Meta Title: Diminished Value Appraisal Near Me | Get a Fair Payout

Meta Description: Don’t settle for the insurer’s low offer. Learn how to find a certified appraiser and use a diminished value appraisal near me to boost your claim.

Has your car been in an accident, leaving you with a check from the insurance company that feels insultingly low? You followed the rules, got it repaired, but now it has an accident history that will slash its resale value. Your search for a “diminished value appraisal near me” is the first step toward reclaiming that lost money.

But here’s a critical piece of advice from an expert who has handled thousands of these claims: an appraiser’s zip code is one of the least important factors. While it feels logical to want someone local, what truly matters is their certification, methodology, and track record fighting—and winning—against billion-dollar insurance carriers. We’re here to level that playing field.

Why Expertise Beats Proximity in a Diminished Value Appraisal Near Me

Your ultimate goal is to hand the insurance adjuster a report so solid and well-documented that they simply cannot dismiss it. While having a local appraiser physically inspect your car might feel reassuring, the real power of a diminished value claim lies in the report’s data and logic—not the appraiser’s location. A physical inspection for inherent diminished value is often redundant in 2026. The crucial evidence—the repair invoices, insurance estimate, and post-repair photos—is already documented. A specialist can analyze this from anywhere and build a stronger case based on verifiable market data.

At its core, your claim is for inherent diminished value. This is the automatic drop in your car’s resale value just because it now has a permanent accident history. Even with flawless repairs, savvy buyers will demand a steep discount, and calculating that loss accurately is a specialized skill.

The Specialist Advantage: Why a National Expert Wins

A certified national specialist offers a level of expertise that most local generalists cannot match. Their entire business is built around dissecting the fine print of insurance disputes and delivering evidence that stands up to intense scrutiny.

- USPAP-Compliant Reports: They produce appraisals that strictly follow the Uniform Standards of Professional Appraisal Practice (USPAP). USPAP is the federally recognized set of ethical and performance standards for the appraisal profession. This makes your claim incredibly difficult for an insurer to challenge on a technicality.

- Real Market Data Analysis: Specialists don’t just pull numbers from online estimators. They dig into extensive databases of dealer-sold comparables and real-time auction results. This process uncovers what similar wrecked-and-repaired cars actually sell for, providing concrete proof of the value loss.

- Experience with Insurer Tactics: A national expert has battled every major insurance carrier hundreds of times. They know the go-to lowball formulas, like the infamous 17c Formula, and build their reports to dismantle those arguments before the adjuster can even make them. The 17c Formula is a simplistic calculation insurers use to minimize payouts, which has no basis in real market conditions.

A report’s authority comes from its data and methodology. A well-documented appraisal from a certified expert in another state is far more powerful than a poorly supported one from a local appraiser down the street.

The takeaway is clear: the most critical factors for a successful claim are the appraiser’s specialized expertise and the quality of their report, not their physical address. Choosing a certified specialist who provides a USPAP-compliant, data-backed market valuation report is the single most effective step you can take. It’s how you turn a weak position into a strong negotiation, with the potential to increase your settlement by $1,000 to $5,000+ by proving the real financial damage the accident caused.

How to Find a Truly Qualified Appraiser (Not Just One “Near Me”)

When you need to get a diminished value claim paid, a search for an “appraiser near me” seems logical, but be cautious. The results are often crowded with generalists, unqualified operators, and online services that use a simple formula—the kind of report an insurance adjuster will dismiss out of hand. You need an independent auto appraiser whose work is so thorough and evidence-based that it forces the insurance company to negotiate based on hard facts.

The Litmus Test: USPAP Compliance

Before you look at anything else, check for one crucial credential: USPAP certification. USPAP stands for the Uniform Standards of Professional Appraisal Practice. It is the quality control standard for the professional appraisal of property, ensuring the appraiser follows a strict, repeatable, and defensible methodology.

When an insurance adjuster sees a USPAP-compliant report, they know they can’t just brush it off. It signals you’ve hired a serious professional, and your car appraisal for insurance claim is built on a foundation of recognized industry standards.

Vet for Specialization and Real-World Experience

Not all appraisers are the same. Someone who appraises classic cars for auctions is great at their job, but they probably don’t know the first thing about countering the tactics used by a major insurer like Progressive or State Farm in a diminished value dispute. You need a specialist.

Here’s how to spot one:

- Diminished Value is Their Main Gig: Check their website. Is diminished value vs. total loss their primary service? Or is it just a bullet point on a long list of other offerings? You want a specialist who lives and breathes this stuff.

- They Have a Proven Track Record: Look for testimonials, case studies, or reviews that mention specific insurance carriers. An appraiser who has gone head-to-head with the big companies knows their arguments and how to dismantle them.

- They Are Transparent About Their Method: A real expert will tell you exactly how they determine the loss in value. They should be talking about using real-world dealer-sold comparables and market data—not a junk formula like 17c.

A major red flag is any appraiser who “guarantees” a specific payout. A true professional guarantees one thing: an ironclad, evidence-based report. Our reports provide the evidence needed to negotiate; we never promise guaranteed outcomes.

The Proof Is in the Report—Ask for a Sample

The absolute best way to judge an appraiser is to see their work. Ask for a sample market valuation report before you even think about hiring them. This is your only window into the quality of what you’re paying for.

When you get the sample, look for these signs of a professional report:

- Vehicle Details are Meticulous: Does it list specific trim levels, optional packages, and detailed pre-accident condition ratings?

- Comparables are Real and Verifiable: Does the report show actual vehicles that recently sold, complete with links or screenshots? Or does it just pull vague values from sources like Kelley Blue Book?

- Adjustments are Clearly Explained: Does the appraiser show their work, explaining why they added or subtracted value for mileage, condition, and options?

- It Tells a Cohesive Story: A strong report reads like a logical argument, connecting the collision and repairs directly to a specific loss in marketability, ending in a firm conclusion.

If the “report” you see is a one-page document with a number from a calculator, run. A legitimate, professional diminished value report is often 15-30 pages long, packed with data, analysis, and supporting evidence. To get a better sense of the principles involved, our guide on what a car appraisal is provides a solid foundation.

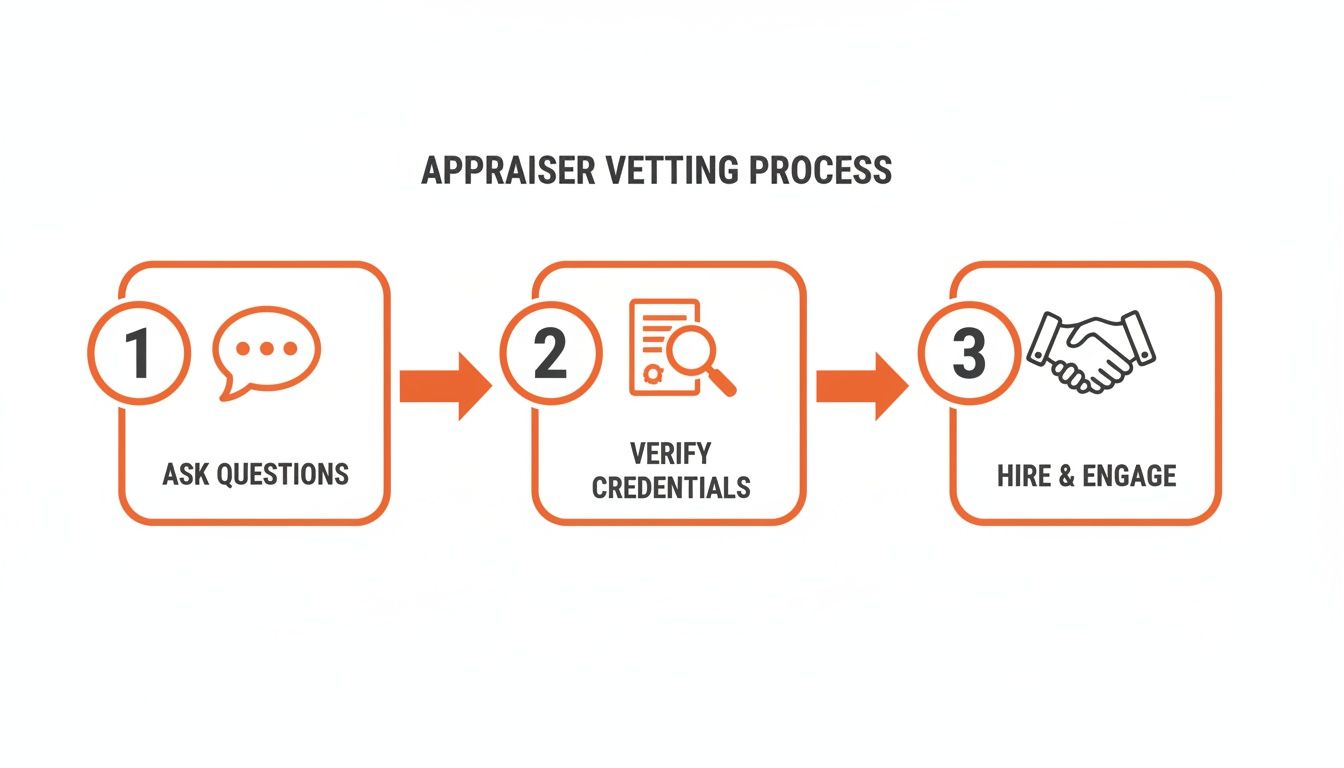

Key Questions to Ask Before Hiring an Appraiser

You’ve done your homework and have a shortlist of potential appraisers. Now for the most important part: the interview. Asking the right questions is how you separate the seasoned pros from the newcomers and find someone who can go toe-to-toe with a billion-dollar insurance carrier. Your search for a “diminished value appraisal near me” isn’t about finding the closest person; it’s about finding the most competent one.

Are Your Reports USPAP Compliant?

This is your first, non-negotiable question. Anything less than a confident “yes” is a dealbreaker.

- A Professional Sounds Like: “Absolutely. Every report we write is fully USPAP compliant. That’s what makes our work defensible and credible under scrutiny from insurers.”

- An Amateur Sounds Like: “What’s that?” or “We have our own internal process.”

An appraiser who ignores USPAP is basically handing the insurance company a pre-written rejection letter for your claim. It’s a massive red flag that screams “unprofessional.”

What Market Data Do You Use to Determine Value?

This question gets to the heart of their entire method. An appraiser is only as good as their data. You want to hear that their entire process is built on real-world, verifiable sales figures from dealer-sold comparables. If they start talking about using simple formulas or relying on basic values from KBB or BlackBook, they aren’t doing the real work required to win your claim.

What Is Your Experience Dealing with My Specific Insurance Company?

Every insurance company has a unique playbook for fighting diminished value claims. A genuinely experienced appraiser knows their tactics—the common lowball arguments, the stall techniques, and the specific software they use, like CCC ONE. CCC ONE is a third-party valuation tool insurers use to generate low initial offers, but it is a starting point for negotiation, not the final authority.

Ask them point-blank: “Have you successfully settled claims with Progressive, State Farm, or Allstate before?” They should be able to confidently talk about that insurer’s specific strategies and explain how their reports are designed to counter them.

Can You Explain the 17c Formula and Why It’s Flawed?

The 17c Formula is a notorious calculation used by many insurance companies to produce a ridiculously low diminished value offer. It’s a simplistic equation that caps the loss and applies arbitrary “modifiers” with no basis in actual market conditions. A true expert will immediately pivot to explaining how their data-driven approach provides a more accurate and legally sound valuation.

For example, real-world data shows vehicles with accident histories often sell for 15-25% less. With over 6 million accidents reported in 2022, the average driver who accepts these lowball offers leaves around $3,500 on the table. Spending $350-$699 on a quality appraisal can easily deliver a 5x to 10x return by proving the actual loss. You can see how these costs stack up on The Auto Mediator’s blog.

Navigating the Appraisal Process From Start to Finish

So, you’ve hired a certified appraiser. Good. You’re ready to stop playing defense against the insurance company’s lowball offer and finally go on the offense. The whole point is to arm you with undeniable proof to get what you’re owed. Let’s walk through what happens next, from gathering your documents to formally submitting your powerful appraisal report.

Assembling Your Evidence

First things first, your appraiser needs ammunition. Your job is to provide all the key documents about your car and the accident. Think of it as handing over the raw materials your expert will use to build an ironclad case on your behalf.

You’ll need to get these items over to them quickly:

- The final insurance estimate of damages.

- The final repair invoice showing work completed.

- Pre-repair and post-repair photos.

- Your vehicle’s VIN, mileage, and options.

Once your appraiser has this package, the real detective work begins. This is where their expertise in crafting a market valuation report makes all the difference.

What Happens Behind the Scenes

This isn’t about plugging a few numbers into a generic online calculator. A real, certified appraiser goes deep, analyzing real-world market data to construct a story that proves your financial loss.

The heart of a legitimate appraisal is its foundation in real, dealer-sold comparables. The report finds vehicles just like yours that sold recently in your local market. This is the direct counterpunch to the theoretical values spit out by insurance software like CCC ONE.

The appraiser then meticulously adjusts the values of those comps based on your car’s specific mileage, options, and pre-accident condition. The final product is a comprehensive report, often 15-30 pages long, that methodically breaks down exactly how much value your vehicle lost.

From Report to Submission

Once you’ve provided your documents, the turnaround is usually just a few business days. You’ll get a detailed PDF, ready to go. The last step is getting this report into the insurance company’s hands. This isn’t just about forwarding an email. It’s a formal notice that you are officially disputing their valuation with certified, evidence-based proof. Our guide on the insurance claim appraisal process digs deeper into how these disputes unfold. Now, armed with an airtight report, you can finally negotiate from a position of strength.

Using Your Appraisal to Negotiate a Fair Settlement

Your certified appraisal report isn’t just an opinion—it’s powerful evidence. But simply having the report is only half the battle. Knowing how to use it effectively is what ultimately secures a fair settlement. This is the moment you stop asking for a handout and start demanding to be made whole, just as your policy requires.

Crafting Your Demand Letter

Your demand letter should be concise, firm, and all business. This isn’t the place for emotional appeals; it’s a professional communication that presents cold, hard facts.

Here’s a simple framework for what your letter needs to include:

- Your Claim Information: Clearly state your name, policy number, and the claim number.

- A Clear Statement of Purpose: “Please find attached my independent, USPAP-compliant appraisal report documenting the inherent diminished value of my vehicle.”

- Reference the Report: “This report, prepared by a certified appraiser, quantifies the market value loss my vehicle has sustained as a direct result of the accident.”

- State Your Demand: “Based on the evidence presented, I am formally demanding payment of $[Appraisal Amount] for my diminished value loss.”

Invoking the Appraisal Clause

Insurance adjusters are trained to push back. They might try to discredit your report, claim your appraiser is biased, or simply ignore your submission altogether. Your most powerful response is to invoke the Appraisal Clause in your auto policy.

The Appraisal Clause is a provision baked into most auto insurance policies that outlines a clear process for resolving valuation disputes. It essentially says that if you and the insurer can’t agree on the value of the loss, you both have the right to hire independent appraisers whose decision can be final and binding.

Invoking the Appraisal Clause isn’t a threat; it’s you exercising a contractual right. It signals to the insurer that you’re serious and ready to escalate the dispute according to the terms of the very policy they wrote.

Standing Firm Against Adjuster Tactics

Armed with a certified appraisal, you are in a position of strength. When the adjuster tries to dismiss your claim, you can respond with confidence.

- If they attack your report: Your response is, “This is a USPAP-compliant report based on verifiable market data. If you have specific, evidence-based objections, please provide them in writing. Otherwise, I will invoke the Appraisal Clause.”

- If they claim they use a standard formula: Your response is, “A formula cannot accurately reflect real-world market losses. This report uses actual sales data, which is a more accurate measure of the loss.”

By presenting factual evidence and understanding your rights, you transform the negotiation from an argument into a data-driven discussion. To better understand the numbers behind your report, check out our guide on how to calculate diminished value.

Frequently Asked Questions (FAQ)

How much does a diminished value appraisal cost?

You can expect a legitimate, USPAP-compliant appraisal from a true specialist to cost between $350 and $699. Think of the fee as an investment. A professionally prepared report has the potential to uncover $1,000 to $5,000+ in lost value that an adjuster would have never offered.

Can I file a claim if the wreck was my fault?

In nearly every state, if you are at fault, you cannot file a first-party diminished value claim with your own insurance company. The major exception is Georgia. However, if another driver hit you, you can almost always file a third-party claim against their insurance company for the value your car has lost.

How long do I have to file a diminished value claim?

Every state has a time limit, called the statute of limitations, for filing property damage claims. This window varies dramatically, from as little as one year in some states to as long as six years in others. It is crucial to move on this as soon as your repairs are done to protect your right to a settlement.

What if the adjuster just rejects my appraisal?

Don’t panic; this is a standard tactic. Your next step is to formally invoke the Appraisal Clause in your auto policy. This clause is your contractual right to resolve a dispute using independent appraisers, forcing the insurer to take your evidence-backed claim seriously. A rock-solid report from a service like SnapClaim is built from the ground up to win this battle.

Don’t leave money on the table. Get your free claim review or order a certified appraisal report today to take control of your insurance settlement.

About AutoAppraisalExpert

AutoAppraisalExpert is a premier provider of independent vehicle appraisal reports and insurance claim consulting. Our mission is to equip vehicle owners with the data-driven evidence required to recover the full financial value of their asset after an accident. Whether navigating a complex Diminished Value claim or disputing a low-ball Total Loss offer, we provide the certified documentation needed to negotiate with insurance companies from a position of strength.

With a national reach and deep industry expertise, we have helped thousands of policyholders identify errors in carrier valuation reports (like CCC) and invoke the Appraisal Clause to secure fair settlements. We pride ourselves on transparency, speed, and reports that stand up to the toughest insurer scrutiny.

Why Trust This Guide

This guide was written and verified by the AutoAppraisalExpert technical team. Our appraisers specialize in total loss disputes and diminished value forensics. We stay current on state insurance regulations, court-accepted valuation practices, and evolving market trends to ensure our readers—and our clients—always have the most accurate information available.

Ready to see what your car is really worth? Get your free estimate today.