Meta Title: Dispute Total Loss Offer and Write a Car Off Fairly

Meta Description: Dispute total loss offer with expert steps. Audit the valuation, use the Appraisal Clause, and push for a fair settlement today.

Your insurer says they want to write a car off, and the number they offered feels wrong. That’s one of the most frustrating calls in the claims process because it sounds final, though it often isn’t.

If you need to dispute total loss offer decisions, start with this mindset. A total loss decision is a valuation decision. And valuation decisions can be challenged when the facts, condition, options, and comparable sales data don’t line up.

Your Car Was in an Accident Now What

The first thing to know is simple. A write-off is not a judgment on you, and it isn’t automatically the last word on what your car was worth.

In insurance language, a total loss means the carrier believes the vehicle is uneconomical to repair or unsafe to return to the road. It does not mean the insurer’s first settlement number is automatically fair.

That distinction matters because many owners freeze when the adjuster says the car is totaled. They assume the process is over. In practice, it’s often the beginning of a financial negotiation.

This happens more than generally assumed. In the UK, a car was declared a total loss every 90 seconds, or nearly 1,000 vehicles per day, according to Best4Gap’s summary of write-off frequency. The exact figures vary by country, but the point is clear. Total loss claims are common, and insurers process them at scale.

What to do before you answer the adjuster

Don’t argue from memory. Build a file.

- Ask for every claim document: Request the valuation report, repair estimate, comparable vehicle list, and any condition deductions.

- Save your own proof: Gather maintenance records, purchase paperwork, window sticker if you have it, photos from before the crash, and receipts for recent tires, options, or upgrades.

- Confirm the title status: If there’s a loan, find out who gets paid first and whether GAP coverage may apply.

- Read a plain-English overview: If you need a quick primer on the process after a total loss decision, this guide on what happens if insurance totals your car is a useful starting point.

Your carrier has a process. You have rights under the policy. Those are two different things.

What not to do

A few mistakes weaken your position fast:

- Don’t accept a verbal explanation: You need the written market valuation report.

- Don’t focus only on repair cost: In most disputes, the primary fight is over pre-accident value.

- Don’t assume software is neutral: The report may look objective, but inputs drive outcomes.

If you stay calm and document everything, you shift the claim from pressure to proof.

Understanding the Total Loss Formula

A carrier doesn’t write a car off because someone in claims has a bad feeling about it. They use a formula.

At the center of that formula are two numbers. One is the vehicle’s Actual Cash Value, or ACV, which means the pre-accident market value of your specific car. The other is the repair cost. If repair costs rise too close to or above the relevant limit, the insurer treats the vehicle as a total loss.

According to Activate Group’s explanation of how insurers calculate a write-off, insurers typically declare a vehicle a total loss when repairs exceed a percentage of pre-accident value, often ranging from 50% to 75%, and they consider make, model, mileage, condition, and regional sales data to determine ACV.

What ACV really means

Owners often hear ACV and think of one of three things:

- the amount they still owe

- the price they see on a dealer lot

- the amount they paid recently

ACV isn’t any of those by default.

It is supposed to reflect what your vehicle was worth in the local market immediately before the loss, considering its actual trim, mileage, options, condition, and comparable sales. That’s why a market valuation report matters so much. If the report starts with bad comparables or wrong equipment data, the final number is skewed before the adjuster even calls you.

Why trade-in and dealer retail aren’t the same

A dealer retail listing includes overhead, reconditioning, and profit. A trade-in number reflects what a dealer might pay while leaving room to resell the car. ACV sits in a market-based zone that depends on real comparable transactions and listings, not a generic book figure alone.

That gap creates confusion. Owners see similar cars advertised for more than the insurer offers and assume the carrier is wrong. Sometimes they are right. Sometimes the comparison is off because the listed cars are newer, cleaner, lower-mileage, or higher-trim.

The only way to know is to audit the details.

Where the dispute usually lives

Most total loss arguments happen in one of these places:

| Dispute Point | Why it matters |

|---|---|

| Vehicle details | Wrong trim, drivetrain, package, or mileage changes the base value |

| Condition adjustments | Excessive deductions can pull the ACV down unfairly |

| Comparable selection | Poor local matches distort what your car would have sold for |

| Missing options | Factory packages and equipment may be omitted |

| Threshold analysis | Borderline cases can turn on how value and repairs were calculated |

Practical rule: If you want to dispute total loss offer numbers, challenge the inputs before you challenge the conclusion.

A simple way to think about the math

Think of the claim like a balance scale.

If the insurer lowers your ACV, the vehicle reaches total loss territory more easily. If the repair estimate rises, the same thing happens. That is why two owners with similar damage can get very different results based on the valuation data behind the file.

Car appraisal for insurance claim work also becomes useful here. A proper independent review doesn’t just say the offer is low. It explains where the insurer’s math went off track.

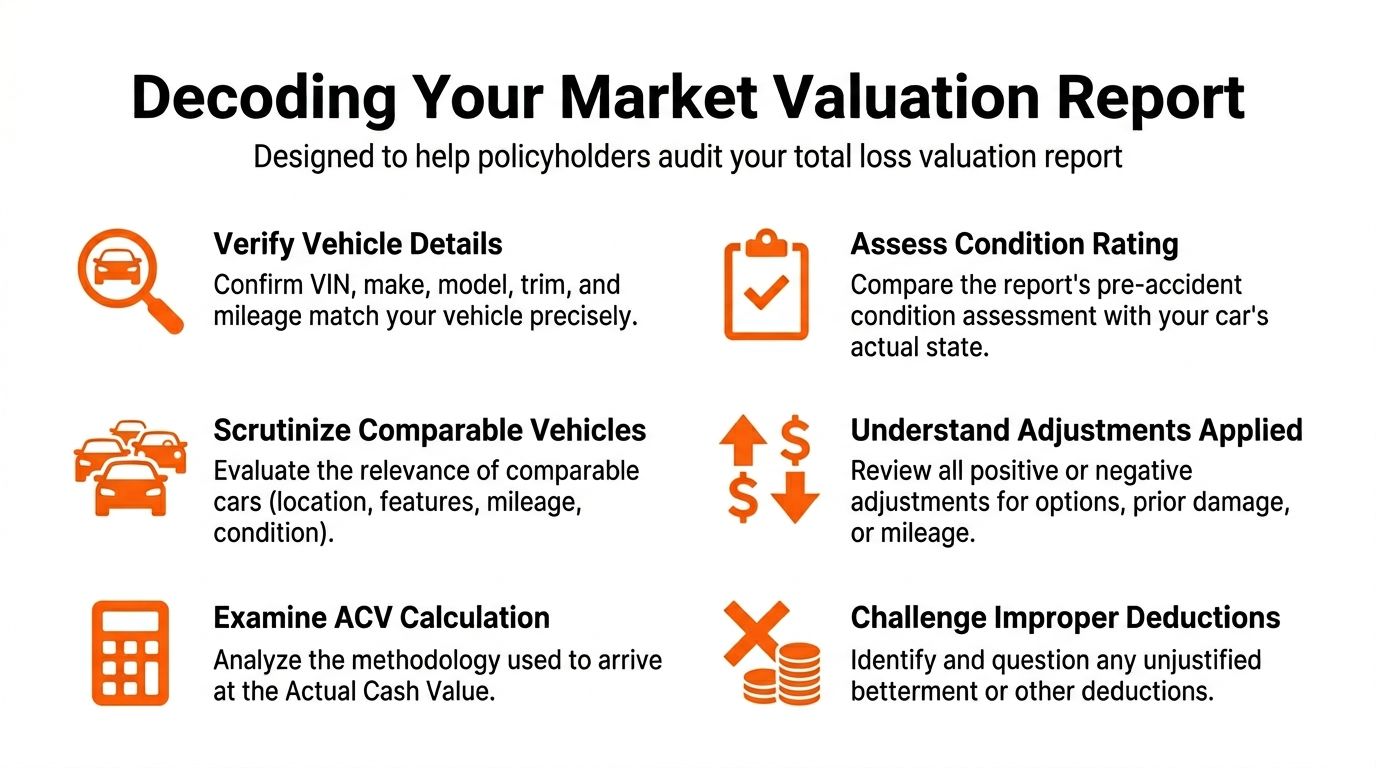

Decoding the Insurer’s Market Valuation Report

Most owners don’t lose value disputes because the insurer was unquestionably right. They lose because they never audited the report.

The standard valuation package, often a CCC report or similar file, looks technical and final. It isn’t. It’s a starting point built from data inputs, assumptions, adjustments, and comparable vehicles. If those inputs are wrong, the output is wrong.

If you want a broader explanation of fair valuation principles, review SnapClaim’s overview of fair market value in auto claims. It helps frame what a valuation should capture.

Start with the identity section

Before you read the numbers, confirm the vehicle itself.

A surprising number of reports miss equipment or use a broad trim label that doesn’t reflect the actual car. If the report identifies the wrong drivetrain, trim package, upholstery, technology package, tow package, or wheel package, the valuation may be low from page one.

Use this checklist:

- Verify the VIN and trim: The VIN should decode to your exact vehicle, not a near match.

- Confirm mileage: Check the odometer figure used. A mileage error can trigger a bad adjustment.

- Review options line by line: Premium audio, driver assistance, sport packages, upgraded wheels, and factory towing equipment are easy to miss.

- Check prior condition notes: If the report says your car had prior damage or poor finish, ask what evidence supports that.

Read the comparable vehicles like an appraiser

Comparable vehicles are the heart of the report, and this section often exposes most low offers.

A real comparable should be close in market relevance, not just vaguely similar. That means similar trim, model year, mileage, condition, equipment, and local market area. A base model from far away is not a strong comp for a higher-spec local vehicle.

Look for these red flags:

- Distant listings: A comp from a very different region may not reflect your local market.

- Mismatched trims: A lower trim can subtly drag the average down.

- Mileage gaps: High-mileage comps can depress value if adjustments are weak.

- Condition inflation against you: The report may rate comparables generously while rating your vehicle harshly.

- Unavailable or stale comps: If the listing sold long ago or can’t be verified, question its relevance.

A CCC report is only as credible as the comparables and adjustments inside it.

Audit every adjustment

Valuation software applies upward or downward adjustments for mileage, condition, prior damage, options, and market factors. Many owners skim past this section. Don’t.

The “value gap” appears here.

Common adjustment problems

| Adjustment Area | What to check |

|---|---|

| Mileage | Was the baseline mileage reasonable for the year and model? |

| Condition | Did they deduct for wear without photos or documentation? |

| Prior damage | Are they assuming old damage without repair records review? |

| Options | Are key factory features missing or undervalued? |

| Comparable changes | Did they adjust comps in a one-sided way that always lowers your value? |

A carrier may also describe a deduction in language that sounds neutral but isn’t supported. “Typical reconditioning” and “dealer-ready adjustments” deserve scrutiny if they lower your number without clear proof.

Build your rebuttal with better evidence

You don’t need to outtalk the adjuster. You need better documents.

Strong rebuttal evidence usually includes:

- Dealer-sold comparables: Same generation, trim, and similar equipment in your market.

- Vehicle-specific records: Window sticker, service history, pre-loss photos, and receipts.

- Correction list: A clean summary of each report error and the page where it appears.

- Independent valuation support: A third-party appraisal based on certified methodology.

If the car had recent work that improved marketability, include that too. New tires, major maintenance, and factory-correct condition support can matter, even if they don’t translate dollar-for-dollar.

What works and what doesn’t

What works:

- calm written challenges

- local dealer comparables

- exact trim correction

- documentation for options and condition

- a professional independent auto appraiser

What doesn’t:

- sending random listings from a different market

- arguing only from loan balance

- saying “Kelley Blue Book says more” without vehicle-specific support

- threatening a lawsuit before you’ve built a record

For repaired vehicles, owners also confuse diminished value vs. total loss. If the insurer totals the vehicle, the claim is about pre-loss market value. If the car is repaired, then post-repair loss in market value becomes a different issue. SnapClaim’s page on diminished value claims is useful if your vehicle is repaired rather than totaled.

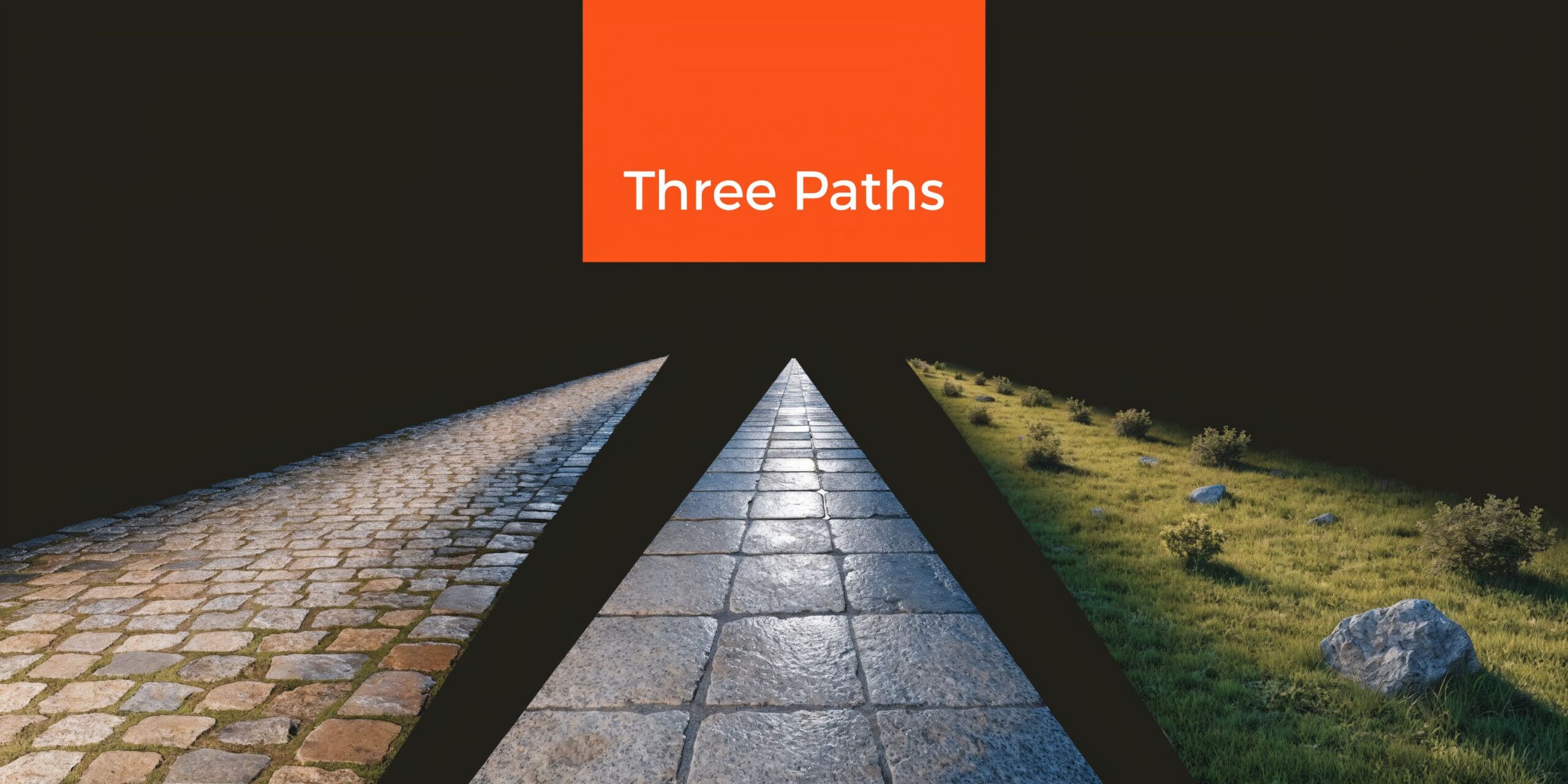

Your Three Options After a Total Loss Decision

Once the insurer says they plan to write a car off, you usually have three practical paths. Many individuals only see one because the adjuster frames the call around acceptance.

That’s a mistake. Each path has different financial and legal consequences.

Option one, accept the settlement

This is the fastest route. It makes sense when the report is accurate, the comparables are solid, and the offered amount reflects the local market.

Best fit for owners who:

- need quick resolution

- have reviewed the valuation and found no material errors

- don’t want to retain the vehicle

The trade-off is obvious. Once you accept too quickly, it gets much harder to reopen a dispute.

Option two, keep the vehicle as owner-retained salvage

Some owners want to keep the car. Maybe the damage is manageable, the vehicle has sentimental value, or they have access to lower-cost repairs.

If you retain the vehicle, the insurer typically deducts salvage value from the settlement and the title consequences can change. That can affect resale, financing, future insurability, and registration requirements.

This path can work when:

- you know the repair path realistically

- you understand the title branding issue

- the vehicle has value to you beyond the claim payout

It doesn’t work well when owners treat it as a way to “win twice.” Keeping a salvage vehicle brings long-term limits.

Option three, dispute the valuation

This is the right path when the problem is not the total loss label itself but the number attached to it.

Signs a dispute is worth pursuing:

- Wrong vehicle data: trim, options, mileage, or drivetrain errors

- Weak comparables: distant, mismatched, or lower-spec vehicles

- Unsupported deductions: condition penalties with little proof

- Local market mismatch: dealer listings in your area suggest a higher value

The strongest disputes aren’t emotional. They are specific.

A side-by-side view

| Option | Main Benefit | Main Risk | Best for |

|---|---|---|---|

| Accept | Fast closure | Leaving money on the table | Accurate valuations |

| Retain salvage | Keep the vehicle | Title and repair complications | Owners with a clear rebuild plan |

| Dispute | Potential to increase your settlement | More time and documentation needed | Lowball valuation cases |

The decision most owners regret

The most common regret isn’t disputing too hard. It’s accepting too soon because the report looked official.

If you aren’t sure, pause the process and ask for the support behind every major deduction and comparable. A short delay used for evidence review is often smarter than a quick signature.

How to Dispute a Low Offer and Write a Car Off on Your Terms

A low offer doesn’t fix itself. You need a method.

The owners who recover better settlements do the same few things well. They get the report. They audit it line by line. They respond in writing. And when the carrier won’t move, they use the policy’s Appraisal Clause.

If you want added context on negotiation tactics before invoking appraisal, review this guide on total loss settlement negotiation.

Step one, ask for the full valuation packet

Don’t work from the check amount alone.

Request:

- the CCC or other market valuation report

- the repair estimate

- the comparable vehicle pages

- the condition rating basis

- the policy language for valuation and appraisal

If the insurer won’t send something, note the request in writing and keep a timestamped copy.

Step two, create an error log

Use a simple list. One issue per line.

Example categories:

- wrong trim

- omitted package

- mileage error

- unsupported condition deduction

- weak comp from outside market

- comp with materially different options. Adjusters respond better to a structured rebuttal than to general frustration.

Step three, gather dealer-sold and dealer-listed comparables

Owners often go off course at this point. They pull any car they can find online.

That approach usually fails.

Use comparables that are:

- same model generation

- similar trim and equipment

- similar mileage range

- in your market or a defensible nearby market

- relevant to pre-loss condition

Dealer-sold comparables are stronger than random asking prices because they reflect real market behavior. Dealer listings still help, but they must be closely matched.

Step four, submit a written valuation dispute

Keep the tone firm and clean. No speeches.

A good dispute letter includes:

- claim number

- vehicle identification

- statement that you dispute total loss valuation

- numbered list of report errors

- supporting attachments

- request for revised ACV review within a stated time

Use this sentence: “I dispute the current Actual Cash Value determination because the valuation report contains factual errors and unsupported adjustments that do not reflect my vehicle’s pre-loss market value.”

Step five, bring in an independent auto appraiser

This is the turning point in stronger cases.

A qualified appraiser doesn’t say the car is worth more. They produce a USPAP-compliant report. That means it follows recognized appraisal standards and uses certified appraisal methodology that can stand up to insurer scrutiny.

The report should address:

- exact vehicle identification

- market area

- comparable vehicle selection

- condition analysis

- option verification

- support for each adjustment

- final fair market value conclusion

A proper car appraisal for insurance claim work product provides an advantage here. It gives the adjuster, supervisor, or defense counsel something specific to evaluate rather than something easy to dismiss.

In practice, professional reports often uncover additional value that basic insurer reports may overlook. The right way to present that is not as a guarantee, but as evidence that a certified review has the potential to increase your settlement when the original report is flawed.

Step six, invoke the Appraisal Clause

This is the part many articles mention but don’t explain.

The Appraisal Clause is a policy provision that usually allows each side to select its own appraiser when there’s a dispute over value. Those appraisers then work to resolve the valuation issue, and if needed, a neutral umpire helps decide the outcome.

Read your policy carefully because wording varies. But the process commonly looks like this:

- You send written notice invoking appraisal under the policy.

- You name your appraiser.

- The insurer names its appraiser.

- The appraisers review the valuation dispute.

- If they disagree, an umpire may be selected under the policy terms.

This is not you “starting a war.” It is you using a contractual right built into the policy for value disputes.

Why the Appraisal Clause matters

It changes the conversation.

Instead of asking the same adjuster to reconsider the same report, you move the dispute into a structured valuation process. That focuses everyone on evidence, not scripts.

What helps at this stage:

- a certified independent report

- a clean package of comps and corrections

- policy language quoted accurately

- professional communication

What hurts:

- invoking appraisal before you understand the policy

- hiring someone who only sends generic pricing screenshots

- confusing liability issues with valuation issues

Step seven, keep your file organized

Use one folder for every document. Save PDFs. Save emails. Save screenshots of listings with dates.

If the matter escalates to counsel, arbitration, or regulatory review, a clean file gives you credibility. A messy claim file weakens a valid dispute.

For general complaint channels and consumer guidance, your state’s insurance regulator is often the best official starting point. The National Association of Insurance Commissioners consumer map can help you locate the correct state department.

State-Specific Rules and Total Loss Thresholds

One of the biggest mistakes I see is owners taking national advice and applying it as if every state handles total losses the same way. They don’t.

Total loss threshold rules vary across the country. According to CarBuzz’s overview of write-off categories and threshold variation, states can set the threshold anywhere from 70% to 100% of ACV, and it notes that states such as Texas and Florida have adjusted thresholds in response to inflation and rising repair costs.

That matters in borderline cases. A vehicle near the line in one state may be repaired in another.

Why local law changes strategy

If your state uses a stricter threshold, the carrier may have less room to total a vehicle based on repair cost alone. If the threshold is higher, ACV disputes can become even more important because the valuation number directly affects how the carrier classifies the loss.

For a deeper state-by-state breakdown, this resource on total loss threshold by state is a useful reference.

Sample State Total Loss Thresholds 2026

| State | Total Loss Formula (TLF) Threshold | Governing Body |

|---|---|---|

| Texas | 80% | State law and insurance regulation |

| Florida | 80% | State law and insurance regulation |

| States with lower threshold models | 70% | State law and insurance regulation |

| States using higher threshold models | 100% | State law and insurance regulation |

This table is intentionally high level because threshold rules can change, and formula application can depend on statute, regulation, salvage rules, and insurer practice.

One-size-fits-all advice is dangerous in total loss claims. Your state rule can change the entire posture of the dispute.

A practical check

Before you accept or reject a total loss determination, confirm:

- Which state’s law applies

- Whether the carrier is using a statutory threshold or internal formula

- Whether title branding rules affect your options

- Whether a threshold change could affect a borderline case

If you’re unsure, verify with your state insurance department before making a final decision.

Insurance Write-Off vs Tax Write-Off A Critical Distinction

People use the phrase “write a car off” in two totally different ways. That causes real confusion.

An insurance write-off means the insurer says the vehicle isn’t economical to repair or should not return to the road in normal service. A tax write-off means a business may be able to deduct qualifying vehicle expenses under tax rules.

An insurance write-off is about vehicle value. A tax write-off is about business expenses. They are not the same.

That confusion is common enough that it was specifically identified in the background material. The issue becomes more complicated when the vehicle is used for business because an insurance payout can interact with basis recovery and depreciation recapture, as noted in this discussion of the insurance-total-loss-versus-tax-deduction confusion.

Why this matters in a claim

For a personal vehicle, your total loss settlement is generally a property damage claim issue. You are fighting over pre-loss market value.

For a business vehicle, you may need to think about both:

- the insurance valuation dispute

- the tax treatment of the payout and prior depreciation

Those are separate analyses. Your appraiser handles value. Your tax professional handles tax consequences.

The clean takeaway

If your insurer says they will write a car off, don’t let tax language distract you from the immediate issue. First confirm the vehicle’s fair market value. Then, if the vehicle was used in business, ask your CPA how the payout fits into your books.

Take Control of Your Total Loss Settlement

When an insurer decides to write a car off, the first number on the table is not a verdict. It’s a position.

If you need to dispute total loss offer numbers, focus on evidence. Audit the valuation report. Correct the vehicle data. Challenge weak comparables. Use local market support. If the carrier will not fix a flawed ACV, the Appraisal Clause can move the dispute into a more balanced process.

The best outcomes come from owners who stop treating the report like a mystery and start treating it like an appraisal file that can be tested. That’s how you close the gap between a software-generated estimate and a supportable fair market value.

Don’t leave money on the table. Get your free claim review or order a certified appraisal report today to take control of your insurance settlement.

Frequently Asked Questions About Total Loss Claims

How long do I have to dispute a total loss offer

It depends on your state law, your policy terms, and where the claim sits procedurally. Act quickly. The longer you wait, the harder it becomes to preserve relevant comparable listings and claim documents from the date of loss.

Can I get diminished value if my car is a total loss

Usually no. These are different claim paths. A total loss claim pays for the vehicle’s pre-loss market value. A diminished value claim applies when the car is repaired but still worth less because of accident history.

What happens if I still owe money on my car loan

Your lender may get paid first from the settlement because it holds a financial interest in the vehicle. If the settlement is less than your loan balance, you may still owe the difference unless you have GAP coverage.

Is CCC the final authority on what my car was worth

No. CCC or similar software is a valuation tool, not the law and not the final authority. The report can be challenged if it uses weak comparables, wrong equipment, bad condition adjustments, or inaccurate market assumptions.

If your insurer wants to write a car off and the numbers don’t add up, Auto Appraisal Expert can help you challenge the valuation with evidence that insurers have to take seriously. Our certified appraisal reports are built to support total loss disputes, audit CCC-style valuation reports, and help policyholders use the Appraisal Clause effectively. If your offer feels low, don’t guess. Get the data you need to negotiate from a stronger position.

About AutoAppraisalExpert

AutoAppraisalExpert is a premier provider of independent vehicle appraisal reports and insurance claim consulting. Our mission is to equip vehicle owners with the data-driven evidence required to recover the full financial value of their asset after an accident. Whether navigating a complex Diminished Value claim or disputing a low-ball Total Loss offer, we provide the certified documentation needed to negotiate with insurance companies from a position of strength.

With a national reach and deep industry expertise, we have helped thousands of policyholders identify errors in carrier valuation reports (like CCC) and invoke the Appraisal Clause to secure fair settlements. We pride ourselves on transparency, speed, and reports that stand up to the toughest insurer scrutiny.

Why Trust This Guide

This guide was written and verified by the AutoAppraisalExpert technical team. Our appraisers specialize in total loss disputes and diminished value forensics. We stay current on state insurance regulations, court-accepted valuation practices, and evolving market trends to ensure our readers, and our clients, always have the most accurate information available.

Ready to see what your car is really worth? Get your free estimate today.