Meta Title: Auto Diminished Value Guide. Recover More Today

Meta Description: Auto diminished value explained clearly. Learn your rights, challenge low offers, and get help recovering your car’s lost value today.

Your car is repaired. It looks fine. Then the insurance offer arrives, and something feels off.

That reaction is often correct. Auto diminished value is the hidden loss many owners discover only after the body work is done and the resale market treats their car differently than a clean-history vehicle. Insurers know this issue well. Most owners do not, at least not until they are trying to sell, trade, or dispute a low claim offer.

The fight comes down to two playbooks. The insurer’s playbook is speed, formulas, and narrow valuation rules. The owner’s playbook is documentation, real comparables, and an independent car appraisal for insurance claim support when the carrier’s number does not reflect market reality.

If you are trying to understand diminished value vs. total loss, wondering whether a software valuation is final, or looking for a stronger market valuation report, this guide will help you take the next step with clarity. For broader claim background, see SnapClaim’s insurance claim resources.

What Is Auto Diminished Value and Why It Matters

Set two identical used cars on a dealer lot. Same year, same trim, similar mileage, same options. One has a clean history. The other shows a reported accident and repair history.

Most buyers will pay more for the clean-history car. That gap is auto diminished value.

The loss is real even after proper repairs

A repaired car can drive straight, look glossy, and pass a casual inspection. It can still be worth less because the accident history follows the VIN through vehicle history reports and buyer scrutiny.

According to this diminished value explanation citing appraiser observations and NAIC loss estimates, experienced inspectors often detect signs of a major accident, reducing a vehicle’s value by up to 50% for subpar repairs and over 20% even for perfect repairs, and the NAIC estimates these losses average 10% to 20% of the direct repair cost.

Two forms of diminished value matter most

Inherent diminished value is the loss caused by accident stigma alone. The repairs may be excellent, but the market still discounts the car because it now has an accident history.

Repair-related diminished value is different. That loss comes from poor repair quality, mismatched paint, alignment problems, panel fit issues, weld evidence, structural concerns, or other signs the vehicle was not restored correctly.

A stressed owner hears, “But the car was fixed.” That statement misses the point. Repairs address physical damage. They do not erase history, buyer caution, or dealer trade-in adjustments.

Why owners miss this loss

Most claim handling is built around repair cost, rental, and visible damage. Diminished value sits in a separate category. It is a market loss, not a repair line item.

That is why owners discover it late, when:

- Trading the car in: The dealer sees the history report and adjusts the number.

- Selling privately: Buyers compare your vehicle against clean-title alternatives.

- Reviewing a low claim offer: The carrier says the repairs made you whole, but the market says otherwise.

Key takeaway: If the accident history lowers what a buyer will pay today, that is a real economic loss even when the vehicle appears fully repaired.

Where diminished value fits with other claim concepts

It helps to separate a few terms:

| Term | Plain-English meaning |

|---|---|

| Actual Cash Value | The vehicle’s fair market value at the time of loss |

| Diminished Value | The drop in market value after repair because of accident history or repair issues |

| Total Loss Threshold | The state rule or insurer framework used to decide whether repair costs justify declaring a total loss |

| Subrogation | When an insurer seeks reimbursement from the party that caused the loss |

Owners also confuse diminished value vs. total loss. A total loss dispute focuses on whether the insurer properly valued a vehicle that was not repaired. A diminished value claim applies when the car is repaired but worth less afterward.

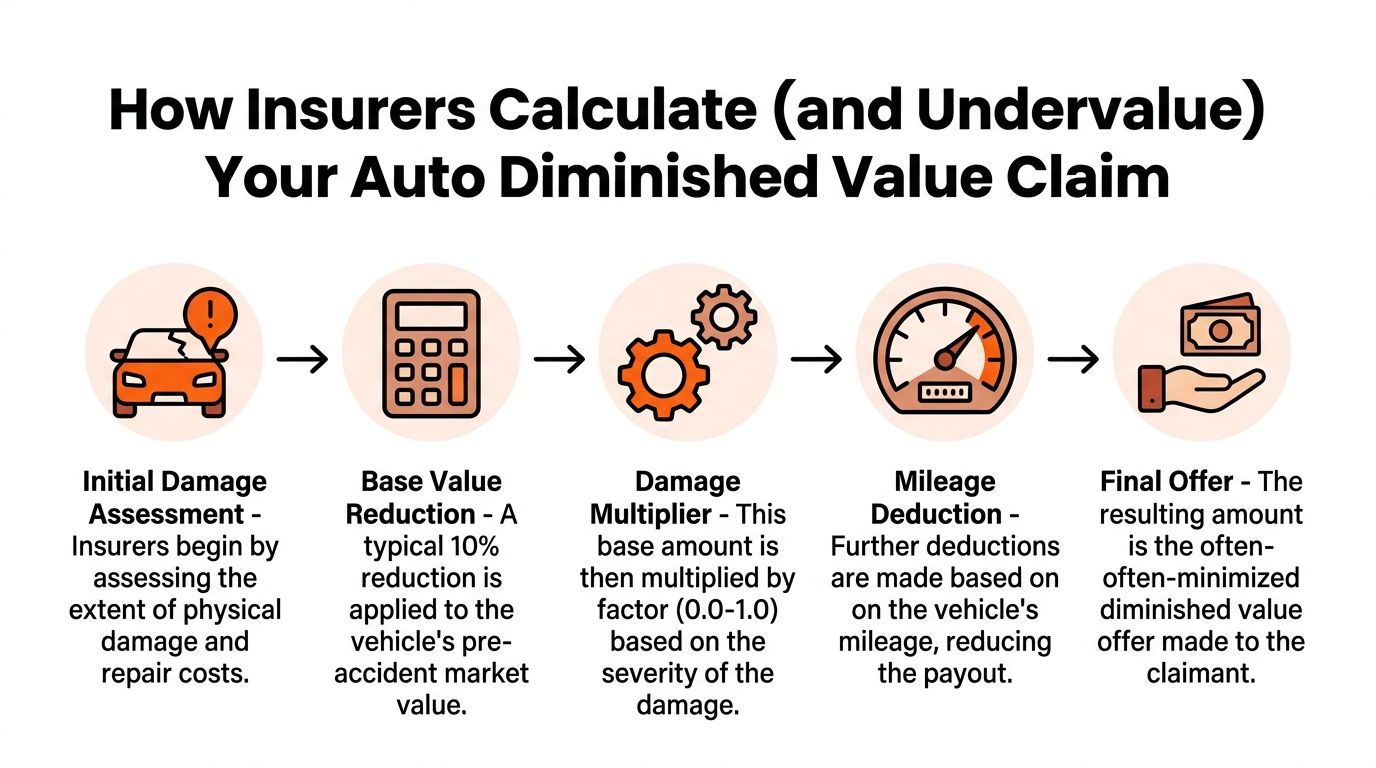

How Insurers Calculate (and Undervalue) Your Auto Diminished Value Claim

Insurers like repeatable systems. That is why many start with the 17c Formula, a method that became widely used after a Georgia case and is now a common benchmark in diminished value handling.

The problem is not that formulas exist. The problem is that owners often mistake the insurer’s first calculation for the true market answer.

The insurer playbook starts with a cap

The 17c Formula begins by capping the base loss at 10% of the vehicle’s pre-accident fair market value. Then it applies a damage multiplier and a mileage multiplier.

J.D. Power’s explanation of diminished value calculations gives a clear example: For a $30,000 vehicle, the formula caps the maximum loss at $3,000. If the insurer assigns 0.50 for moderate damage and 0.80 for 30,000 miles, the result is $1,200. J.D. Power also notes that experts criticize these caps as arbitrary because they ignore real market data.

What the formula looks like in practice

Here is the same structure in plain English:

Start with pre-accident value

A carrier estimates what your vehicle was worth before the crash.Apply the 10% cap

The formula immediately limits the possible claim.Reduce again for damage severity

Structural damage usually gets a higher multiplier than cosmetic repair.Reduce again for mileage

Higher mileage lowers the result further.

This is efficient for the carrier. It is not the same thing as a market analysis.

Why owners should question the result

The 17c Formula can be useful as a negotiating reference. It is weak as a measure of what real buyers pay in your market.

A buyer does not shop by saying, “I’ll discount this car because a formula used a mileage multiplier.” A buyer looks at history reports, repair disclosures, condition, trim, demand, and clean-history alternatives.

That gap between formula logic and market behavior is where many low offers come from.

The software issue owners run into

Many carriers also rely on valuation platforms and preset workflows. Programs such as CCC are tools, not judges. They can speed up claims handling, but speed is not the same as fairness.

Common carrier tactics include:

- Selecting weak comparables: Vehicles with different histories, condition profiles, or equipment can drag down the valuation.

- Leaning on formula outputs: The adjuster treats a starting number like a final answer.

- Focusing on repair completion: The carrier argues the invoice closed the file, even though resale stigma remains.

- Separating market reality from claim handling: If the software says one thing and local buyers say another, the owner has to prove the difference.

If you want to understand the math carriers use before challenging it, this guide on how to calculate diminished value is a useful reference.

Practical tip: The insurer’s number is a negotiating position. Treat it as the opening move, not the verdict.

What works better than arguing abstractly

Owners are at a disadvantage when they say, “My car is worth more,” without supporting data.

Owners gain an advantage when they present:

- dealer-sold comparables

- clean-history versus accident-history market examples

- repair documentation showing the severity and location of damage

- a certified independent valuation opinion

This is the core divide between the insurer’s playbook and the owner’s playbook. The insurer wants a controlled formula. The owner needs a market valuation report built on actual comparables.

For claim-specific background and broader strategy, SnapClaim’s diminished value page gives additional context on how these disputes develop.

Understanding Your Rights in Different States

Your rights depend on two things. Who caused the crash, and which state’s rules apply.

Those two facts determine whether you are dealing with a first-party claim or a third-party claim. A first-party claim is one against your own insurer. A third-party claim is one against the at-fault driver’s insurer.

The biggest state-law distinction

The clearest national rule comes from the NAIC research. The NAIC report on diminished value and state recovery rules explains that Georgia is the only state with clear legal precedent for first-party diminished value claims, and all other states (except Michigan) allow recovery from the at-fault driver’s third-party liability insurer because the insurer has a duty to make the claimant whole.

That means many owners do have a path to recover auto diminished value, but not always from their own carrier.

Why this changes strategy

If you are in Georgia, the analysis may include a first-party route against your own policy.

If you are outside Georgia, the stronger path is the at-fault driver’s liability carrier, assuming the facts and coverage line up. Michigan is the notable exception identified in the NAIC material.

This difference matters because owners often call their own insurer first, get little guidance, and assume the claim is impossible. Sometimes they are talking to the wrong carrier.

States without a standard formula

Many states do not give you a neat diminished value formula. That sounds frustrating, but it can help if the insurer is hiding behind a weak canned calculation.

In those states, proof becomes the center of the case:

- Pre-accident value evidence

- Post-repair market evidence

- Repair severity documentation

- An appraisal that measures the delta between before and after

A formula-free state does not mean a no-claim state. It means your evidence has to do more work.

Uninsured and underinsured issues

Some policies may allow diminished value recovery through uninsured motorist coverage, depending on the contract language and state law. Policy wording matters here. So does timing.

If coverage is disputed, look closely at the declarations page, endorsements, and any appraisal or dispute-resolution language. The issue is less about broad assumptions and more about what your policy says.

Practical tip: Before arguing value, confirm the claim path. Wrong carrier, wrong coverage theory, or wrong state assumption can stall an otherwise strong case.

Where to check your state rules

A good next step is your state insurance regulator. For example, the California Department of Insurance consumer resources can help you review claim rights, complaint options, and policy handling questions if your claim involves California.

If your dispute may overlap with a total loss question, this resource on total loss threshold by state can help separate repairability issues from diminished value recovery.

A Step-by-Step Guide to Documenting and Filing Your Claim

Strong diminished value claims begin with a clean file.

If the insurer has a thin file and you have a thick one, the negotiation changes. That is especially true when the carrier tries to minimize damage severity or treat the repair invoice as the end of the story.

Start with the basic claim file

Gather every document tied to the accident and repair.

- Crash documentation: Police report, claim number, date of loss, and the at-fault driver’s insurance details.

- Photos before and during repairs: Keep images of the damage before teardown if you have them. Repair-stage photos can be valuable.

- Final repair invoice: This is one of the most important records in the file.

- Vehicle history report: It helps show how the accident is now attached to the vehicle’s record.

- Ownership and vehicle details: Registration, VIN, mileage, trim, options, and any recent maintenance or condition evidence.

Why the repair invoice matters so much

Kelley Blue Book’s diminished value guidance notes that the 17c framework uses damage multipliers ranging from 1.0 for severe structural damage down to 0.25 for minor cosmetic issues, with 0.75 for major structural and panel damage and 0.50 for moderate damage. That is why your repair invoice matters. It shows what was repaired, where the damage occurred, and whether structural components were involved.

An owner who only sends photos is asking the insurer to guess. An owner who sends line-by-line repair documentation is showing the insurer exactly how serious the loss was.

Build your demand package in order

Use a clean sequence so the adjuster can follow your position.

Identify the claim

Include your claim number, vehicle details, date of loss, and liability facts.State the diminished value position

Say the vehicle sustained post-repair market loss due to accident history and, if applicable, the nature of repairs.Attach supporting records

Include photos, invoices, and any history report showing the accident now appears on record.Add your valuation evidence

This may be your own market research or, preferably, an independent appraisal.Request a written response

Ask the insurer to explain any denial or low offer in writing.

What not to do early

Owners weaken claims in predictable ways.

- Do not cash a check marked as full and final settlement if you disagree with the amount.

- Do not rely on phone conversations alone. Get positions in writing.

- Do not describe major repairs as minor just to seem cooperative.

- Do not skip the invoice review. Structural work hidden in abbreviations often changes the value discussion.

Expert advice: The first insurer response is a test of your file quality. If your package is weak, expect a denial or a token offer. If your package is organized and specific, the carrier has more work to do before dismissing it.

How to respond to a low offer

A low offer does not mean the claim lacks merit. It means the carrier is waiting to see whether you can support a higher number.

Respond by asking:

- What valuation method did you use?

- Which comparable vehicles did you rely on?

- Did you account for accident history stigma in the local market?

- Did you review the full repair invoice and damage location?

- Are you treating a formula result as a market conclusion?

That approach is more effective than saying the offer is unfair.

When the file starts to overlap with a total loss dispute

Sometimes the same owner is dealing with repair issues, diminished value, and questions about whether the vehicle should have been totaled. That is where diminished value vs. total loss becomes important.

If the carrier’s handling raises fair market value concerns beyond post-repair stigma, a broader valuation review may be necessary. For many owners, SnapClaim’s fair market value resource is a useful starting point for understanding how actual market value disputes are framed.

How an Independent Appraisal Wins Your Diminished Value Claim

At some point, many diminished value claims stop being a conversation and become a proof problem.

That is when an independent auto appraiser matters. The adjuster already has the insurer’s number. What changes the file is a competing valuation built on defensible methods and actual market evidence.

What a strong appraisal does

A proper diminished value appraisal does not just announce a number. It explains the number.

That includes:

- the vehicle’s pre-accident fair market value

- the vehicle’s post-repair market value

- the reasons buyers discount the repaired unit

- comparable market evidence supporting the difference

- analysis of damage severity, repair scope, mileage, trim, and condition

MWL’s discussion of third-party diminution claims notes that in states such as California (where there is no standardized formula), the basis for the claim relies on a professional car appraisal for insurance claim purposes. It also notes that insurers often use a rough 10% of NADA value as a starting point, while an independent market valuation report using real comparables can justify a higher loss.

Why this works better than arguing with formulas

A formula tells the insurer what it wants to pay under a standardized process.

A certified appraisal tells the insurer what the market evidence supports for your specific vehicle.

That difference is critical. Good appraisals use dealer listings, sold comparables when available, equipment matching, and market-based reasoning. They can also address repair context that a formula ignores, such as structural areas, premium trim, color desirability, or buyer sensitivity in a particular segment.

The Appraisal Clause matters

Many auto policies include an Appraisal Clause. In simple terms, it is a contract provision that gives the parties a formal path to resolve valuation disputes using appraisers.

Owners overlook this often. They assume the software printout or adjuster letter ends the issue. It does not. If your policy includes an appraisal process, that can become your point of influence.

A useful overview of this process is available in this guide to the insurance claim appraisal process.

Key takeaway: The most effective response to a low diminished value offer is not frustration. It is a report the insurer must answer with substance.

What to look for in the report

Not every valuation document carries the same weight.

Look for a report that is:

- USPAP-compliant: That means it follows recognized appraisal standards.

- Specific to your vehicle: Not a generic template with broad assumptions.

- Comparable-driven: Real market evidence beats abstract opinion.

- Clear enough to survive scrutiny: The best reports can be read by adjusters, attorneys, and arbitrators without guesswork.

This is also where high-quality appraisal work can expose the value gap owners miss; in practice, a professional report identifies substantial additional value that a carrier or adjuster may overlook. This does not guarantee outcome, but it often gives the owner the evidence needed to negotiate with far more authority.

Frequently Asked Questions About Auto Diminished Value

Is auto diminished value the same as a total loss dispute

No. Auto diminished value applies when the vehicle is repaired but worth less afterward. A total loss dispute focuses on whether the insurer correctly valued a vehicle that was declared a total loss, or whether the total loss decision itself was proper.

The evidence overlaps, but the claim theory is different.

Can I recover diminished value if the repairs look perfect

Yes. A perfect-looking repair does not erase accident history. In many claims, the loss comes from stigma attached to the vehicle’s record, not visible flaws.

That is why owners should not accept “it was fixed” as a complete answer.

Do I need an appraiser for every claim

Not every claim, but many serious disputes become much stronger with one. If the insurer denies the claim, offers a very low number, or relies on a generic formula without meaningful market support, an independent appraisal becomes the best next step.

A strong appraisal is useful when the vehicle is newer, has meaningful pre-loss value, or sustained significant repair work.

What is Actual Cash Value

Actual Cash Value, often shortened to ACV, means the vehicle’s fair market value at the time of loss. In a total loss case, ACV is the core number that drives the settlement. In a diminished value claim, pre-accident ACV can also be part of the analysis because it helps establish what the vehicle was worth before the crash.

Does the insurer’s software have the final say

No. Valuation software is a tool. It is not law, and it is not the market itself.

Insurers use software because it creates speed and consistency. Owners challenge software outputs when the comparables are weak, the condition adjustments are wrong, or the resulting number does not match real-world buyer behavior.

What makes a diminished value claim stronger

The strongest files include:

- Clear liability facts

- Complete repair invoices

- Photos showing the original damage

- Evidence the accident now appears on history reports

- A professional market valuation report or independent appraisal

The more your evidence looks like a valuation file instead of a complaint, the better your position.

Take Control of Your Settlement

The insurer’s playbook is predictable. Limit the claim. Use a standardized formula. Treat the first number as if it ends the discussion.

Your playbook should be different. Confirm the correct claim path. Build the file carefully. Use repair records, buyer-facing market evidence, and a certified valuation when the insurer’s number does not hold up.

That is how owners close the value gap. Not by arguing louder, but by replacing the carrier’s assumptions with proof.

If you are dealing with auto diminished value, keep one point in mind. A repaired car can still be worth less, and the first insurance position is rarely the final word when the file is strong enough to challenge it. The same principle applies in related valuation disputes involving diminished value vs. total loss, disputed ACV, or a lowball software-generated number.

Don’t leave money on the table. Get your free claim review or order a certified appraisal report today to take control of your insurance settlement.

About AutoAppraisalExpert

AutoAppraisalExpert is a premier provider of independent vehicle appraisal reports and insurance claim consulting. Our mission is to equip vehicle owners with the data-driven evidence required to recover the full financial value of their asset after an accident. Whether navigating a complex Diminished Value claim or disputing a low-ball Total Loss offer, we provide the certified documentation needed to negotiate with insurance companies from a position of strength.

With a national reach and deep industry expertise, we have helped thousands of policyholders identify errors in carrier valuation reports (like CCC) and invoke the Appraisal Clause to secure fair settlements. We pride ourselves on transparency, speed, and reports that stand up to the toughest insurer scrutiny.

Why Trust This Guide

This guide was written and verified by the AutoAppraisalExpert technical team. Our appraisers specialize in total loss disputes and diminished value forensics. We stay current on state insurance regulations, court-accepted valuation practices, and evolving market trends to ensure our readers, and our clients, always have the most accurate information available.

Ready to see what your car is really worth? Get your free estimate today.

If your insurer is minimizing your auto diminished value claim, Auto Appraisal Expert can help you review the valuation, identify weak assumptions, and obtain a certified appraisal report that provides the evidence needed to negotiate from a stronger position.