Meta Title: Dispute Total Loss Offer With an Appraiser Today

Meta Description: Dispute total loss offer with an appraiser. Learn the process, use the Appraisal Clause, and fight for a fair settlement today.

Your insurer sent a number. It feels low. You compare it to what similar vehicles sell for, and the offer still does not make sense.

If you need to dispute total loss offer numbers or challenge a weak repair-related valuation, you are exactly the kind of owner who should understand what auto insurance appraisers do. The insurer’s first number is not the final word. In many claims, it is only the starting point for a valuation fight.

Your Guide to Auto Insurance Appraisers and Fair Settlements

A frustrated owner usually calls after the same moment. The car is gone, or repaired but stigmatized by an accident history, and the carrier’s settlement lands with a thud. The report looks official. The offer does not look fair.

That disconnect is common because the company valuing your loss is also the company paying it. An auto insurance appraiser hired independently does something different. The job is to measure the vehicle’s true loss using market evidence, not to close a file cheaply.

The financial implications are more substantial than many drivers realize. The average collision insurance claim now exceeds $4,300, and rising repair costs tied to technology such as ADAS sensors are pushing more vehicles into total-loss territory, according to Appraisal Engine’s report on vehicle appraisal trends. That is one reason valuation disputes are becoming more serious, not less.

What an auto insurance appraiser does

An appraiser for the policyholder examines the claim from the value side, not just the damage side. That can include:

- Actual Cash Value analysis: Actual Cash Value, or ACV, means the vehicle’s fair market value immediately before the loss.

- Diminished value analysis: This measures the market loss that remains after repairs because buyers pay less for a vehicle with accident history.

- Market valuation report review: This means auditing the insurer’s valuation document for weak comparables, bad option adjustments, or unsupported condition deductions.

- Appraisal Clause support: This helps the owner use the policy’s dispute mechanism when negotiations stall.

Practical takeaway: If the insurer’s number feels disconnected from real local listings, dealer pricing, or your vehicle’s equipment and condition, that is not something to shrug off. It is a reason to get the valuation reviewed.

Good auto insurance appraisers are not magicians. They are evidence builders. They gather comparable sales, verify trim and options, examine condition, and write a report that can survive scrutiny from an adjuster, supervisor, attorney, or umpire.

Independent Appraiser vs The Insurer’s Adjuster

The fastest way to understand this process is to understand the two people on opposite sides of it.

An insurance adjuster handles the claim for the carrier. An independent auto appraiser evaluates the disputed value from outside the carrier’s system. Both may know vehicles. Their roles are not the same.

Independent Appraiser vs. Insurer’s Adjuster At a Glance

| Factor | Independent Auto Appraiser | Insurance Company Adjuster |

|---|---|---|

| Who they work for | The vehicle owner or claimant | The insurance company |

| Primary objective | Develop a supportable opinion of value | Resolve the claim within company procedures |

| How value is built | Reviews real market data, vehicle specifics, condition, options, and comparable sales | Often relies heavily on internal valuation workflows and vendor reports |

| View of software | Treats CCC or similar tools as a starting point, not a final authority | May treat software outputs as the default framework |

| Dispute role | Supports negotiation and Appraisal Clause action | Defends or explains the carrier’s position |

| Report focus | Market-backed valuation built for challenge and review | Claim file documentation for settlement handling |

Why the numbers often differ

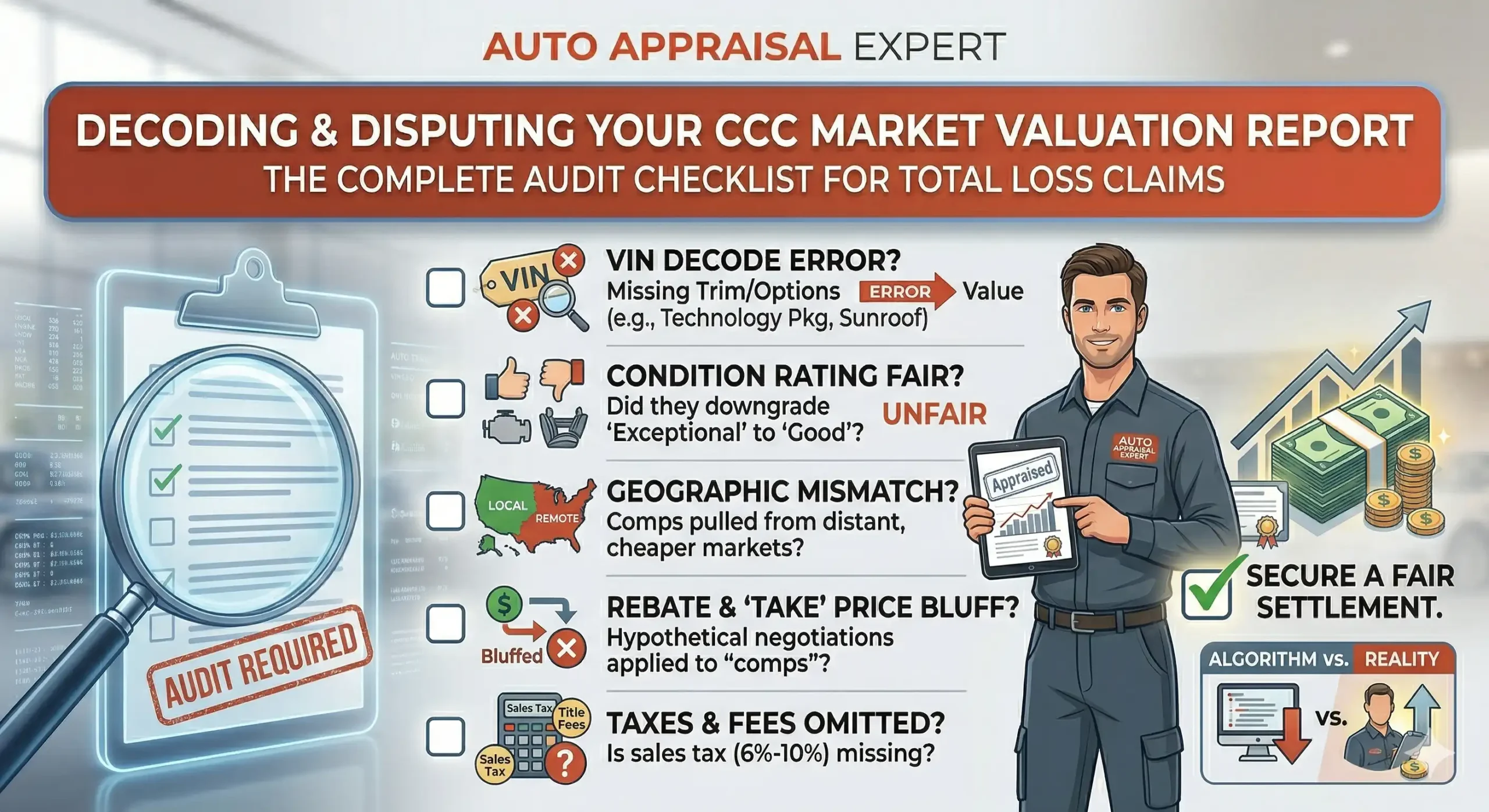

The insurer’s adjuster is not necessarily dishonest. But the workflow is built around consistency, speed, and cost control. That system can miss details that matter to value, especially when the software used to generate a market valuation report relies on comparables that are merely convenient instead of comparable.

A proper independent appraisal usually checks for issues like these:

- Wrong trim or package level: A vehicle with premium options can be grouped with lower-equipped units.

- Condition deductions that do not fit the evidence: The report may assume wear or prior issues that are not documented.

- Bad geographic comparisons: Listings too far outside the true local market can skew results.

- Weak comparable choices: Vehicles with different drivetrains, histories, mileages, or option sets can drag value down.

The conflict is structural

Owners often think the argument is about one number. It is usually about methodology. The carrier asks, “What did our system produce?” The independent appraiser asks, “What would this vehicle command in the relevant market?”

That difference matters even more with modern vehicles. Electronic options, ADAS hardware, camera systems, and trim-specific equipment can materially change value and repair consequences. If those details are glossed over, the owner absorbs the loss.

Expert tip: Ask the adjuster to explain each comparable used in the valuation. If they cannot clearly justify why each comp matches your year, make, model, trim, mileage, options, and local market, the report deserves scrutiny.

What works and what does not

What works:

- Calm written objections

- A point-by-point critique of the insurer’s valuation

- Real dealer-sold or active market comparables

- A certified appraisal report built on recognized methodology

What does not:

- Telling the adjuster the offer “feels unfair”

- Sending random screenshots with no analysis

- Arguing from emotion instead of market evidence

- Assuming the software result is untouchable

If you are going to fight a low offer, fight on evidence. That is where auto insurance appraisers are most effective.

Key Appraisal Services Total Loss and Diminished Value

Most claim disputes fall into two buckets. The vehicle is a total loss, or the vehicle was repaired and now carries a market stigma.

Those are different claims. They require different valuation logic.

Total loss appraisals

In a total-loss claim, the core issue is Actual Cash Value. Again, ACV means the vehicle’s fair market value just before the accident. The insurer may present that number through a CCC-style valuation package or another software-driven report.

That report is not sacred. It is an estimate built from inputs, assumptions, and comparable choices. If those choices are poor, the settlement can come in low.

A total-loss appraisal typically focuses on:

- Vehicle identification: Exact year, make, model, trim, drivetrain, packages, and options

- Condition verification: Prior condition matters, but deductions must be supportable

- Comparable market research: The strongest comps are real listings from the relevant market

- Report audit: The appraiser checks whether the insurer’s adjustments are reasonable

If you want a consumer-friendly explanation of value concepts, review SnapClaim’s fair market value resource. It helps frame what the insurer should be trying to measure.

Diminished value appraisals

A repaired car can still be worth less than an identical car with no accident history. That is diminished value, or DV.

The easiest analogy is real estate. Two identical homes on the same street do not sell for the same price if one had major flood damage in its history, even if repaired well. Vehicles work the same way. Buyers discount accident history.

That issue is more serious on newer, technology-heavy vehicles. Wreck Check Atlanta notes that IIHS 2025 data shows ADAS-equipped vehicles can lose 15-30% more value post-collision, with recalibration costs of $2,000-$5,000 often omitted in standard insurer reports. That matters because post-repair value is not just about visible bodywork. It is also about complex systems, repair stigma, and buyer confidence.

Diminished value vs. total loss

Here is the clean distinction:

- Total loss: The fight is over what the vehicle was worth before the loss.

- Diminished value: The fight is over how much value the vehicle lost after repairs.

- Car appraisal for insurance claim: This is the broader process that can apply to either situation, depending on the claim type.

For a deeper breakdown of post-repair loss, see this guide on diminished value after an accident.

Key point: Owners often mix these claims together. Do not. A total-loss valuation and a diminished-value appraisal answer different questions, use different evidence, and should be argued differently.

Where people go wrong

A common mistake is focusing only on repair invoices. Repair bills matter, but they do not fully answer a market-value dispute. A vehicle can be repaired correctly and still suffer a measurable resale penalty because history reports and buyer perception changed.

Another mistake is accepting formula-only thinking. Some insurers lean on simplified methods. A real appraisal should test those assumptions against the market that buyers and dealers operate in.

If your claim involves either a total-loss dispute or a repaired vehicle with accident stigma, auto insurance appraisers fill the gap between a generic software output and the vehicle’s real-world value.

When You Should Hire An Independent Auto Appraiser

Not every claim needs one. Some do. The problem is that owners usually wait too long.

The right time is when the dispute turns from a simple question into a valuation problem. Once that happens, you need evidence, not more phone calls.

Red flags that justify an appraisal

- Your offer does not match public market checks: If your research on Kelley Blue Book and actual dealer listings points one way while the carrier points another, the valuation deserves review.

- The insurer’s comparables look wrong: Different trim, wrong mileage range, weak condition assumptions, or vehicles from questionable markets are all warning signs.

- Your vehicle is unusual: Classic, custom, enthusiast, specialty, or highly optioned vehicles are easier for generic systems to undervalue.

- You are dealing with diminished value: These claims often fail when owners submit only repair bills and not a true market analysis.

- The report feels formula-driven: If the adjuster can only repeat what the software says, rather than explain why the comparables are sound, get a second opinion.

Why the timing matters

The strongest disputes are organized early. You want the policy, insurer valuation report, photos, repair estimate or final invoice, and your own vehicle documentation lined up before positions harden.

Owners also underestimate the influence a formal report can add. According to Total Loss Appraisals’ appraisal clause overview, invoking the Appraisal Clause with a certified appraisal report has led to valuation increases of 20-50%, with an average recovery of $3,495 for policyholders disputing the insurer’s initial offer.

That does not mean every appraisal produces the same result. It does mean the right report can materially change the conversation.

What to gather before you hire anyone

Bring order to the file first:

- The carrier’s valuation packet

- Photos of the vehicle before and after loss, if available

- Window sticker, build sheet, or option list

- Maintenance records and proof of upgrades

- Repair documents

- Any dealer quotes or local comparable listings you found

Practical tip: If your insurer’s report has pages of adjustments but no clear explanation in plain English, ask for a supervisor review and an independent appraisal at the same time. Do not wait for the same flawed report to be reissued with a different cover email.

Starting the process

A good intake process should be simple. The owner provides claim documents, vehicle details, and the insurer’s valuation materials. The appraiser then decides whether the issue is a total-loss ACV dispute, a diminished-value claim, or both.

If you want a straightforward place to understand claim support options, SnapClaim’s main site is a useful starting point.

The Independent Appraisal Process and Methodology

A serious appraisal is not guesswork. It is a repeatable process.

The strongest reports are USPAP-compliant. USPAP stands for Uniform Standards of Professional Appraisal Practice, which is the recognized framework for developing and reporting credible appraisal opinions. That matters because a report built to professional standards carries more weight when a carrier, attorney, or umpire reviews it.

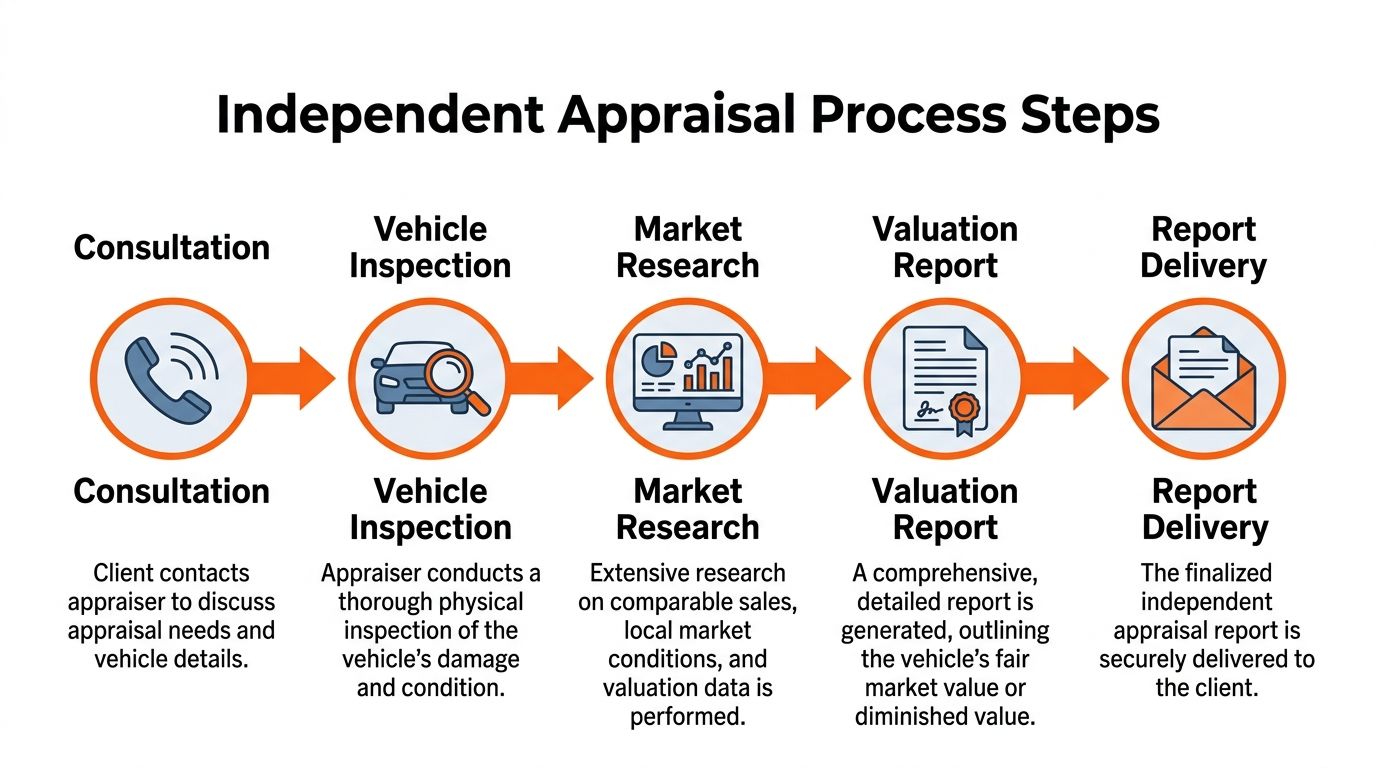

What the workflow looks like

Step one through step three

File review

The appraiser collects the insurer’s documents, photos, VIN details, option information, repair records, and any prior valuation material. The goal is to identify what the carrier assumed and whether those assumptions hold up.Inspection and condition analysis

Depending on the claim, this may involve reviewing pre-loss condition, post-repair status, or both. Condition affects value, but condition adjustments must be tied to actual evidence.Comparable market research

Many disputes are won or lost at this stage. Certified appraisers use tools such as V-CAR to integrate real-time market data from more than 1,000 regional listings, cross-referencing that data with NAAA condition codes 1-5 to support true market value, according to Chesapeake Auto Appraisers.

Step four and step five

Valuation analysis

The appraiser compares the insurer’s numbers against stronger market evidence. That often means checking trim accuracy, mileage treatment, options, condition, and whether the comparable vehicles are comparable.Report generation

The finished report should explain the logic, not just announce a number. It needs to show how the valuation was reached, why certain comps were used or rejected, and where the insurer’s market valuation report may have gone off track.

For a focused look at how this kind of report is used in claims, see this guide on insurance claim appraisal.

What separates a credible report from a weak one

A weak report is mostly conclusion. A strong report is mostly support.

Look for these features:

- Clear identification of the exact vehicle

- Comparable selection explained in plain English

- Condition and options supported by records or photos

- Discussion of errors in the insurer’s market valuation report

- Methodology that can be defended if challenged

The software myth

Owners often hear that CCC ONE or another valuation platform already determined the number. That framing is misleading.

Software is a tool. It can organize data quickly. It can also carry forward bad assumptions quickly. If a report starts with the wrong trim, wrong package, wrong condition, or poor comps, the output may look polished while still being wrong.

Expert advice: Ask whether the insurer’s report is based on dealer-sold comparables, live market listings, or adjusted substitutes. The closer the evidence is to real local market activity, the stronger your position.

How to Use Your Report to Dispute a Settlement Offer

Once you have the report, the job shifts from valuation to strategy. Many owners lose momentum here. They get a strong appraisal, email it over, and hope the adjuster suddenly agrees.

Use a process instead.

Start with a written challenge

Send a short, professional letter or email that does three things:

- Identifies the dispute clearly: State that you dispute the valuation amount, not coverage generally.

- Attaches the appraisal report: Refer to the report as your evidence of fair market value or diminished value.

- Requests a revised settlement review: Ask for a written response.

Do not send a rant. Send a record.

Name the specific problems in the carrier’s report

Keep the focus on evidence. Typical objections include:

- Wrong or weak comparable vehicles

- Unsupported condition deductions

- Missing options or trim differences

- Failure to account for relevant local market conditions

- In a repaired vehicle claim, failure to account for stigma or technology-related post-collision loss

This guide on total loss settlement negotiation gives a useful framework for organizing that pushback.

Use the Appraisal Clause if the carrier holds its ground

The Appraisal Clause is a policy provision that allows a value dispute to be decided through appraisers rather than left entirely to ordinary adjuster negotiation. In plain terms, each side selects an appraiser. If the appraisers cannot agree, they select an umpire to resolve the difference.

This is often the cleanest way to move a deadlocked valuation dispute forward.

A practical approach looks like this:

Review your policy language carefully

Look for timing requirements, notice requirements, and any wording about selecting appraisers or an umpire.Give formal notice

State in writing that you are invoking the Appraisal Clause under the policy.Identify your appraiser

Include the appraiser’s name and contact information if your policy requires it.Preserve your paper trail

Save every letter, email, report, and response.

Why the clause matters

In over 90 Maryland and Virginia court cases, independent audits that invoked the Appraisal Clause resulted in an average settlement increase of 15% by successfully challenging ACV figures in CCC Market Valuation Reports, according to Auto Appraisal Network.

That does not guarantee your outcome. It does show that a structured appraisal dispute can work when supported by a defensible report.

Check your state’s rules

Appraisal rights and enforcement can vary by state. Before you invoke the clause, review your state’s insurance guidance. As one example, the Texas Department of Insurance is a useful reference point for state-level consumer information.

Important: The Appraisal Clause usually resolves the amount of loss. It does not necessarily resolve every other coverage dispute. Keep your argument focused on value unless counsel advises otherwise.

What works best in practice

The best settlement disputes share a pattern:

- The owner stays professional

- The report is specific

- The objections are tied to market facts

- The policy language is used properly

- Deadlines are respected

What fails is vagueness. If you want to dispute total loss offer numbers effectively, act like you are building a case file, not venting frustration.

Frequently Asked Questions About Auto Insurance Appraisers

How long does an auto insurance appraisal take

It depends on the file quality and the claim type. A straightforward total-loss review can move faster than a complex diminished-value case involving heavy repair documentation, technology issues, or disputed condition. Delays usually come from missing records, not the valuation work itself.

What if the two appraisers cannot agree

That is where the umpire comes in under the Appraisal Clause process. The umpire is the neutral third party who resolves the disagreement when the appraisers remain apart on value. Your policy language controls the exact procedure, so read it carefully before invoking the clause.

Do I have to pay for the insurance company’s appraiser

Policy language often explains how costs are handled. In many appraisal processes, each side pays its own appraiser and shares the umpire cost, but you should confirm that in your own policy before moving forward. Do not assume. Verify.

Is a market valuation report from CCC final

No. It is evidence, not a verdict. A market valuation report is only as reliable as the comparables, condition adjustments, option coding, and market assumptions behind it. That is why owners hire an independent auto appraiser to review and challenge it.

Can I use an appraiser for a repaired car, not just a total loss

Yes. That is the core use case for diminished value vs. total loss disputes. If the car was repaired but now carries an accident history that hurts resale value, a diminished-value appraisal may provide the evidence needed to negotiate.

Conclusion

If your insurance offer feels low, do not assume the file is closed. Auto insurance appraisers exist because valuation disputes are real, common, and often fixable with better evidence.

The most important point is simple. You do not need to win a shouting match with an adjuster. You need a credible, market-backed report, a clean written challenge, and the discipline to use your policy rights properly. That is how owners dispute total loss offer numbers effectively. It is also how they challenge weak diminished-value positions after repairs.

Don’t leave money on the table. Get your free claim review or order a certified appraisal report today to take control of your insurance settlement.

About AutoAppraisalExpert

AutoAppraisalExpert is a premier provider of independent vehicle appraisal reports and insurance claim consulting. Our mission is to equip vehicle owners with the data-driven evidence required to recover the full financial value of their asset after an accident. Whether navigating a complex Diminished Value claim or disputing a low-ball Total Loss offer, we provide the certified documentation needed to negotiate with insurance companies from a position of strength.

With a national reach and deep industry expertise, we have helped thousands of policyholders identify errors in carrier valuation reports (like CCC) and invoke the Appraisal Clause to secure fair settlements. We pride ourselves on transparency, speed, and reports that stand up to the toughest insurer scrutiny.

Why Trust This Guide

This guide was written and verified by the AutoAppraisalExpert technical team. Our appraisers specialize in total loss disputes and diminished value forensics. We stay current on state insurance regulations, court-accepted valuation practices, and evolving market trends to ensure our readers, and our clients, always have the most accurate information available.

Ready to see what your car is really worth? Get your free estimate today.

If you are ready to challenge a low insurance valuation, request a free review from Auto Appraisal Expert. A certified appraisal report can give you the evidence needed to negotiate from a stronger position.