. Instead, our appraisers perform a deep analysis of your local sales market to determine your car’s true fair market value.

A professional market analysis prioritizes dealer-sold comparable vehicles. Why? Because these represent what a real person actually paid for a similar car in a retail setting—the same setting you’d use to replace your vehicle. This is the gold standard for proving value.

Our report builds an undeniable case using concrete facts. We identify several comparable vehicles for sale or recently sold at dealerships near you. Then, we make precise, documented adjustments to their prices based on differences in mileage, options, and condition to arrive at a value for your car. This transparent method shows exactly how we arrived at the number, creating a defensible figure that forces the insurer to take your claim seriously.

Invoking the Appraisal Clause: Your Right to a Fair Fight

Buried in the fine print of most auto insurance policies is your secret weapon: the Appraisal Clause. This clause is your contractual right to dispute an insurer’s valuation by bringing in your own independent expert. It’s your legal tool to force a fair negotiation.

Think of the Appraisal Clause as your official right to a second opinion. When you and your insurer are at a standstill over your car’s value, this clause moves the argument out of the adjuster’s hands and into a structured, fair process.

Activating Your Right to Dispute

Invoking the Appraisal Clause is a formal step that forces the insurance company to come to the negotiating table as an equal. Here’s how the process typically plays out:

- You Hire an Appraiser: You hire your own independent, certified appraiser to create a detailed market valuation report.

- The Insurer Hires an Appraiser: Your insurance company is then required to hire its own appraiser to do the same.

- The Experts Negotiate: The two appraisers present their evidence and work to agree on the vehicle’s true value.

- An Umpire Steps In (If Necessary): If they can’t agree, they select a neutral third-party expert, an “umpire,” who makes a final, binding decision.

This process completely levels the playing field. An adjuster can easily dismiss your complaints, but they can’t ignore a formal appraisal submitted as part of this contractual process. Our USPAP-compliant appraisals are designed to be undeniable evidence in this exact fight, providing the deep analysis that stands up to intense insurer scrutiny.

Conclusion: Take Control of Your Claim

Understanding what is a car appraisal is the first step toward justice. It’s not just a number; it’s a meticulously crafted, evidence-based report that gives you the power to challenge an insurance company’s lowball offer. Systems like CCC ONE are a starting point, not the final authority. Your policy’s Appraisal Clause gives you the right to demand a fair valuation based on real market data.

A professional appraisal is an investment that provides the evidence needed to negotiate. It often uncovers $1,000 to $5,000+ in additional value that adjusters may overlook, transforming your claim from a point of frustration to a position of strength.

Don’t leave money on the table. Get your free claim review or order a certified appraisal report today to take control of your insurance settlement.

Frequently Asked Questions (FAQ)

What is the purpose of a car appraisal for an insurance claim?

The purpose of a car appraisal for an insurance claim is to determine the vehicle’s true fair market value. It serves as independent, expert evidence to dispute an insurer’s low settlement offer for either a total loss or a diminished value claim, ensuring the policyholder can negotiate for the full amount they are owed.

How do I start the appraisal process for a total loss?

First, formally notify your insurance carrier in writing that you are disputing their valuation and invoking the Appraisal Clause in your policy. Next, hire a certified, independent auto appraiser. They will prepare a USPAP-compliant market valuation report to submit to the insurance company and begin negotiations on your behalf.

What is the difference between diminished value vs. total loss?

A total loss occurs when a vehicle’s repair costs exceed a certain percentage of its value (the total loss threshold), and the insurer pays you its pre-accident value. Diminished value applies to a repaired vehicle; it’s the loss in resale value your car suffers simply because it now has an accident history, even after perfect repairs.

How much value does a professional appraisal add?

While there are no guarantees, a professional appraisal often uncovers $1,000 to $5,000 or more in additional value. Appraisers identify errors in the insurer’s report—like missed options, incorrect comps, or unfair condition adjustments—and use real market data to provide the evidence needed to negotiate a higher settlement.

About AutoAppraisalExpert

AutoAppraisalExpert is a premier provider of independent vehicle appraisal reports and insurance claim consulting. Our mission is to equip vehicle owners with the data-driven evidence required to recover the full financial value of their asset after an accident. Whether navigating a complex Diminished Value claim or disputing a low-ball Total Loss offer, we provide the certified documentation needed to negotiate with insurance companies from a position of strength.

With a national reach and deep industry expertise, we have helped thousands of policyholders identify errors in carrier valuation reports (like CCC) and invoke the Appraisal Clause to secure fair settlements. We pride ourselves on transparency, speed, and reports that stand up to the toughest insurer scrutiny.

Why Trust This Guide

This guide was written and verified by the AutoAppraisalExpert technical team. Our appraisers specialize in total loss disputes and diminished value forensics. We stay current on state insurance regulations, court-accepted valuation practices, and evolving market trends to ensure our readers—and our clients—always have the most accurate information available.

Ready to see what your car is really worth? Get your free estimate today.