Meta Title: Classic Car Inspectors Guide. Protect Your Claim

Meta Description: Need classic car inspectors? Learn how to hire the right expert and use the report to challenge a low offer. Start your claim review.

If you’re buying, insuring, or fighting over the value of an older collectible vehicle, classic car inspectors can save you from an expensive mistake.

The problem is simple. Most owners don’t need an inspection until circumstances are critical. A purchase is moving fast, an insurer has issued a low offer, or a repaired classic now carries an accident history that buyers won’t ignore. In those moments, a basic shop opinion isn’t enough. You need documentation that holds up under scrutiny.

The Hidden Risks Why a Regular Mechanic Is Not Enough

A claim lands on my desk after a classic is totaled. The owner has a letter from his local shop saying the car was “very clean” and “mechanically sound.” The insurer still values it like an ordinary old used car. That happens because a repair shop opinion and a classic inspection serve different purposes.

A regular mechanic is trained to find faults that affect safety, drivability, and repair cost. A classic car inspector looks at those items too, but its core function is broader. The inspector documents authenticity, prior damage, restoration quality, correctness of parts, and the condition details that change market value. Those points matter in a purchase. They matter even more when an insurer is deciding whether your car was a high-quality survivor, a properly restored example, or just an old vehicle with a paint job.

I have seen claims stall because the owner’s mechanic focused on compression numbers and brake function while missing replaced VIN tags, incorrect trim, reproduction stampings, and signs of old collision repair under fresh undercoating. A carrier will gladly use those gaps against you. If the file does not show why the car was worth more, the first offer usually reflects that.

Roadworthy and properly valued are different standards

A classic can run well and still be worth far less than the owner believes. It can also run well and be worth far more than the insurer admits.

The difference often sits in details a general shop does not document with appraisal discipline:

- Non-original parts that reduce collectability even if they work properly

- Paint and bodywork that conceal filler, prior rust repair, or poor panel replacement

- Undercoating and fresh finishes used to hide corrosion, seams, or rough welding

- Trim, castings, tags, and date-coded components that do not match the car’s claimed identity

- Restoration shortcuts that present well online but lower market value under close inspection

That last point matters in disputes. Insurers often treat a shiny older restoration as equal to a properly documented one. They are not equal in the collector market.

Where general inspections fall short

Classic inspection work rewards specialized pattern recognition. Good inspectors know where a certain model rusts first, which welds should look factory, what panel gaps are normal for the era, and which reproduction parts are accepted by the market versus discounted. They also photograph the evidence in a way that holds up later, when a claim adjuster, appraiser, or attorney reviews the file months after the loss.

A specialist inspection usually covers:

- Provenance and documentation review, including ownership history, restoration records, and supporting paperwork

- Body and structure analysis for replaced panels, corrosion repair, accident damage, and fit issues

- Undercarriage inspection for patching, scaling, poor metal work, and structural weakness

- Mechanical condition with value context, not just a list of repairs needed

- Interior, trim, and originality review to separate honest age from incorrect replacement

- Photo-backed findings that can support valuation work, diminished value analysis, or a total loss dispute

Why this matters in an insurance dispute

Insurance companies start with internal valuation systems and comparable sales data. Those tools are only as good as the inputs. If the file ignores rare options, correct driveline components, high-grade restoration work, or unusual originality, the number comes in low.

That creates two problems. In a total loss case, the carrier may understate actual cash value because the inspection record does not show what the car really was before the damage. In a repaired-vehicle case, the owner may struggle to prove diminished value because there is no solid pre-loss documentation of condition, authenticity, and market standing.

The right inspector gives you evidence, not opinions. That is the difference between arguing with an insurer and presenting a file they have to answer.

Where to Find Vetted Classic Car Inspectors

Many individuals start with a search engine. That’s fine for a first pass, but it’s not how you find the best classic car inspectors.

The strongest leads usually come from communities and professionals who already know the weak points of a specific make, body style, or era.

Start with marque-specific communities

If you own or want a model with a dedicated following, start there.

Marque clubs and model-specific communities often know which inspectors understand the details that affect value. A Corvette owner needs different expertise than a vintage Porsche or a muscle-car buyer chasing numbers-matching originality.

Look for referrals from:

- Owners’ clubs with active technical members

- Regional collector car groups that see local inventory repeatedly

- Restoration specialists who know who documents cars carefully

- Auction participants who regularly buy at the upper end of the market

Ask a narrow question, not a broad one. Don’t ask, “Know a good inspector?” Ask, “Who catches hidden body work on early cars from this platform?” The answers get better fast.

Use professional directories carefully

Appraisal and inspection directories can help, but don’t stop there.

A listing tells you someone wants business. It doesn’t prove they know your exact vehicle or that their report will be useful in a claim. For insurance disputes, credentials matter because the document may need to support negotiations, attorney review, or an appraisal clause demand.

Appraisal Clause is a policy provision that often lets you hire your own appraiser when you and the insurer disagree on value. That right can be powerful, but only if your supporting evidence is solid.

When you review candidates, look for:

| What to check | Why it matters |

|---|---|

| Experience with your make and era | Classic defects are model-specific |

| Detailed photo reports | Insurers and buyers respond to visible proof |

| Documentation review | Titles, VINs, restoration records, and history affect value |

| Insurance dispute familiarity | A claim-ready report is different from a casual inspection |

| Independence | Seller-connected inspectors create obvious risk |

Be cautious with seller-recommended inspectors

A seller may offer an “easy” inspector. Sometimes that’s harmless. Sometimes it isn’t.

If the inspector depends on dealer, auction, or broker referrals for repeat business, ask harder questions. You want an inspector who can say uncomfortable things in writing.

That doesn’t mean auction-connected experts are unusable. It means you should confirm whether they’re acting as a neutral evaluator or as part of a transaction pipeline.

The best inspector for a dispute is usually the one who’s comfortable documenting defects that make a sale harder.

Add digital provenance when the stakes justify it

Physical inspection still comes first. But for higher-value collectibles, digital history tools are becoming more relevant.

According to Auto Appraisal’s classic car inspection discussion, classic car thefts were up 12% in 2025 and Hemmings’ blockchain pilots were tracking 5,000+ vehicle histories, reflecting a growing push toward immutable provenance records for originality and fair market value disputes.

That doesn’t replace a hands-on inspection. It supplements it.

Use digital provenance tools to help answer questions such as:

- Was this component history documented earlier

- Did the vehicle’s stated configuration change over time

- Are restoration claims supported by traceable records

- Does the ownership history align with the sales story

For a high-value claim, that extra layer can matter. A physical inspector may identify a concern. A digital record can help prove whether it’s a harmless replacement, a major authenticity issue, or a fraud problem that affects fair market value.

The Vetting Process Key Questions for Any Inspector

The call usually happens after the bad news. The insurer has undervalued the car, called repair work “cosmetic,” or ignored what the loss did to originality. At that point, hiring the wrong inspector costs money twice. First in the fee, then in a report that cannot hold up under scrutiny.

A serious inspector should be willing to discuss process before scheduling the visit. If that conversation feels slippery, the report often is too.

Ask about method before price

Fee matters. Method matters more.

For insurance disputes, I want to hear how the inspector handles three jobs separately: condition documentation, authenticity review, and valuation support. Plenty of people can walk around a classic with a flashlight. Fewer can produce a report that helps prove pre-loss condition, supports a total loss position, or explains diminished value after repair.

Ask these questions directly:

- What do you review before seeing the car? Strong inspectors ask for photos, VIN data, restoration records, prior appraisals, repair invoices, and any claim paperwork already in play.

- How long are you typically on site? A rushed visit usually means missed underbody issues, incomplete photo documentation, and weak notes.

- Do you inspect the underbody, chassis, and hidden rust areas closely? If access is limited, ask how they document that limitation in the report.

- Do you pair photographs with written findings? Photos without conclusions are just a gallery. Conclusions without photos are easy for an insurer to dismiss.

- Have you written reports for total loss or diminished value disputes involving classics? That answer should include examples of the type of documentation they provide, not a generic “yes.”

One more question separates experienced inspectors from sales-oriented ones.

Ask what they cannot confirm during a field inspection.

A good inspector will tell you where lab testing, paint-depth readings, teardown, marque specialist input, or title research may still be needed. That kind of restraint makes a report more credible, not less.

Test for model fluency

Classic expertise is rarely broad and deep at the same time. A person may know postwar American cars well and still miss known trouble spots on an air-cooled Porsche or a chrome-bumper British roadster.

Give them the exact year, make, model, and any claimed restoration level. Then listen for specifics. You want to hear about problem areas, authenticity markers, and market-sensitive details that affect claim value.

Better answers usually cover:

- known rust points and water traps

- trim, casting, or tag details that are often incorrect after restoration

- common filler, patch, or repaint shortcuts

- driveline or suspension weaknesses specific to that model

- originality items that materially affect insurer negotiations and resale value

If the answer sounds like a general speech about “old cars,” keep looking.

Ask what they measure and how they document it

Observation matters. Measured findings carry more weight in a dispute.

A qualified inspector should be able to explain what tools they use, what conditions limit reliable readings, and how those findings appear in the report. That may include paint meter readings, compression results when appropriate, chassis and panel alignment observations, date-code verification, corrosion checks, and detailed photo mapping of damage or prior repairs.

What matters is not a rehearsed list of tools. What matters is whether the inspector can connect each finding to a value impact. For an insurance claim, “prior repair noted” is weak. “Prior quarter-panel replacement with finish variation, seam inconsistency, and non-original weld presentation affecting market desirability” is useful.

That distinction is where many reports fail.

Ask credentials in a way that matters

Credentials help when an insurer challenges the report, but initials alone do not make an inspector persuasive. Ask how they apply standards, not just what certificates they hold.

Use this set of questions:

- Are you USPAP-compliant when valuation opinions are included?

- What appraisal or inspection training do you hold for collector vehicles?

- Have your reports been used in appraisal clause cases, subrogation matters, or diminished value disputes?

- Do you separate factual inspection findings from valuation conclusions?

- Will your report state assumptions, limits, and unavailable evidence clearly?

That last point matters more than many owners realize. Insurers often attack a report at its edges. They look for missing assumptions, unclear sourcing, and opinion stated as fact.

If you’re weighing fees, compare the final product, not just the invoice. A cheaper report that cannot support a claim is expensive in practice. For a realistic sense of pricing on related valuation work, review this guide to auto appraisal cost.

Use a quick screen before you hire

| Question | Strong answer | Weak answer |

|---|---|---|

| Do you know this model? | Identifies specific fault areas, originality markers, and claim-sensitive details | Gives broad comments about classic cars in general |

| How do you inspect for prior repair or rust? | Explains access points, concealment areas, documentation limits, and photo support | Says they “look it over” |

| What will the report include? | Photo set, written findings, records review, condition analysis, and valuation relevance | Promises a short summary |

| Can this report help with an insurance dispute? | Explains how findings are tied to loss, market effect, and documentation standards | Avoids commitment or stays vague |

A capable inspector will not be bothered by careful questions. In claim work, informed clients are easier to defend.

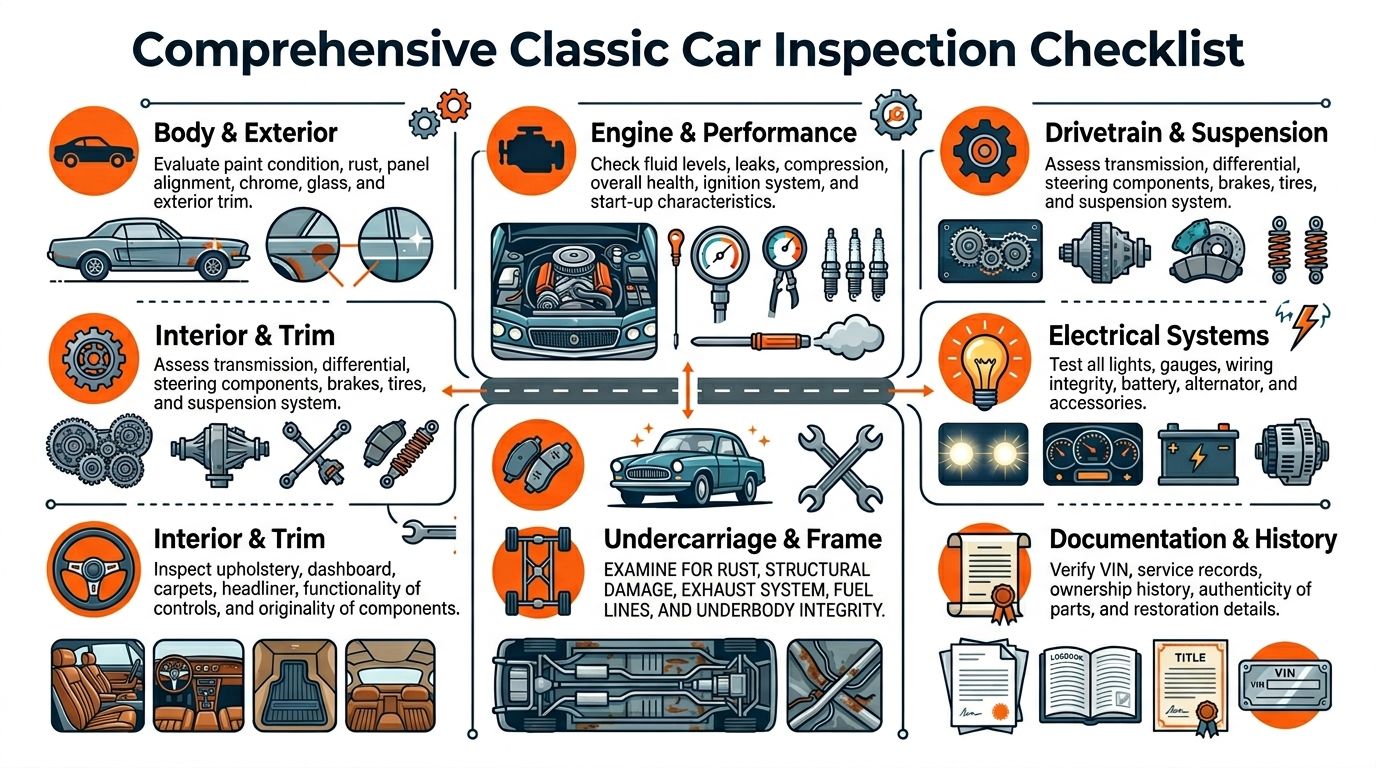

Deconstructing the Inspection A Detailed Checklist

A seller says the car is “older restoration, very solid,” and the photos look convincing. Then an insurer later argues that the quarter panel work was old damage, the underbody corrosion was pre-existing, and the replacement trim does not affect value. A useful inspection closes those gaps before a dispute starts.

For classic and collector vehicles, the job is not limited to checking whether the car runs and drives. The inspector needs to document condition in a way that holds up if you later need to prove pre-loss condition, challenge a total loss valuation, or support a diminished value claim. If you want the broader context, this guide on what a car appraisal covers helps explain how inspection findings feed into value opinions.

A good inspection follows a repeatable process and leaves a paper trail. Casual language such as “nice car” or “driver quality” is not enough. The report should identify what was seen, what was tested, what could not be verified, and what each finding means for condition, originality, and claim exposure.

Body and exterior

Bodywork tells the truth faster than the seller usually does.

The inspection should cover paint consistency, overspray, panel fit, chrome quality, trim attachment, weatherstrip edges, glass condition, and signs of prior repair. On a classic car, the issue is rarely just appearance. Old collision work, filler, poor metal finishing, and incorrect replacement panels can change both market value and how an insurer views later damage.

Useful body notes often include:

- Reflections that wave or distort, which can indicate filler or uneven blocking

- Panel gaps that vary side to side, which may point to repair history or poor reassembly

- Paint build-up at moldings or seals, a common clue that a repaint was done with shortcuts

- Glass date codes or markings that do not match the car’s story, especially on cars represented as highly original

Undercarriage and frame

This area separates a surface-level inspection from a claim-ready one.

The report should address frame rails, floor pans, rockers, torque boxes, suspension pickup points, trunk floors, patch sections, and corrosion hidden by fresh coating or underseal. Good inspectors also photograph drain areas, seams, and weld patterns. Those details matter later because insurers often classify rust, prior repairs, and long-term deterioration as unrelated to a current loss.

Fresh coating on old metal proves little.

Interior and trim

Interior condition affects value more than many owners expect, especially on cars where originality drives the market.

The report should record upholstery materials, seat pattern correctness, dash condition, instrument function, headliner fit, carpet moisture, trunk trim, and wear consistent with the stated mileage or restoration age. A cabin can present well in photos and still lose ground in a valuation dispute if the materials, colors, hardware, or stitching are incorrect for the model year.

Trim also matters in insurance work. Broken original pieces, discontinued switchgear, and rare trim components can be expensive to source and difficult to value if they were never documented before the loss.

Engine and drivetrain

Mechanical review needs two tracks. One is operation. The other is identity.

The inspector should note cold start behavior, idle quality, smoke, leaks, fluid condition where visible, transmission engagement, clutch take-up, braking response, steering play, differential noise, and exhaust condition. On collector cars, the report should also record visible casting numbers, stampings, tags, and other identifiers when accessible without disassembly.

That second part is where many ordinary inspections fall short. A replacement engine may still run well, but it can change value, claim strategy, and settlement position. I have seen insurers pay close attention to originality only after a loss, when the owner no longer has good pre-loss documentation.

Electrical systems and accessories

Older wiring can be tidy, serviceable, dangerous, or all three.

Inspectors should test lights, gauges, charging function, wipers, blower motors, horn, radio, power accessories, and any aftermarket additions. The report should also comment on wiring quality, fuse protection, splice methods, and whether modifications were done cleanly or improvised. Poor electrical work affects safety, restoration cost, and insurer arguments about pre-existing condition.

Documentation and history

The car and the paperwork should support each other.

A proper report should address:

- VIN, serial, or chassis number verification

- Title consistency

- Service records

- Restoration invoices and photo records

- Ownership history

- Evidence for originality or rarity claims

Do not accept repeated seller language as documentation. If a car is described as matching-numbers, fully restored, or one of a limited build, the inspector should state what was verified, what source was used, and what remains unconfirmed. That distinction becomes important when an insurance company tries to reduce a payout by treating documented features as unsupported claims.

Reading the Report and Spotting Critical Red Flags

Once the report arrives, many owners make the next mistake. They skim for a bottom-line opinion and ignore the evidence behind it.

That approach misses both vehicle problems and report problems.

Professional classic car inspections generally have a notable cost, and specialists on rare vehicles can run higher. The reason that fee makes sense is straightforward. A report in that range can uncover hidden rust or poor restoration work that may involve significant repair costs, making the inspection a fraction of the potential loss and, as one source puts it, “good insurance” against scams and undisclosed damage in online transactions (DFW Auto Appraisal on classic car inspection).

What a usable report should contain

A report worth paying for usually has four traits.

- Specific findings rather than broad impressions

- Clear photos of the exact issue being described

- Documentation notes that separate verified facts from seller claims

- A conclusion tied to condition and value relevance

If the inspector says there is corrosion, the photos should show where. If they say originality is questionable, they should explain what doesn’t match. If they could not verify a claim, the report should say that plainly.

For a broader explanation of how appraisal documents work, this guide on what is a car appraisal is a useful companion.

Vehicle red flags that deserve real weight

Not every defect is a deal-breaker. Some are routine age issues. Some change the value picture completely.

Pay close attention to findings involving:

| Red flag | Why it matters |

|---|---|

| Structural rust | Repair cost and safety concerns can become severe |

| Frame or underbody repairs | Prior damage may be larger than disclosed |

| Non-matching or questionable driveline identity | Collectability can drop quickly |

| Poor restoration quality | Cosmetic appeal may hide expensive corrective work |

| Missing or weak documentation | Value claims become harder to support |

Report red flags that owners overlook

Sometimes the car isn’t the biggest issue. The report is.

Watch for:

- Vague language such as “appears fine for age” with no detail

- Few photos or photos that don’t match the written concerns

- No distinction between confirmed facts and unverified seller statements

- No follow-up availability when you ask reasonable questions

- No discussion of limitations where verification was not possible

If an inspector can’t explain their own report after delivery, don’t expect an adjuster or attorney to trust it.

The strongest reports let you act: You can renegotiate the purchase, walk away, support a fair market value challenge, or hand the file to an independent auto appraiser without asking them to rebuild the factual record from scratch.

How to Use Inspection Findings in Insurance Claims

Many owners overlook this point, leaving money on the table. They treat the inspection as a buying tool only, then fail to use the same evidence when the insurer undervalues the claim.

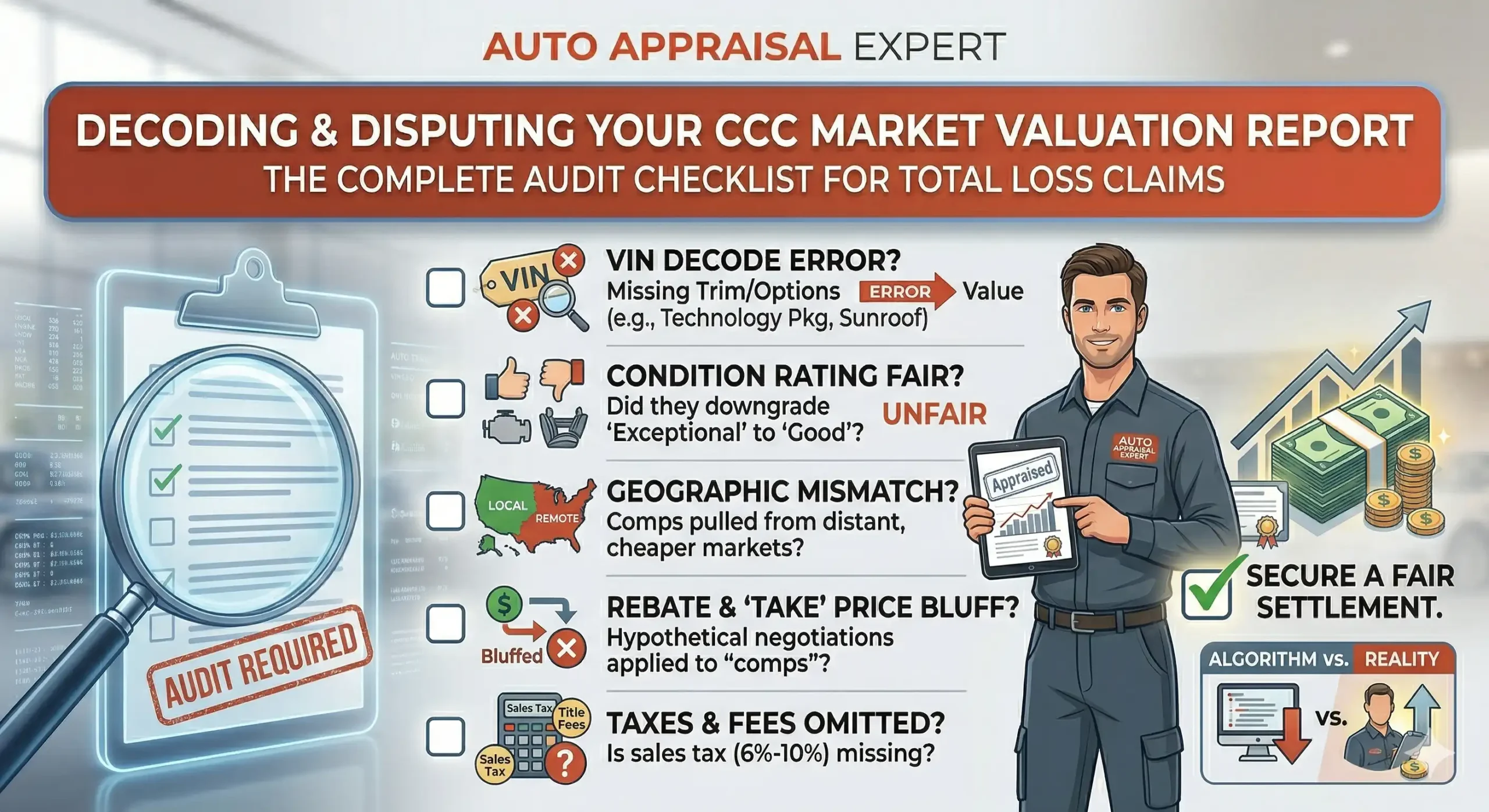

A good classic inspection report does more than describe condition. It gives you third-party support when a carrier relies too heavily on software-generated valuation. That matters because a market valuation report from a platform such as CCC is still a starting point. It is not the final word on a collector vehicle with unusual condition, authenticity, or restoration history.

Use the report to challenge low total loss valuations

In a total loss case, the insurer may miss the details that separate your vehicle from ordinary comparables.

Your inspection can help establish:

- Pre-loss condition

- Originality and authenticity

- Documented options or restoration quality

- Why generic comps are poor matches

- Why the carrier’s Actual Cash Value is understated

If you need deeper valuation support, a dedicated fair market value resource like SnapClaim’s fair market value guide can help frame what should and should not be in a defensible total loss analysis.

Total loss threshold is the point at which the insurer treats the vehicle as uneconomical to repair under state rules or internal claim calculations. That threshold doesn’t erase the need for accurate valuation. It makes accurate valuation more important.

Use the report in diminished value disputes

This is the gap most classic owners don’t see until after repairs.

According to IMC Inspection’s discussion of classic car appraisal gaps, a major blind spot in the market is guidance on post-accident diminished value appraisals for classics, and these vehicles can suffer a 20% to 30% value drop from accident stigma alone. That same discussion notes that a professional inspection report can provide the evidence needed to audit and dispute low CCC-based insurer valuations, especially in states such as California. For added context on the claim itself, review SnapClaim’s diminished value guide.

Diminished value means the drop in market value after proper repairs because buyers discount a vehicle with accident history. On classic vehicles, that stigma can be sharper because collectors care significantly about documented condition and uninterrupted history.

Use the report when invoking the appraisal clause

If the carrier won’t move, check your policy.

Many policies contain an appraisal clause. That clause often allows each side to choose an appraiser to resolve a value dispute. Your inspection report can become the factual backbone of that process by showing what the vehicle was, what it wasn’t, and why the insurer’s assumptions are incomplete.

If you’re preparing that step, this overview of an insurance claim appraisal explains how the process usually works.

For general consumer guidance on insurance complaints and claim handling, your state’s department of insurance is often the best public reference point. The California Department of Insurance is one example of a regulator owners can consult for claim rights and complaint procedures.

The key point is simple. Insurers negotiate from documents. You should too.

Frequently Asked Questions About Classic Car Inspections

How much should classic car inspectors charge?

It depends on the car, the inspector’s expertise, and whether the assignment is a straightforward pre-purchase review or a deeper collector-grade evaluation. In the verified market range, professional inspections typically involve a certain fee, with specialists on rare vehicles sometimes charging more. The key question isn’t price alone. It’s whether the report is thorough enough to support a purchase decision or an insurance dispute.

Can I use a pre-purchase inspection later in a claim?

Sometimes, yes. A strong pre-loss report can help establish prior condition, originality, and market position. That can be useful in a later car appraisal for insurance claim context, especially for a total loss dispute. It works best when the report is detailed, dated, photo-backed, and prepared by a qualified independent professional.

Does every classic need a specialist inspector?

If the vehicle’s value depends on originality, quality of restoration, rare trim, or documented history, yes, a specialist is the safer choice. A regular mechanic can still be helpful on basic mechanical questions, but they usually aren’t enough for collector-level authenticity and valuation issues.

What’s the difference between diminished value and total loss?

Diminished value vs. total loss is one of the most important distinctions in an insurance claim. Diminished value means your repaired classic is now worth less because of its accident history. Total loss means the insurer has decided the vehicle should be settled rather than repaired based on its claim analysis and applicable threshold rules.

Should I accept the insurer’s software valuation?

Not automatically. Carrier software can be useful, but it’s still a starting point. If the vehicle is unusually original, well documented, restored to a high standard, or difficult to compare, you may need an independent auto appraiser and a stronger market valuation report built on dealer-sold comparables and condition-specific analysis.

Don’t leave money on the table. If you’re dealing with a classic vehicle purchase, a low insurance offer, or a dispute over post-accident value loss, Auto Appraisal Expert can help you review the evidence and determine the next step. Get your free claim review or order a certified appraisal report today to take control of your insurance settlement.

About AutoAppraisalExpert

AutoAppraisalExpert is a premier provider of independent vehicle appraisal reports and insurance claim consulting. Our mission is to equip vehicle owners with the data-driven evidence required to recover the full financial value of their asset after an accident. Whether navigating a complex Diminished Value claim or disputing a low-ball Total Loss offer, we provide the certified documentation needed to negotiate with insurance companies from a position of strength.

With a national reach and deep industry expertise, we have helped thousands of policyholders identify errors in carrier valuation reports (like CCC) and invoke the Appraisal Clause to secure fair settlements. We pride ourselves on transparency, speed, and reports that stand up to the toughest insurer scrutiny.

Why Trust This Guide

This guide was written and verified by the AutoAppraisalExpert technical team. Our appraisers specialize in total loss disputes and diminished value forensics. We stay current on state insurance regulations, court-accepted valuation practices, and evolving market trends to ensure our readers, and our clients, always have the most accurate information available.

Ready to see what your car is really worth? Get your free estimate today.