Meta Title: What Does Total Loss Mean in Insurance? Act Now

Meta Description: What does total loss mean in insurance? Learn your rights, dispute low offers, and get fair value. Read the guide and take action now.

Your adjuster says the car is a total loss. Then they give you a number that feels wrong.

That’s the moment most owners freeze. They assume the decision is final, the software is objective, and the check cannot be changed. It isn’t. If you’re asking what does total loss mean in insurance, you need more than a definition. You need a strategy for protecting the value of your vehicle and your rights under the policy.

Your Insurance Nightmare The Total Loss Phone Call

The call usually sounds routine on their end.

“Your vehicle has been declared a total loss.”

Then comes the settlement figure. You do the math in your head and realize it probably won’t buy a similar replacement in your area. That’s when the panic starts.

I’ve seen this pattern over and over. The owner isn’t upset because the car was damaged. They’re upset because the number doesn’t line up with the market. The insurer is talking from a market valuation report. The owner is thinking about what it would take to replace the vehicle they had yesterday.

Those are not always the same thing.

A total loss decision is often just an economic decision by the carrier. It doesn’t automatically mean the vehicle is impossible to repair. It means the insurer believes paying Actual Cash Value, or ACV (the vehicle’s value immediately before the loss), is cheaper than fixing it.

Your car may be totaled. Your claim is not over.

If the first offer feels low, trust that instinct and verify it with evidence. Insurers use systems and vendors built for speed and consistency. You need to look at whether the data behind that offer matches your vehicle, your trim, your options, your mileage, and your local market.

Here’s the hard truth. Many owners accept the first number because they’re exhausted, short on transportation, and worried about storage fees or loan payments. That pressure is real. But pressure is not proof that the valuation is fair.

You still have options:

- Review the valuation report: Ask for every comparable vehicle and every condition adjustment.

- Check the ACV: If the ACV is wrong, the whole settlement starts from the wrong number.

- Use a car appraisal for insurance claim support: Real market evidence changes negotiations.

- Consider an independent auto appraiser: A third-party valuation can expose problems in the insurer’s report.

Decoding the Total Loss Declaration

A total loss is not magic. It’s math mixed with state law.

In the United States, a vehicle is declared a total loss when repair costs exceed a state-specific total loss threshold, typically ranging from 60% to 80% of the car’s ACV, and many states use a 75% benchmark according to Bankrate’s explanation of total loss rules.

What ACV means

Actual Cash Value is what your car was worth right before the crash. Not what you paid for it. Not what you still owe. Not what it costs to buy a cleaner replacement from a dealer tomorrow.

Insurers usually build ACV from details like:

- Year and model: Basic identity of the vehicle

- Mileage: Higher mileage usually lowers value

- Condition: Prior wear, prior damage, and maintenance can affect value

- Options and trim: Packages, safety features, and upgrades matter

- Local market: A vehicle’s value in one region may not match another

That last point matters more than people realize. A vehicle should be valued in the market where it would reasonably sell, not in some cheaper market that drags your number down.

What the total loss threshold does

The total loss threshold is the legal or practical line where the insurer decides repair no longer makes financial sense. Some states use a fixed percentage. Others use a formula instead of a hard percentage.

That’s why two similar cars with similar damage can get different outcomes in different states.

Practical rule: The total loss decision and the settlement amount are two different fights. Even if the carrier is right that the car is totaled, they can still be wrong about what it was worth.

If you want a plain-language overview from a major insurer, Progressive’s total loss resource is a useful starting point for general definitions.

The part owners miss

People often focus only on whether the vehicle should have been repaired. That’s usually not the best battle.

The bigger issue is often valuation. If the insurer undervalues the ACV, everything downstream gets worse:

- Your payout drops

- Your loan shortfall can grow

- Your replacement options shrink

- Your negotiating position weakens unless you challenge the report

That’s why understanding what does total loss mean in insurance matters. It means the carrier has chosen the payout route. It does not mean you have to accept their number without checking the math.

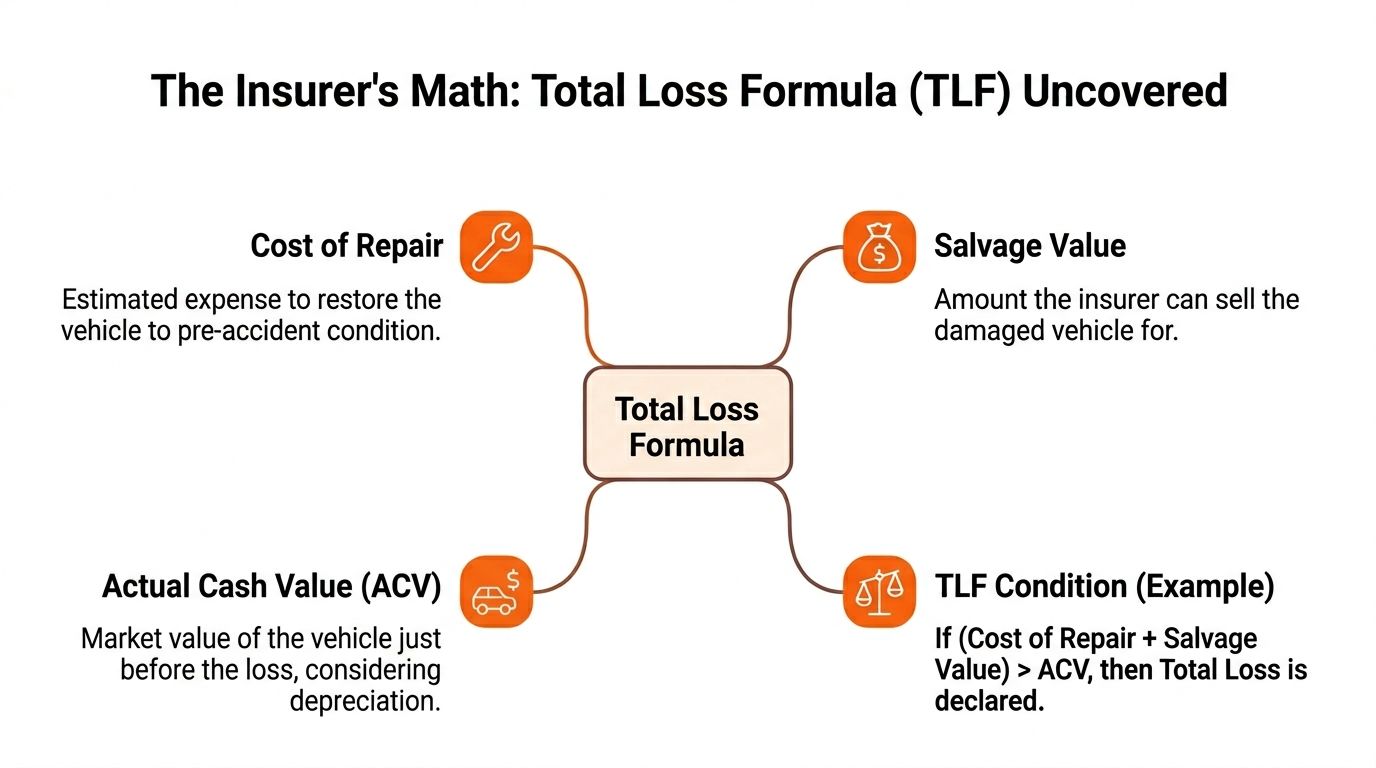

The Insurer’s Math The Total Loss Formula Uncovered

When a state uses the Total Loss Formula, the insurer compares repair cost against the vehicle’s value after accounting for salvage value, which is what the damaged vehicle can bring at auction.

Using the TLF, if a vehicle’s ACV is $15,000 and its projected salvage value is $4,000, the repair threshold becomes $11,000. If repairs exceed that amount, the insurer declares a total loss, as outlined by Quilia’s glossary explanation of total loss.

The formula in plain English

The carrier is not just asking, “Can this car be repaired?”

They’re asking, “Does it make financial sense to repair this car when we could pay ACV and recover money from the wreck through salvage?”

That’s why salvage value matters. The more the insurer expects to recover at auction, the easier it becomes for them to declare the vehicle a total loss.

Here’s the logic:

- Start with ACV

- Subtract salvage value

- Compare the result to repair cost

- If repairs exceed that number, the carrier totals the car

If you want a state-by-state overview of how different jurisdictions handle thresholds and formulas, this breakdown of the total loss threshold by state is useful.

The algorithm myth

Many claims go sideways at this stage.

Insurers often present software outputs, especially a CCC Market Valuation Report, as if the number came from a neutral machine that discovered truth. That’s not how valuation works.

Software is only as good as the inputs, assumptions, and adjustments inside it. If the report uses weak comparables, trims down your condition, misses options, or pulls from a softer market, the output can still look polished while being wrong.

A printed report is not the same as a fair valuation.

CCC ONE and similar systems are tools. They are not final authority.

Where the number gets pushed down

Watch for these issues in the insurer’s market valuation report:

- Wrong comparables: They use base models when you owned a better trim.

- Geographic mismatch: They pull vehicles from cheaper markets.

- Condition deductions: They apply blanket deductions that don’t reflect your car’s actual pre-loss condition.

- Missing features: Packages, wheels, driver-assist systems, or premium audio can disappear in the report.

- Dealer reality ignored: Dealer-sold comparables often reflect what replacement costs better than abstract adjustments do.

A fair car appraisal for insurance claim purposes should test the report, not worship it. Real value comes from real market data, especially dealer-sold comparables and accurately matched listings in your area.

Your Car Is Totaled What Happens Now

Once the insurer declares a total loss, you’re usually looking at two paths. Neither is automatically right. Both come with consequences.

If a policyholder keeps a totaled vehicle, the payout is reduced by the car’s salvage value, and owner-retained salvage often leaves the net payout 15% to 25% lower than full ACV, while also requiring a salvage title, according to Wikipedia’s overview of total loss and retained salvage.

Option one, take the settlement and surrender the car

This is the simpler route.

You sign the title over, the insurer takes possession, and the claim closes once value is agreed. The carrier then disposes of the vehicle through salvage channels. If you have a loan, the lender may get paid first depending on the balance.

This option usually makes sense when:

- The damage is extensive: Repair logistics would be a headache

- You need a clean replacement path: You don’t want title complications

- You don’t want future resale problems: A salvage history hurts marketability

Option two, retain salvage and keep the vehicle

Some owners want to keep the car because it has sentimental value, they believe repairs can be managed, or they think they can come out ahead.

Be careful.

When you retain salvage, the insurer reduces your payout because they aren’t getting the wreck to sell. You keep the car, but you also keep the headache. In many states, you’ll deal with a salvage title, which is a branded title showing the vehicle was declared a total loss.

That creates practical problems:

- Registration can become more complicated

- Insurance options may narrow

- Resale value usually drops

- Financing a salvage or rebuilt vehicle is harder

- Inspection and repair documentation may be required before the car returns to the road

For a more detailed walkthrough of the process, see what happens if insurance totals your car.

A side by side view

| Decision | What you get | Main upside | Main drawback |

|—|—|—|

| Surrender the vehicle | Agreed ACV, subject to policy terms | Cleanest exit | You lose the car |

| Retain salvage | Reduced payout plus the damaged car | You keep the vehicle | Lower net payout and title complications |

Keeping a totaled car only makes sense if you understand the title consequences, the repair path, and the reduced payout before you sign anything.

Don’t choose salvage retention just because the check feels small. Fix the valuation first. Then decide what to do with the vehicle.

Why Your Total Loss Offer Is Probably Too Low

The first offer is often not the fair offer.

A 2025 J.D. Power study found that 65% of total loss claimants received initial offers below fair market value, and independent audits found that valuations from tools like CCC can be 20% to 30% below what real market comparables support, as summarized in The Hartford’s totaled car guidance.

Why the gap happens

Insurers don’t pay claims by walking dealer lots and asking what it really takes to replace your vehicle. They rely on valuation systems and vendor reports. Those reports can miss reality in ways that consistently lower ACV.

Common problems include:

- Bad comparable selection: A cheaper trim level is not a comparable.

- Condition downgrades: Generic deductions can undercut a well-kept car.

- Feature omissions: Trim packages and options are often undervalued or skipped.

- Market lag: Fast-changing local prices don’t always show up cleanly in standardized reports.

That’s the value gap. The insurer calls the report “market value.” The market says otherwise.

What fair market value should rely on

A proper valuation should be grounded in evidence people can verify. The best evidence usually includes:

- Dealer-sold comparables

- Same or very similar trim

- Close mileage

- Matching options

- Reasonable geographic relevance

- Accurate pre-loss condition analysis

If you want a broader explanation of how fair market value is approached, SnapClaim’s fair market value resource is a solid primer. Their main site also has useful insurance-claim context.

The insurer’s report is a starting bid. Treat it like one.

What to review before you respond

Don’t argue in general terms. Audit the report line by line.

Look for:

- Model mistakes: wrong drivetrain, trim, or body style

- Mileage errors: even small mistakes can matter

- Condition assumptions: especially unexplained deductions

- Option omissions: technology, safety, premium packages

- Comparable quality: local, similar, and comparable

Here, people also confuse diminished value vs. total loss. A total loss claim is about what the car was worth immediately before the crash. A diminished value claim is about loss in market value after repairs. They are related topics, but they are not the same claim.

Your Playbook for Disputing a Low Total Loss Offer

If the offer is low, don’t vent. Build a file.

Policyholders who actively dispute low total loss offers by invoking the Appraisal Clause and supplying their own market data audits can recover 18% more on average than the initial offer, according to Sargent Law Firm’s discussion of total loss disputes.

Start with the insurer’s own paperwork

Request the full market valuation report, not just the settlement summary.

You want every page that shows:

- the comparables

- the options list

- the condition adjustments

- the valuation date

- the source of the data

If they used CCC ONE or a similar system, review it as if you’re auditing a contractor’s estimate. Because that’s what you’re doing.

Build your evidence file

Now gather what supports your car’s real pre-loss value.

Include:

- Dealer listings: Same year, make, model, trim, and similar mileage

- Service records: These help support condition

- Photos: Pre-loss photos can show cosmetic condition and options

- Purchase documents: Useful for confirming trim and factory equipment

- Upgrade evidence: Wheels, packages, accessories, and installed features

A strong car appraisal for insurance claim dispute is specific. “My offer feels low” won’t move an adjuster. “Comparable one is a base trim and lacks my package” might.

Bring in an independent auto appraiser

An independent auto appraiser changes the tone of the claim.

An independent auto appraiser provides a third-party valuation based on real market evidence, not just the carrier’s chosen report. The best reports are USPAP-compliant, meaning they follow recognized professional appraisal standards and use certified valuation methodology that can stand up under scrutiny.

That matters because adjusters are used to complaints. They respond differently to documented evidence.

A credible appraisal report can:

- Challenge weak comparables

- Correct trim and equipment errors

- Support better ACV with dealer market data

- Provide a basis for formal escalation

For related negotiation tactics, this guide on total loss settlement negotiation is worth reading.

Use the Appraisal Clause if the carrier won’t move

The Appraisal Clause is a policy provision that lets each side select an appraiser when they disagree on value. If the two appraisers can’t agree, an umpire may be involved depending on the policy language and process.

This right is powerful because it shifts the fight away from a one-sided adjuster conversation.

Expert advice: Don’t invoke the Appraisal Clause blindly. First build your evidence, understand your policy language, and make sure the dispute is about value.

A simple order of operations

- Get the report

- Mark the errors

- Collect real comparables

- Document condition and options

- Obtain an independent appraisal

- Negotiate in writing

- Invoke the Appraisal Clause if needed

You don’t need to be loud. You need to be organized.

Frequently Asked Questions About Total Loss Claims

Is total loss the same as diminished value

No. A total loss claim pays for the vehicle’s pre-accident value because the insurer has decided not to repair it. A diminished value claim argues that a repaired vehicle is still worth less in the market because it now has an accident history. For more background on that second issue, SnapClaim’s diminished value page gives a helpful overview.

| Attribute | Total Loss Claim | Diminished Value Claim |

|---|---|---|

| Core issue | Vehicle is not being repaired economically | Vehicle was repaired but lost market value |

| Valuation focus | Pre-loss ACV | Post-repair loss in resale value |

| Vehicle outcome | Usually surrendered or retained as salvage | Owner keeps repaired vehicle |

| Main dispute | Fair market value before loss | Value stigma after repair |

Can I dispute a total loss offer if I agree the car is totaled

Yes. Those are separate issues. You can agree the vehicle meets the total loss threshold and still challenge the insurer’s ACV. That is often the smarter path.

What is gap insurance and does it increase my car’s value

GAP insurance covers the difference between the insurance settlement and your loan balance in some situations. It does not increase your car’s ACV. It helps with loan exposure, not valuation.

How long do I have to dispute a total loss offer

That depends on your policy language, your state, and whether the carrier has imposed paperwork or title deadlines. Don’t wait. Ask for the valuation report immediately, preserve your records, and put disputes in writing as soon as you identify errors.

If your settlement feels light, don’t guess. Get evidence. A professional review can identify report errors, weak comparables, and missed value before you sign away your ability to negotiate. Visit Auto Appraisal Expert if you need help understanding your options, challenging a low offer, or getting a certified report that supports a stronger dispute. Don’t leave money on the table. Get your free claim review or order a certified appraisal report today to take control of your insurance settlement.

About AutoAppraisalExpert

AutoAppraisalExpert is a premier provider of independent vehicle appraisal reports and insurance claim consulting. Our mission is to equip vehicle owners with the data-driven evidence required to recover the full financial value of their asset after an accident. Whether navigating a complex Diminished Value claim or disputing a low-ball Total Loss offer, we provide the certified documentation needed to negotiate with insurance companies from a position of strength.

With a national reach and deep industry expertise, we have helped thousands of policyholders identify errors in carrier valuation reports (like CCC) and invoke the Appraisal Clause to secure fair settlements. We pride ourselves on transparency, speed, and reports that stand up to the toughest insurer scrutiny.

Why Trust This Guide

This guide was written and verified by the AutoAppraisalExpert technical team. Our appraisers specialize in total loss disputes and diminished value forensics. We stay current on state insurance regulations, court-accepted valuation practices, and evolving market trends to ensure our readers, and our clients, always have the most accurate information available.

Ready to see what your car is really worth? Get your free estimate today.