Meta Title: Total Loss Car Settlement Guide. Dispute Low Offers

Meta Description: Total loss car settlement guide. Learn how to dispute low offers and take action with a certified appraisal today.

Your insurer called your car a total loss, then sent a number that feels wrong. That reaction is common, and in many cases, it is justified.

A total loss car settlement is the amount an insurer offers for your vehicle’s pre-accident value after deciding repairs are not economically practical. It is not a sacred number. It is a valuation decision, and valuation decisions can be challenged.

Most owners get stuck on one question: “Can I fight this?” Yes, if you have evidence. The core dispute is usually about Actual Cash Value (ACV), which means your car’s market value immediately before the loss. The stakes are real. In 2024, the average property damage liability claim reached $6,770, and in a total loss claim that settlement must reflect the vehicle’s full pre-accident worth, making valuation accuracy critical (Better Collision on total loss valuation).

The hard part is that the insurer’s report often looks final. It uses software, market comps, condition adjustments, and dense formatting that makes the result seem objective. But software is a starting point, not a judge.

What works is calm, documented pushback. What does not work is telling the adjuster the offer “feels low” without proof. To strengthen your position, you need the insurer’s math, your own market evidence, and a clear understanding of the appraisal rights built into many policies.

Your Guide to a Fair Total Loss Car Settlement

A low offer usually lands when you are already dealing with towing, rental issues, title paperwork, and the loss of your transportation. That is exactly why many people accept the first number too quickly.

A fair total loss car settlement starts with one mindset shift. The insurer’s first offer is an opening position, not the end of the discussion. If the ACV is off, the settlement is off.

What the insurer is really paying for

The carrier is supposed to value your vehicle as it existed immediately before the crash, theft, fire, or other covered event. That means the focus should be on your specific car, not a generic version of it.

The right questions are practical:

- Was the trim level correct

- Were the mileage and options accurate

- Did the report use true local comparable vehicles

- Did it discount your car for condition without support

- Did it ignore upgrades or recent maintenance that affect marketability

If those pieces are wrong, the offer can be wrong by more than most owners expect.

Why owners lose ground early

Insurers usually control the first draft of the value story. They order the report, choose the software vendor, and present the result in a way that looks neutral.

That does not mean the report is useless. It means you should treat it like any other claim document. Review it, test it, and challenge it where the facts do not hold up.

Key takeaway: The strongest disputes are not emotional. They are built on a better valuation record.

Where to focus first

Start with the basics before you argue over the bottom line:

- Get the valuation report: Ask for the full market valuation report, not just the settlement summary.

- Confirm the loss method: Find out whether the insurer used a threshold rule or a formula.

- Check your policy rights: Look for an Appraisal Clause, which is the contract process used to resolve value disputes without filing a lawsuit.

- Build a file: Keep photos, maintenance records, purchase documents, and receipts for major options or upgrades.

If you want a plain-English overview of fair market value concepts before you review the insurer’s numbers, SnapClaim’s fair market value resource is a useful starting point.

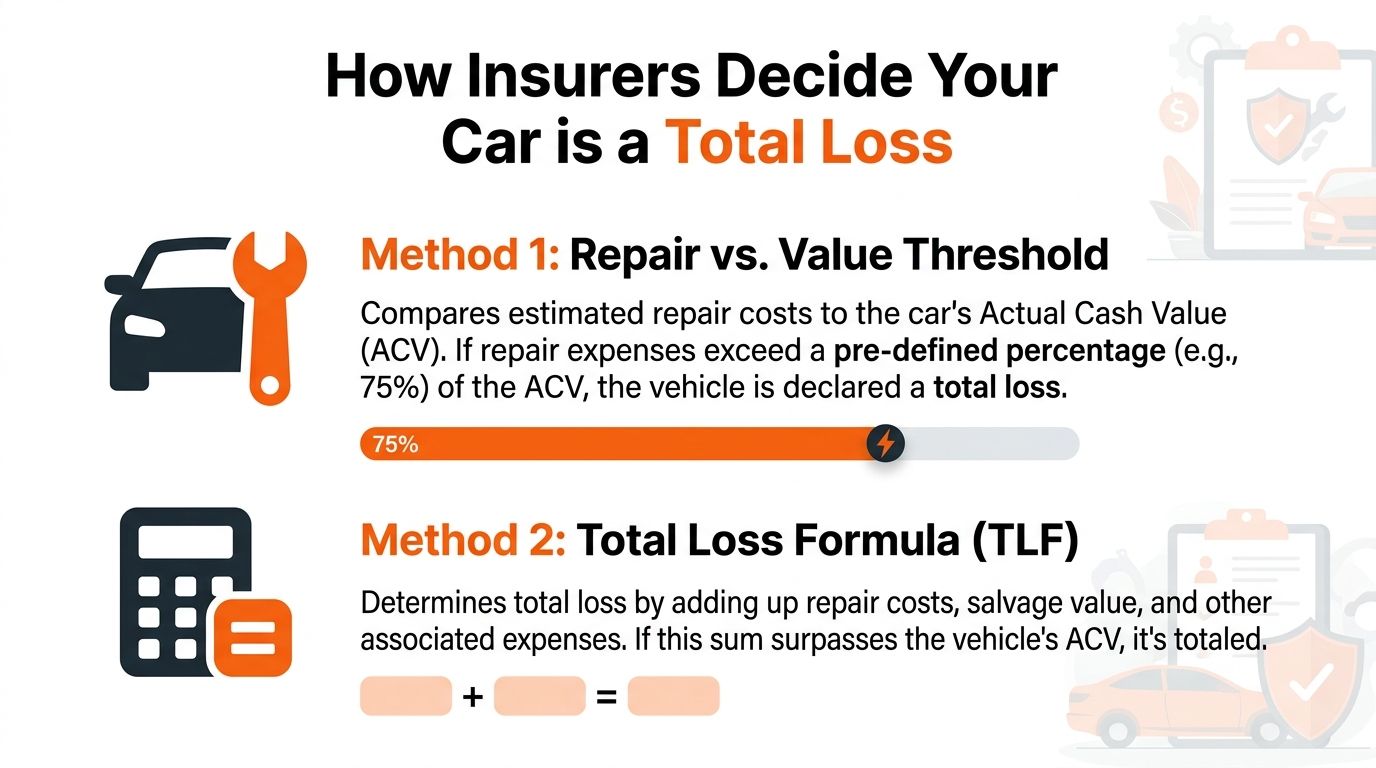

How Insurers Decide Your Car is a Total Loss

“Totaled” is a financial decision before it is anything else. A vehicle can look repairable and still be declared a total loss if the economics do not work.

The threshold method

Many states use a total loss threshold, which is the percentage of the vehicle’s ACV at which repair costs force a total loss decision. The range is wide. Thresholds run from 60% in Oklahoma to 100% in Texas, and in a 75% threshold state like Alabama, a car with a $20,000 ACV is a total loss if repairs exceed $15,000 (SnapClaim’s total loss threshold by state guide).

That single rule can change the outcome dramatically from one state to the next.

Here is a simple comparison:

| State | Threshold | Repair Cost to Total |

|---|---|---|

| Oklahoma | 60% | A $20,000 ACV vehicle totals at $12,000 in repairs |

| Alabama | 75% | A $20,000 ACV vehicle totals at $15,000 in repairs |

| Texas | 100% | A $20,000 ACV vehicle totals at $20,000 in repairs |

If you want a state-by-state breakdown focused on claim strategy, this total loss threshold by state guide is worth reviewing.

The Total Loss Formula

Some states and insurers use the Total Loss Formula (TLF). This method asks whether:

repair cost + salvage value ≥ ACV

Salvage value means what the damaged vehicle is worth after the loss, usually at auction or for parts. Think of it as the insurer’s recovery on the back end.

A straightforward example appears in the verified data: a vehicle with $15,000 ACV and $4,000 salvage value totals when repairs exceed $11,000, because $11,000 + $4,000 ≥ $15,000.

That is why a car can be declared a total loss even when the raw repair estimate seems lower than expected. The insurer is comparing the repair path against the settlement path.

Why this matters in a dispute

Owners often focus only on whether the car should have been repaired. In practice, the better question is whether the insurer used the right rule and the right value inputs.

Three problems show up often:

- Wrong state rule: The carrier applies a generic standard instead of your state’s rule.

- Low ACV: If they undervalue the car, it becomes easier to total.

- Inflated or accepted salvage assumptions: A bad salvage input can change the TLF result.

Practical tip: Before arguing about the settlement amount, verify the total loss decision itself. A flawed threshold analysis can taint the entire claim.

For broader consumer guidance, your state insurance regulator is often helpful. The National Association of Insurance Commissioners consumer resources can help you locate your state department and complaint process.

Decoding Actual Cash Value The Number That Matters Most

You get the call. The adjuster says the car is a total loss and gives you a number that sounds official. For many owners, that is the moment the claim starts to feel settled. It is not.

Actual Cash Value, or ACV, is the number that drives the payout on a total loss claim. Insurers present it as if it were a fixed market fact. In practice, it is a valuation opinion built from selected comparables, software inputs, condition assumptions, and adjustment choices. That matters, because a weak valuation file can push the settlement down before you ever get a chance to respond.

Under many policies, the carrier owes the vehicle’s actual cash value at the time of loss. That usually means the price a buyer would have paid for your specific vehicle, in your market, just before the crash. Consumer references such as Kelley Blue Book can provide pricing context, but they do not control your claim. The insurer’s number is only a starting point if the report behind it is wrong.

I see the same misunderstanding in disputed claims all the time. Owners assume they have to prove the insurer acted in bad faith. Usually they do not. They need to show that the valuation is incomplete, mismatched, or based on poor comparables, then force the issue through the policy’s appraisal process if the carrier will not correct it voluntarily.

ACV depends on inputs, not labels

A valuation report can look polished and still be wrong in the places that count.

Insurers and their vendors generally build ACV from comparable vehicles, then adjust for differences in mileage, trim, options, and condition. Courts and practitioners regularly treat total loss value as a fair market value question tied to comparable sales, dealer listings, and local market evidence. Nolo’s explanation of actual cash value and replacement cost gives a useful consumer overview of that distinction.

The practical takeaway is simple. If the comps are inferior vehicles, if your trim is coded incorrectly, or if options are missing, the final number can be too low while still looking technical on paper.

The dispute is usually about vehicle identity

Before arguing over dollars, confirm the report reflects the right vehicle.

A proper market valuation should account for details that buyers pay for:

- Correct trim level and drivetrain

- Factory packages and standalone options

- Accurate mileage

- Pre-loss condition supported by photos

- Recent service or components that affect marketability

- Local market area, not a convenient wider search that pulls in cheaper comps

Trim errors are common. So are missing option packages. A base model and a higher package version can share the same body style and still carry a meaningful price difference in the retail market.

Recent maintenance is a trade-off area. New tires, brakes, or major service rarely return dollar for dollar, but they can support a stronger condition rating and help rebut blanket downward adjustments.

Retail evidence usually carries the most weight

The strongest challenge file looks like something an appraiser would assemble, not a complaint email.

Start with vehicles offered for sale by dealers or reputable retailers in your market. Match year, make, model, trim, mileage, drivetrain, and major options as closely as possible. Save the listing, the VIN if available, and screenshots showing price and equipment. If you can get the original window sticker or a manufacturer build sheet, use it.

This is the standard I use when reviewing a disputed total loss file. Broad pricing averages are less persuasive than a tight group of actual comparable vehicles. If you want a closer look at how these reports are built and where the common errors appear, review this guide on how to audit a CCC total loss valuation report and secure a fair settlement.

What usually does not help much

Some facts matter emotionally but have limited valuation weight:

- Your original purchase price

- Your loan balance

- General statements that used cars cost more now

- Online estimates that do not match your trim, mileage, and equipment

Those points can explain your frustration. They usually do not prove market value.

Appraiser’s view: ACV is a negotiable valuation conclusion, not an objective endpoint. If the insurer’s number is built on bad comps or bad adjustments, challenge the report, document the correct market evidence, and use the appraisal clause when the carrier refuses to move.

How to Audit Your Insurer’s CCC Valuation Report

Most disputed total loss claims turn on one document. It is usually a CCC Market Valuation Report or a similar software-generated file.

The format looks polished. The charts look technical. That presentation can make owners assume the number is objective. It is not. It is an insurer-commissioned valuation tool.

A notable class action alleged that State Farm used CCC software to manipulate comparable vehicle data and apply arbitrary downward condition adjustments, violating laws requiring payment of full retail cash value (Top Class Actions summary of the CCC allegations).

The CCC report’s goal is to find the cheapest plausible value, not the most accurate one.

Start with the vehicle description

Before you review the comparables, make sure the report correctly identifies your own car.

Check these first:

- VIN and trim: One trim-level error can skew the whole valuation.

- Mileage: Odometer mistakes happen.

- Options and packages: Missing factory equipment is common.

- Condition notes: Some reports apply negative adjustments that do not match the car’s pre-loss condition.

A report can be mathematically neat and still be factually wrong.

Scrutinize the comparable vehicles

Many low valuations are built here.

Look at each comp and ask:

- Is it the same trim or a lesser one

- Is the mileage close

- Is it in your real market

- Is it dealer-sold or some weaker listing type

- Does it have materially different equipment

If your SUV had premium package features and the report uses stripped-down comparables, the average will sink fast.

This detailed guide to auditing a CCC total loss valuation can help you review the report line by line.

Watch the condition adjustments

Condition adjustments often look technical enough to avoid challenge. They should not.

The key questions are simple:

- What exactly was the defect

- Was it documented

- Was the deduction reasonable

- Was the same scrutiny applied to the comps

If your car received a downward adjustment for ordinary wear while the comparables were treated as retail-ready, the valuation is tilted from the start.

Red flags that justify pushback

You do not need to find fraud to dispute a report. Ordinary sloppiness is enough if it affects value.

Common red flags include:

- Base-model comps for a better-equipped vehicle

- Comps located far outside the meaningful market area

- High-mileage outliers

- Unsupported prior damage assumptions

- Missing options

- Duplicate or near-duplicate comparables

- Large negative condition deductions with weak documentation

The algorithm myth

Adjusters sometimes talk about the software as if it settled the matter. It does not.

Software can organize data. It cannot independently verify whether the trim was wrong, whether a comp was a poor match, or whether a condition deduction was fair. A human chose the inputs, and humans can challenge them.

What works: Pointing to specific errors on specific pages.

What does not: Telling the adjuster that you “know the car is worth more” without documents.

If the report has enough defects, it loses persuasive value. At that point, the insurer either revises it or you escalate with a competing appraisal.

Your Action Plan to Dispute a Low Total Loss Car Settlement

A successful dispute is not a rant. It is a file.

The strongest total loss car settlement challenges follow a sequence. You document the errors, build a better market record, and present the insurer with a cleaner valuation than the one it started with.

According to the verified data, policyholders who use professional independent appraisers can recover 15% to 25% more by challenging flawed insurer valuations (Christensen & Hymas on total loss claim valuation disputes).

Step one. Put the dispute in writing

Phone calls are useful for logistics. They are poor for preserving a valuation challenge.

Send a short, professional email or letter that says:

- you dispute the ACV

- you want the full valuation report and all comparable vehicle details

- you identified factual errors or weak comps

- you are gathering counter-evidence

- you reserve your contractual rights under the policy, including appraisal if applicable

Keep the tone neutral. You are not accusing anyone of bad faith at this stage. You are creating a record.

A simple format works:

I dispute the current valuation of my vehicle and the resulting total loss settlement offer. Please provide the complete valuation report, all comparable vehicle data, and any condition adjustment support relied upon. I am gathering dealer comparables and documentation regarding trim, options, mileage, and pre-loss condition, and I request that the claim remain open for review.

Step two. Gather better comparables

Dealer-sold comparables are usually the gold standard in a valuation dispute because they reflect real replacement market conditions.

Use established listing platforms and save the evidence carefully. Good sources often include dealer listings on major marketplaces and local dealer inventory pages.

Capture:

- Full listing screenshots: Include price, VIN if shown, mileage, trim, and dealer name.

- Vehicle details pages: These often show packages and equipment.

- Geographic relevance: Favor your market or a defensible nearby market.

- Date captured: Listings change.

If you need a place to start, SnapClaim offers educational resources around claim documentation and valuation disputes.

Step three. Organize your support file

Your evidence packet should be clean enough that an adjuster or supervisor can review it quickly.

Include:

- purchase documents if available

- service records

- tire or major maintenance receipts

- option/package proof

- pre-loss photos

- a concise summary of report errors

Do not bury the point. Lead with the biggest valuation defects first.

Step four. Consider a professional car appraisal for insurance claim support

There is a point where a DIY challenge stops being efficient. That point usually arrives when the insurer digs in behind its software.

A professional car appraisal for insurance claim support can help when:

- the CCC report uses poor comparables

- the vehicle has uncommon options or trim

- the market is thin

- the condition adjustments are aggressive

- the claim may need appraisal clause escalation

An independent auto appraiser should be using recognized methods and a report format that can survive scrutiny. In practice, the strongest reports are USPAP-compliant, meaning they follow the Uniform Standards of Professional Appraisal Practice, which is the core professional framework appraisers use to document and support valuation opinions.

Step five. Present the countercase clearly

Do not send a pile of attachments with no roadmap. Give the insurer a short cover summary.

A useful structure is:

- Vehicle errors in the insurer report

- Comparable errors in the report

- Your better comparables

- Supporting records for options and condition

- Requested revised value review

Practical tip: Adjusters respond better to an organized valuation package than to repeated calls asking for “more money.”

What works and what fails

What usually works

- factual corrections

- dealer comparables

- option proof

- professional appraisal support

- escalation to a supervisor when the file supports it

What usually fails

- emotional arguments

- unsupported online estimates

- arguing from loan balance

- broad claims that “the market is crazy”

- accepting the insurer’s comparables without checking trim and mileage

If direct negotiation stalls, the next serious tool is not another angry email. It is the appraisal clause.

Invoking the Appraisal Clause Your Contractual Right

Many owners do not realize their policy may already contain the mechanism to resolve a value fight. It is called the Appraisal Clause.

How the process usually works

In plain terms:

- you select your appraiser

- the insurer selects its appraiser

- if the two appraisers cannot agree, they select an umpire, which is a neutral third appraiser

- the dispute is decided through that process based on valuation evidence

This is why the quality of your appraisal matters. A weak opinion does not gain influence just because it is labeled an appraisal.

If you want a practical overview of the process, this insurance claim appraisal guide is a helpful reference.

Why this changes the power dynamic

Before appraisal, the insurer can hide behind its software and internal review layers. Once appraisal is invoked, the issue becomes evidence-driven.

That shifts the conversation in a useful way. The question stops being “Will the adjuster reconsider?” and becomes “Which valuation is better supported?”

Why report quality matters

If your case may reach appraisal, the supporting valuation should be built like it will be examined by another appraiser and possibly an umpire.

That means:

- clear comparable selection

- documented adjustments

- support for trim and options

- defensible condition analysis

- real market data rather than guesswork

A USPAP-compliant report carries more weight because it follows recognized appraisal standards. It is not magic, but it is far harder to dismiss.

Important distinction: Appraisal decides value disputes. It usually does not decide coverage disputes. If the insurer says the loss is not covered at all, that is a different fight.

When to invoke it

The clause becomes useful when:

- the insurer has your evidence and still refuses to correct obvious valuation defects

- the dollar gap is meaningful

- the report errors are structural, not minor

- you need a binding process rather than endless back-and-forth

Used correctly, the Appraisal Clause is the policyholder’s strongest tool for influence in a total loss car settlement dispute. It forces the discussion back to fair market value, where it belongs.

Frequently Asked Questions About Total Loss Settlements

How long do I have to dispute a total loss offer

The deadline depends on your policy, the insurer’s procedures, and your state’s claim rules. Do not assume you have unlimited time. Ask the adjuster for the claim deadline in writing, review your policy, and start your dispute as soon as you receive the valuation report.

What happens if I still owe money on my car loan

In a financed total loss, the insurer typically pays the lender first. If the settlement is less than the loan payoff, you may still owe the difference unless you have GAP coverage. GAP insurance covers the gap between the ACV settlement and the remaining loan or lease balance.

Can I keep my totaled car and repair it myself

Sometimes, yes. If you keep the vehicle, the insurer generally reduces the payout to account for salvage value. You also need to understand the title consequences. Many states require a salvage title, and a rebuilt title process may be necessary before the vehicle can return to the road legally.

Does diminished value apply in a total loss claim

Usually, no for that same vehicle. Diminished value vs. total loss is an important distinction. Diminished value means a repaired vehicle lost market value because of its accident history. A total loss means the vehicle is not being valued as a repaired car for return to market. If you want a plain-language explanation of diminished value claims, SnapClaim’s diminished value page is a solid reference.

Do I have to accept the insurer’s CCC report

No. You can challenge the report’s comparables, adjustments, trim coding, options, and condition assumptions. The report is evidence. It is not a final ruling.

Should I negotiate myself or hire help

That depends on the file. If the valuation errors are obvious and the market is easy to document, some owners can make progress on their own. If the report is dense, the trim or options are unusual, or the insurer is leaning hard on software, an independent appraiser is often the more efficient move.

A low total loss car settlement can leave you short when it is time to replace the vehicle. The owners who do best are the ones who treat the claim like a valuation problem, not just an insurance problem. Get the report. Audit it. Build better comparables. Use the Appraisal Clause if the carrier refuses to correct the numbers.

Don’t leave money on the table. Get your free claim review or order a certified appraisal report today to take control of your insurance settlement with Auto Appraisal Expert.

About AutoAppraisalExpert

AutoAppraisalExpert is a premier provider of independent vehicle appraisal reports and insurance claim consulting. Our mission is to equip vehicle owners with the data-driven evidence required to recover the full financial value of their asset after an accident. Whether navigating a complex Diminished Value claim or disputing a low-ball Total Loss offer, we provide the certified documentation needed to negotiate with insurance companies from a position of strength.

With a national reach and deep industry expertise, we have helped thousands of policyholders identify errors in carrier valuation reports (like CCC) and invoke the Appraisal Clause to secure fair settlements. We pride ourselves on transparency, speed, and reports that stand up to the toughest insurer scrutiny.

Why Trust This Guide

This guide was written and verified by the AutoAppraisalExpert technical team. Our appraisers specialize in total loss disputes and diminished value forensics. We stay current on state insurance regulations, court-accepted valuation practices, and evolving market trends to ensure our readers, and our clients, always have the most accurate information available.

Ready to see what your car is really worth? Get your free estimate today.