Meta Title: How Do Insurance Companies Calculate Total Loss? Act Now

Meta Description: How do insurance companies calculate total loss? Learn the formulas, dispute low offers, and take action for a fair settlement today.

Your adjuster says the car is totaled, and for a moment that sounds like closure. Then the valuation report arrives, and the number feels wrong.

If you are searching how do insurance companies calculate total loss, you are usually not looking for theory. You want to know why the offer is low, whether the insurer’s math is right, and what you can do next without getting pushed around.

Your Car Is Totaled Now What?

Most owners hit the same wall. The insurer makes the process sound mechanical, almost automatic, as if the settlement amount came from a neutral machine and cannot be questioned.

That is not how this works in practice.

A total loss decision is a business calculation. The carrier compares what your vehicle was worth before the crash with what it would cost to repair it and what the damaged vehicle is still worth as salvage. If any of those inputs are wrong, the result can be wrong too.

The stressful part is that many owners focus on the word “totaled” when the core fight is often about value. A vehicle can be correctly declared a total loss and still be undervalued.

Key takeaway: The total loss decision and the settlement amount are related, but they are not the same issue. You can agree the car is totaled and still dispute the price.

If your offer seems light, do not treat the insurer’s first number as a final ruling. Treat it like an opening position. The strongest responses are calm, documented, and built on better market evidence than the report the adjuster started with.

The Three Pillars of a Total Loss Calculation

A total loss file usually rises or falls on three inputs. Get these right, and you can tell whether the insurer made a fair call or fed weak numbers into a polished report.

Actual cash value

Actual Cash Value, or ACV, is the vehicle’s market value one moment before the crash. It is separate from your loan balance, your down payment, or what you spent on the car years ago.

This is the number owners should watch most closely.

In practice, ACV is often built from comparable vehicles, then adjusted for mileage, trim, options, condition, and local market data. That sounds objective. It is only as good as the inputs. If the report uses the wrong trim level, misses factory options, applies harsh condition deductions, or pulls comparables from the wrong market area, the ACV drops fast.

That is why I tell owners to treat the insurer’s valuation as a starting position, not a final truth. A report generated in CCC ONE or a similar system can look official and still be wrong in ways that matter.

Repair estimate

The second pillar is the repair estimate. This is the projected cost to return the vehicle to pre-loss condition using accepted repair procedures, labor times, parts prices, and paint materials.

Early estimates are often incomplete. A bumper cover, fender, and headlamp can be obvious on day one. Bent structure, suspension damage, wiring damage, calibration work, and hidden safety-system issues may not show up until teardown begins.

That matters because total loss decisions are made on economics, and repair costs often climb after the first inspection. Owners who see a low preliminary estimate should not assume the number is settled.

Two practical points matter here:

- Supplements change the file. Once hidden damage is documented, the repair total can increase enough to shift the carrier’s decision.

- Method matters. Cheap aftermarket parts, recycled parts, or missed calibrations can make an estimate look lower than a proper repair would cost.

Salvage value

The third pillar is salvage value. This is what the damaged vehicle is expected to bring after the loss, usually through a salvage auction or dismantler sale.

Owners rarely see much detail behind this number, but insurers pay attention to it. If the wrecked vehicle still has strong auction value because of reusable parts, a desirable drivetrain, or limited damage to certain components, the carrier may recover more after declaring it a total loss.

That creates a real trade-off. Higher salvage value can push a claim toward total loss in formula-based systems, even when the repairable damage does not look catastrophic to the owner standing beside the car.

Why these three numbers deserve a hard review

Each number can be challenged on facts.

- ACV falls apart when the comparables are weak or the option list is incomplete.

- Repair estimates fall short when teardown has not happened or proper procedures were skipped.

- Salvage values get inflated when the carrier assumes a stronger auction result than the vehicle’s condition supports.

Ask for the valuation report, the full repair estimate, and any condition or options pages used to support the offer. Do not settle for a single payout number on a phone call.

Once you have those documents, you can audit the file line by line. That is how owners stop arguing with an adjuster’s conclusion and start challenging the inputs that produced it.

Inside the Insurer’s Toolkit How They Value Your Car

You get the call. The adjuster says the value came from the system, the report is already generated, and the offer is what it is.

Treat that report as a starting position, not a final answer.

Insurers usually build total loss offers through outside valuation vendors and claims software, often CCC ONE. The report can look technical enough to shut down questions. It may have condition scores, option lists, comparable vehicles, and adjustment tables. That does not make it neutral. It reflects the choices made inside the file, and those choices can be wrong.

What the software does

Valuation software pulls comparable vehicle data, applies adjustments for mileage, equipment, condition, and market area, then produces an actual cash value range or figure. Some carriers also reference pricing guides such as Kelley Blue Book or older NADA-based data, but the claim offer usually turns on the vendor report attached to the file.

CCC ONE is common, and it has real influence in total loss claims. I have reviewed plenty of these reports. The pattern is consistent. If the trim level is off, the options are incomplete, or the comparable vehicles are weak, the final number can come in low while still looking polished on paper.

That is why owners need the full report, not just the payout number.

Where low valuations usually start

The problem is rarely a dramatic mistake. It is usually a stack of small ones.

Common examples include:

- Trim or drivetrain mismatches. A base model comparable against a higher trim, AWD against FWD, or missing package content.

- Bad comparable selection. Vehicles from a different market area, poor condition listings, or units with accident history.

- Condition deductions that lack support. Interior, exterior, or prior damage adjustments without photos or a real inspection basis.

- Missing options and package content. Premium audio, driver-assist packages, tow packages, upgraded wheels, or factory technology features left off the sheet.

- Unsupported comparable adjustments. Large downward adjustments applied in ways the owner cannot verify from the report.

A report can be formatted cleanly and still be built on bad inputs.

What helps in a dispute

Generic book values and random listings usually do not move a claim much. Specific, vehicle-matched evidence does.

What gets attention:

- Dealer listings for close matches in year, make, model, trim, mileage, and equipment

- VIN-based option decoding to prove missing packages or factory features

- Service records, photos, and receipts that support pre-loss condition

- A written independent appraisal that explains why the insurer’s comparables or adjustments do not hold up

What usually does not help:

- Your original purchase price

- Your loan balance

- A sentimental value argument

- Listings from far outside your market

- A single printout with no adjustment explanation

Audit the report like a file reviewer

Read the insurer’s valuation the way an appraiser reads it. Check each comparable for trim, mileage, options, condition, seller type, and distance from your market. Look for missing features on your own vehicle. Look at every deduction and ask a simple question: what is the factual support for this adjustment?

That approach changes the conversation. You are no longer arguing that the offer feels low. You are pointing to the exact inputs that produced it.

For a plain-English explanation of how fair market value is supposed to work in a claim, SnapClaim’s fair market value resource is a useful reference.

Owners also mix up total loss value with diminished value. They are different claim issues. A diminished value claim deals with resale loss after repairs. A total loss claim deals with what your vehicle was worth one minute before the crash.

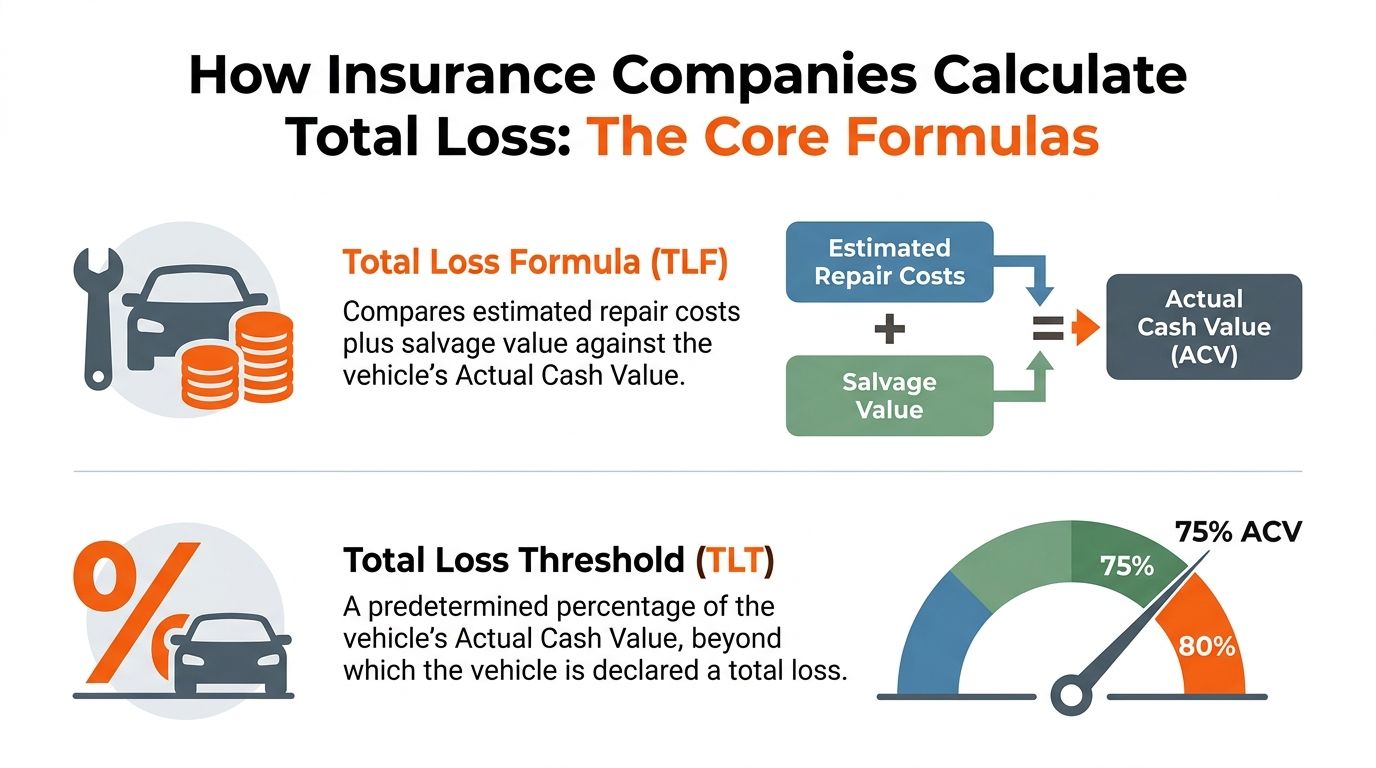

How Insurance Companies Calculate Total Loss The Core Formulas

Insurers usually use one of two core methods. If you know which method applies, you can follow the math yourself and see whether the file makes sense.

Total loss threshold

Under a Total Loss Threshold, or TLT, the insurer compares repair cost to a percentage of the car’s ACV.

Insurance companies use total loss threshold rules that vary by state from 60% to 100% of ACV, according to Better Collision’s overview of key factors and calculations for total loss.

A straightforward example from that same discussion is a vehicle with $10,000 ACV and $7,000 in repairs. At a 70% threshold, the repair cost hits the line exactly, so the insurer can classify the car as a total loss.

This method is easy to grasp:

- Determine ACV.

- Identify the state threshold.

- Compare repair cost against that percentage.

If repairs cross the threshold, the insurer may total the vehicle rather than authorize repairs.

Total loss formula

The second method is the Total Loss Formula, or TLF.

Under TLF, a vehicle is totaled if Repair Costs + Salvage Value > ACV, as explained by Kelley Blue Book’s guide to totaled cars.

This method captures something threshold rules do not. The insurer is not just looking at repair cost. It is looking at repair cost plus what it can recover by selling the damaged vehicle.

Here is the example provided in the verified data:

| Item | Amount |

|---|---|

| Actual Cash Value | $15,000 |

| Salvage Value | $4,000 |

| Maximum repair spend before totaling under TLF | $11,000 |

If repairs go over $11,000, the insurer would generally choose the payout route because repairs plus salvage exceed ACV.

Another example from the verified material shows an ACV of $14,000, repairs of $10,000, and salvage of $6,000. That totals $16,000, which is greater than the ACV, so the vehicle qualifies as a total loss under TLF.

Why insurers like formulas

Formulas give carriers a framework they can defend internally and, to a point, externally. But they still depend on the quality of the numbers plugged into them.

A weak ACV can make a borderline repairable car look totaled. An inflated salvage bid can push the file over the line. That is why owners should not only ask which formula is being used, but also ask where each number came from.

Audit question: Is the disagreement really about the formula, or is it about the value inputs feeding the formula?

Where to verify the method

A good practical check is to review your state’s rules and then compare them to the insurer’s explanation. If the adjuster cites a threshold rule in a state that relies on formula-based analysis, or vice versa, that is a sign to slow down and ask for the basis in writing.

For a consumer-facing overview from a major insurer, State Farm’s totaled car guidance can help you compare general carrier explanations with what you are being told on your own claim.

State Rules Matter How Your Location Changes the Game

The answer to how do insurance companies calculate total loss changes by state. That is not a small detail. It can change whether the same vehicle gets repaired, totaled, or disputed.

Insurance companies determine a vehicle is a total loss using state-specific rules, and those thresholds typically range from 60% to 100% of ACV, with many states around 70% to 75%, according to Kryder Law’s state-threshold overview.

Same damage different outcome

A car with identical damage can produce different outcomes depending on where the claim is handled.

The verified data gives clear examples:

- Alabama: 75% threshold

- Texas: 100% threshold

- Some states without fixed thresholds: TLF applies instead

That means a vehicle may be totaled much sooner in one state than another. In a high-threshold state, the insurer may have more room to consider repair. In a formula-based state, salvage value can become the deciding factor.

Sample state total loss rules 2026

| State | Governing Rule | Example Implication |

|---|---|---|

| Alabama | 75% threshold | Repairs that cross that percentage of ACV can trigger a total loss decision |

| Texas | 100% threshold | Repairs generally must reach full ACV before the threshold is met |

| Arizona | TLF | The claim turns on whether repair cost plus salvage value exceeds ACV |

| Illinois | TLF-style example in verified data | A vehicle can total even when the repair figure alone does not tell the full story |

If you want a more detailed breakdown, review this state-by-state resource on the total loss threshold by state.

Why owners get tripped up here

Adjusters sometimes explain total loss decisions in broad terms. That can leave owners thinking all states use the same trigger.

They do not.

The practical mistake is assuming your friend’s claim in another state should have worked the same way as yours. It may not. Your negotiating power depends partly on whether your state uses a fixed percentage, the Total Loss Formula, or a blended approach.

The right question to ask

Do not ask only, “Why did you total my car?”

Ask this instead:

- What rule did you apply in my state

- What ACV did you use

- What salvage value did you assign

- What repair estimate did you rely on

That forces the discussion out of generic talking points and into claim-specific facts.

How to Dispute a Low Total Loss Offer

A low total loss offer is not a personal insult, and disputing it is not a hostile act. It is a normal valuation disagreement.

The most effective disputes are organized, specific, and supported by better evidence than the insurer used.

Start with the insurer’s own paperwork

Ask for the full valuation package. If the insurer used CCC or a similar platform, request the full market valuation report, not just the summary page.

Then audit it line by line.

Look for:

- Wrong trim or package: A near-match is not the same as an exact match.

- Missing options: Premium audio, safety packages, towing equipment, or factory tech packages can affect value.

- Condition errors: If the report assumes average or rough condition when your vehicle was cleaner or better maintained, challenge that.

- Geographic drift: Comps from outside your true local market can skew value.

For a deeper walkthrough of the common problems inside carrier reports, this guide on how to audit your CCC valuation and secure a fair settlement is worth reviewing.

Build your counterpackage

You do not need a dramatic letter. You need a credible file.

Useful evidence includes:

- Dealer-sold comparables: Better than random classifieds because they are closer to actual retail market evidence.

- Service history: Shows maintenance and can support condition.

- Pre-loss photos: Helps rebut unfair condition deductions.

- Receipts for recent work: Tires, battery, major service, and notable upgrades can matter.

- VIN-correct equipment list: Shows what your vehicle had.

Practical tip: Focus on comparable vehicles that match year, make, model, trim, drivetrain, mileage range, and major options as closely as possible.

Use the appraisal clause when needed

The Appraisal Clause is a policy provision that often gives each side the right to select its own appraiser when there is a disagreement about value. It is one of the most important tools available to owners in total loss disputes.

The verified data notes that policyholders can challenge low ACV conclusions through the policy’s Appraisal Clause and independent appraisal process when insurer valuations are disputed.

The insurer’s software is not the final authority. Your policy may already contain the mechanism for a formal value challenge.

What to say to the adjuster

Keep it calm and businesslike.

A strong message usually does three things:

- Identifies the disputed items

- Attaches supporting evidence

- Requests a revised valuation or appraisal process

A weak message usually says only that the offer “feels too low.”

What not to do

Some moves waste time or weaken your position.

Avoid:

- Threats before evidence

- Sending unrelated listings

- Arguing from loan balance

- Relying only on broad guidebook values

- Accepting the report without reading the adjustments

If your situation involves a repaired vehicle rather than a total loss, you may also want to understand the separate issue of diminished value claims through SnapClaim. Owners often mix those two concepts together, and that can muddy negotiations.

The Independent Appraisal Your Strongest Negotiation Tool

When the insurer’s report is weak, an independent auto appraiser gives you something far more useful than frustration. It gives you evidence.

A professional appraisal is not just a higher opinion of value. It is a documented, supportable analysis built to stand up to scrutiny.

What a strong appraisal includes

The best reports are USPAP-compliant, meaning they follow established professional appraisal standards. They should also rely on certified valuation methodology rather than broad guesswork.

A sound independent appraisal usually includes:

- Dealer-sold comparables or carefully vetted market comps

- Clear adjustments for mileage, condition, and options

- A review of valuation report errors

- A defensible final value conclusion

- Support for Appraisal Clause disputes when needed

If you want a plain-language primer on the process itself, this article on what a car appraisal is is a helpful starting point.

Why this works better than a price guide printout

A KBB screenshot can be a reference point. It is rarely enough to win a hard dispute by itself.

A serious total loss challenge needs a report that addresses the actual vehicle, the actual local market, and the actual flaws in the carrier’s file. That is why a formal car appraisal for insurance claim use carries much more weight than informal pricing opinions.

The author brief also correctly notes a truth many owners discover late. A professional appraisal often uncovers significant overlooked value. Used properly, that does not guarantee a result, but it can materially improve your negotiating position.

Where it fits in the claim

An appraisal is especially useful when:

- The insurer refuses to correct obvious comp errors

- The report undervalues rare trim or equipment

- Condition deductions are aggressive

- You need support to invoke the Appraisal Clause

For a broader claims resource, SnapClaim and its fair-market-value materials can help owners understand what evidence-based valuation should look like in an insurance dispute.

Conclusion Take Control of Your Settlement

A total loss claim feels final when the insurer says the car is done. The valuation is not final just because the adjuster says it is.

You now know how do insurance companies calculate total loss, where the process often breaks down, and how to challenge a weak result. The carrier’s software is a starting point. It is not the law, and it is not the market itself.

Audit the report. Gather better comparables. Use the Appraisal Clause when needed. That is how owners move a total loss dispute from guesswork to evidence.

Frequently Asked Questions About Total Loss Claims

How do insurance companies calculate total loss in most cases

They usually rely on either a total loss threshold or the Total Loss Formula. Under threshold rules, the insurer compares repair cost to a state-set percentage of Actual Cash Value. Under TLF, the insurer totals the vehicle when repair cost plus salvage value is greater than ACV.

Can I dispute a total loss offer if I agree the car is totaled

Yes. That is common.

You can agree that the vehicle should not be repaired and still dispute the insurer’s valuation. The main issue becomes whether the ACV in the carrier’s market valuation report reflects the actual pre-loss market value of your vehicle.

What should I ask the adjuster for after a total loss decision

Ask for:

- The full market valuation report

- The repair estimate

- The salvage value used

- The rule or formula applied in your state

- Any condition or mileage adjustments

Those documents let you verify the math and spot weak comparables or missing equipment.

Is insurance software like CCC ONE the final authority

No. It is a valuation tool.

Insurers use software and third-party vendors as a starting point, but the report can be challenged if the comparables, options, condition ratings, or market assumptions are wrong. That is why many owners hire an independent auto appraiser or invoke the Appraisal Clause.

About AutoAppraisalExpert

AutoAppraisalExpert is a premier provider of independent vehicle appraisal reports and insurance claim consulting. Our mission is to equip vehicle owners with the data-driven evidence required to recover the full financial value of their asset after an accident. Whether navigating a complex Diminished Value claim or disputing a low-ball Total Loss offer, we provide the certified documentation needed to negotiate with insurance companies from a position of strength.

With a national reach and deep industry expertise, we have helped thousands of policyholders identify errors in carrier valuation reports like CCC and invoke the Appraisal Clause to secure fair settlements. We pride ourselves on transparency, speed, and reports that stand up to the toughest insurer scrutiny.

Why Trust This Guide

This guide was written and verified by the AutoAppraisalExpert technical team. Our appraisers specialize in total loss disputes and diminished value forensics. We stay current on state insurance regulations, court-accepted valuation practices, and evolving market trends to ensure our readers and our clients always have the most accurate information available.

Ready to see what your car is really worth? Get your free estimate today.

Call To Action

Don’t leave money on the table. Get your free claim review or order a certified appraisal report today to take control of your insurance settlement.

Take the next step with Auto Appraisal Expert. If your insurer’s total loss offer looks low, get professional help reviewing the valuation, identifying report errors, and building the evidence you need to negotiate from strength.